Environmental Test Chambers Market: Strategic Imperatives for 2026 Decision-Makers

As companies rewire product development, supply chains and regulatory roadmaps to meet a more exacting decade ahead, environmental test chambers have moved from specialized lab equipment to a strategic asset. PW Consulting’s latest Environmental Test Chambers Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes multi-year market performance and forward scenarios to help executives convert environmental testing capability into a competitive advantage. The market expanded steadily through the first half of the decade — rising from under USD 900 Million in 2020 to roughly USD 1,019 Million in 2025 — and our models show it tracking toward roughly USD 1,334 Million by 2032, implying a mid-single-digit compound annual growth rate (3.8% CAGR across the 2026–2032 forecast window). This steady expansion masks important inflection points that procurement, R&D and aftermarket leaders must act on in 2026.

Environmental Test Chambers Market

Why this study matters in 2026

- Regulatory shifts are non-linear: Recent revisions to environmental testing standards — including updated dry heat procedures and expanded mechanical stress tests — increase the technical bar for validation. Firms that anticipate standard amendments will shorten certification timelines and reduce time‑to‑market risk.

- Sustainability and refrigerant transitions are now executable strategy: Adoption of low‑GWP refrigerants (for example, CO2 / R744 in specific chamber classes) is moving from pilot projects to commercial deployments. Capital planning that ignores retrofits or new‑builds for low‑emission systems will face stranded asset risk and rising compliance costs.

- Demand profile is broadening: Traditional buyers (automotive, aerospace, electronics) are joined by pharmaceuticals, battery manufacturers and climate resilience initiatives, each bringing different test protocols and service expectations. The result: more bespoke systems, and elevated demand for integrated lab services.

- Market structure has strategic implications: The market sits in a middle state of concentration: several global vendors hold substantial presence, yet there is room for regional specialists and service‑oriented entrants to capture share. This creates both partnership and consolidation opportunities for established players and new entrants alike.

What the PW Consulting report delivers (practical, actionable content)

- Concise executive dashboards that translate macro growth and regulatory signals into three decision-ready scenarios (Base, Accelerated Adoption, and Disruption) tailored for 2026 CAPEX planning.

- Buyer’s playbook and procurement scorecards — vendor evaluation matrices that combine technical capability, service footprint, retrofit readiness (including refrigerant conversion), and total cost of ownership (TCO) over 7–10 year lifecycles.

- Technology adoption roadmap — mapping which chamber capabilities (e.g., high heat‑load walk‑ins, HALT/HASS, battery safety rigs) become mission‑critical by application, and suggested R&D investment timing to capture test-driven product differentiation.

- Regulatory impact matrix — a practical tool linking specific standard changes to required equipment changes, test laboratory processes, and validation timelines so compliance teams can prioritize mitigations.

- Service and aftermarket playbook — models to size serviceable installed base, design subscription and lab‑as‑a‑service offerings, and quantify margin expansion through spare parts, retrofits and calibration contracts.

- Competitive benchmarking and M&A signal map — granular supplier profiles, strengths/weaknesses, partnership fit assessments and a shortlist of acquisition targets by strategic intent (capacity, technology, geographic reach).

- Data deliverables — downloadable time‑series market sizing, forecast matrices, pricing trend proxies and sensitivity analyses to stress test business cases for 2026 investment cycles.

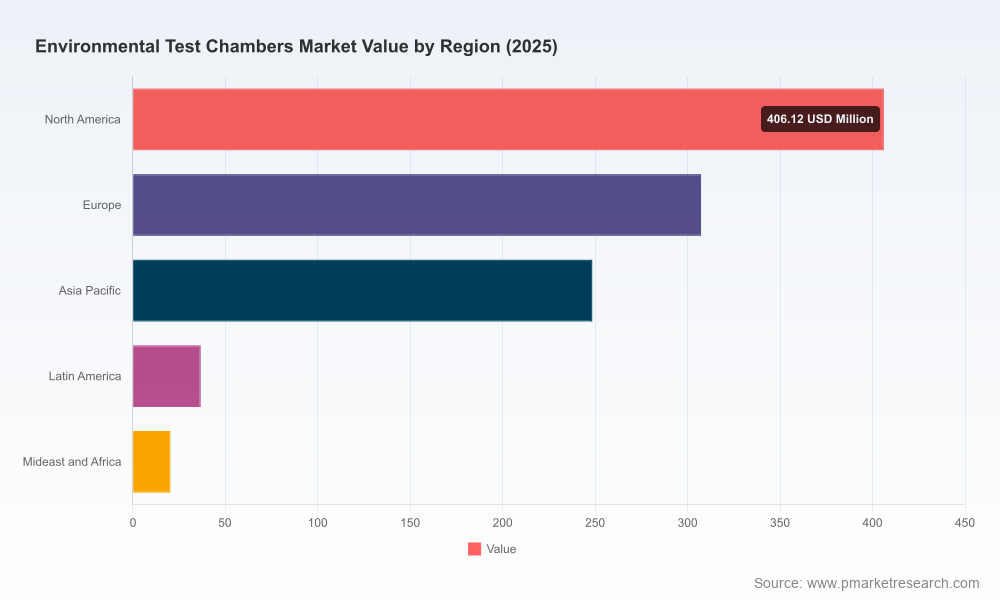

Note: This overview showcases the frameworks and decision tools in the study. The full report contains the granular regional and application splits, model spreadsheets, and live vendor scorecards that underpin these recommendations.

