Interface Bridge ICs Market: Strategic Briefing for 2026 Decisions

As PW Consulting’s lead industry analyst, I present a focused briefing that contextualizes our full Interface Bridge ICs Market study and explains why this intelligence is mission-critical for technology, procurement, and corporate development teams preparing strategic moves in 2026. This briefing is designed as a high-value “preview”: it demonstrates our analytic depth and the practical implications of the findings, while directing decision-makers to the full report for the detailed segment tables, vendor scorecards, and transaction-level data that underpin confident action.

Interface Bridge ICs Market

Macro view — what the numbers say

Our bottom-up market model shows the interface bridge IC market moving from a smaller niche in the early 2020s to a stable, modest-growth industry by the mid-2020s. Total market revenue grows from the early 2020s into 2025 and is forecast through 2032 with a compound annual growth rate of approximately 2.8% over the forecast period. That cadence reflects a mix of secular drivers (Type-C and high-speed external interfaces, expanding automotive zonal architectures) and offsetting forces (module-level integration, aggressive low-cost alternatives, and tighter OEM cost controls). The net result for 2026 stakeholders is a market that offers pockets of attractive margin and strategic leverage—but requires precision in segment focus and partnership strategy.

Interface Bridge ICs Market

Why this matters for 2026 strategic decisions

- Timing of design cycles: Bridge ICs sit early in OEM and tier‑1 design windows; selection decisions made in 2026 will cascade through BOMs and supplier commitments for several model years, especially in automotive and industrial programs with long qualification timelines.

- Margin compression vs. premium differentiation: Commoditization at the low end continues to compress prices, while vendors that combine hardware with certification, software stacks, and integrated power/PD features can sustain premium pricing.

- Supply resilience and qualification risk: Component shortages and distribution arbitrage have created real operational risk. Procurement and product teams need granular supplier intelligence to avoid late-stage redesigns or single‑source exposures.

- M&A and partnership windows: The market’s structural dynamics create specific targets for bolt‑on acquisitions and JV structures—especially for companies seeking to add automotive grade IP or driverless USB/C capabilities rapidly.

What our full report delivers (practical, actionable content)

The complete PW Consulting study is organized to support three types of 2026 decisions—product roadmapping, commercial planning, and corporate development. Key deliverables include:

Interface Bridge ICs Market

- Granular market sizing and forecast model (2020–2032) with scenario tabs to stress-test outcomes under alternate technology adoption and price‑decline vectors.

- Competitive landscape deep-dive: vendor matrices, capability mapping, go‑to‑market footprints, and route‑to‑qualification timelines for automotive, industrial, and consumer OEMs.

- Technology and feature heatmaps that show where value accrues (e.g., Type‑C/PD integration, driverless connectivity, high‑baud-rate UART bridges, automotive functional safety readiness).

- Supply chain risk map and procurement playbook—covering single‑source exposures, alternate vendor routing, distributor trustworthiness, and inventory hedging strategies.

- Commercial & pricing playbook: battleground strategies for suppliers facing both low‑cost commodity alternatives and premium, certified solutions.

- M&A & partnership screening: prioritized target list, valuation sensitivity checks, and integration risk templates designed for acquirers and PE sponsors.

- Use cases and design‑win timelines: actionable recommendations for OEMs and module makers on accelerating time to market while preserving margin.

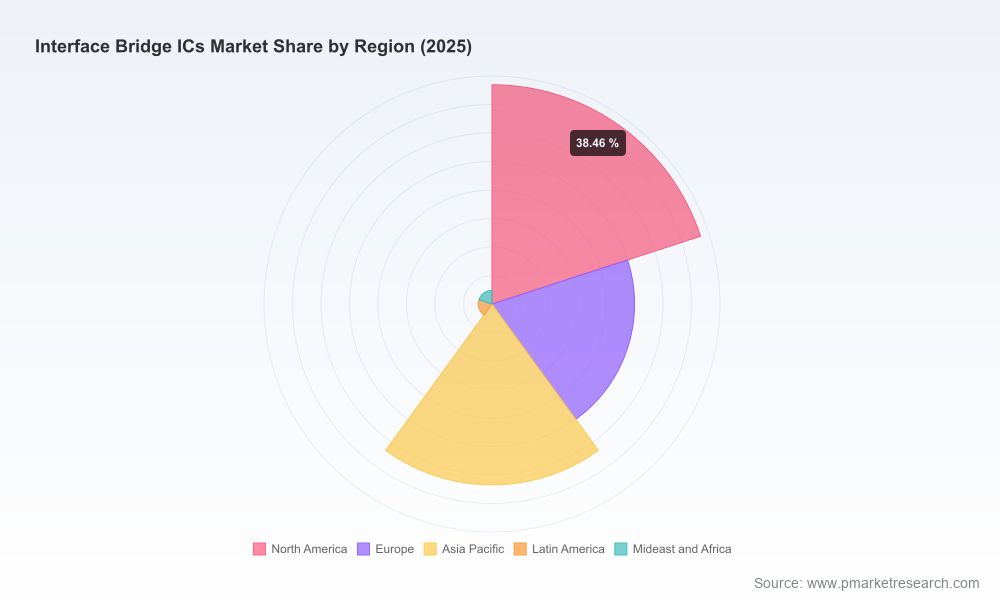

To preserve confidentiality of our proprietary modelling and to align with the “trailer” intent of this briefing, the detailed segment tables and vendor share metrics are available only in the full report.

Competitive dynamics — positioning and implications

The competitive