Environmental Test Chambers Market

Competitive landscape — patterns to watch (and the players shaping them)

The competitive fabric of the environmental test chamber market combines legacy OEM engineering depth with agile, regional challengers and service innovators. Several observations emerge from our 2025 market audit and vendor interviews:

Environmental Test Chambers Market

- Product breadth as a defensive moat — Firms with the broadest portfolios of chamber types (from compact reach‑in units to full walk‑in and drive‑in configurations) sustain enterprise relationships across multiple business units and life‑cycle stages. Their installed base becomes the platform for aftermarket growth and recurring calibration revenues.

- Specialized simulation capabilities win in high‑margin niches — Suppliers that invest in HALT/HASS systems, high heat‑load walk‑ins for data center simulation, and combined environmental/vibration rigs capture premium projects in aerospace, server OEMs and EV battery validation.

- Regional lab capability influences purchasing patterns — Market entrants that pair equipment sales with local test facilities or lab‑as‑a‑service offerings accelerate adoption among SMEs and OEM supply chains reluctant to commit to CAPEX.

Key vendors profiled in the study illustrate these dynamics. Leading global OEMs maintain scale and cross‑application product portfolios; specialized firms differentiate on simulation fidelity and modularity; regional manufacturers compete aggressively on customization and cost. Our competitive concentration analysis shows a market where top three vendors control a meaningful share — but the top five leave ample room for second‑tier consolidation and nimble specialists to win vertical segments.

Recent market activity underlines the shifting product and service priorities: new-generation endurance chambers and high‑heat walk‑ins designed to simulate server loads have entered the market, full-service environmental testing facilities have been established in growth markets to reduce time‑to‑test, and novel chambers touting sub‑percent accuracy are being launched for demanding regulatory contexts. Parallel to product innovation, refrigeration chemistry advances and standards updates are reshaping retrofit and replacement economics.

Strategic playbook for 2026 (prioritized actions for executives)

- Reprice procurement against TCO and compliance lag: Move beyond purchase price to include refrigerant transition costs, certification time, spare parts lead times and service footprints. For 2026 CAPEX, prioritize systems with modular retrofittability to low‑GWP refrigerants where practical.

- Build lab partnerships or lab‑as‑a‑service offerings: If your organization lacks volume justification for owned chambers, secure preferential access to certified labs or invest in joint facilities to compress validation cycles during product launches.

- Invest selectively in differentiated chamber capabilities: Identify 1–2 mission‑critical testing capabilities (e.g., high heat load, HALT/HASS, battery safety) and create center‑of‑excellence roadmaps. Focus R&D spending to reduce external test dependency for these profiles.

- Design aftermarket and service revenue engines: Convert installed base into recurring revenue via preventive maintenance contracts, calibration subscriptions and software‑enabled uptime SLAs. Service margins will be a primary lever for mid‑cycle margin improvement.

- Scan M&A and partnership corridors: Target capabilities and geographies where incumbent OEM footprints are thin — service networks, specialized simulation vendors, or regional manufacturers with retrofit know‑how are high‑impact targets in 2026.

- Map compliance milestones into product roadmaps: Use the regulatory impact matrix in this study to assign ownership and budgets for standard changes; align test capability investments so validation is a gating function, not a post‑launch liability.

How to use this research in boardroom decision cycles

Procurement directors will use the report’s buyer scorecards to standardize vendors across global sites and to create five‑year replacement schedules that reflect refrigerant and standards risks. R&D leaders will use the technology adoption roadmap to prioritize test fixtures and lab investments that shave months off validation. Service and aftermarket directors will use the installed‑base models to design subscription tiers and to forecast spare‑parts inventories. Corporate strategy and M&A teams will run the competitive and scenario models to calibrate bolt‑on acquisition bids and to price earn‑outs tied to service growth.

We have intentionally framed this article as a strategic trailer: it highlights the analytical depth and the practical deliverables you can expect, while omitting the granular regional and application splits, the vendor scorecard detail and the downloadable model files that constitute the core intelligence for operational decisions. Those elements are included in the full PW Consulting report and the associated data pack.

Next steps — how to capture the advantage in 2026

- Request the full report package (includes models and vendor scorecards) to convert the scenarios into site‑level CAPEX and service plans.

- Run a rapid 90‑day diagnostic using our regulatory impact matrix and TCO tools — identify the single highest value retrofit or service offering to launch in 2026.

- Engage with our advisory team for a 2‑week vendor selection sprint or an M&A target screening based on the competitive maps in the study.

For leaders balancing product reliability, regulatory certainty, and sustainability imperatives, the environmental test chamber market presents both a compliance necessity and a platform for competitive differentiation. The choices you make in 2026 — about which capabilities to own, which to outsource, and how to monetize service — will materially affect cost, speed to market and product credibility for the remainder of the decade.

For detailed analysis of this topic, please visit the official page:Environmental Test Chambers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com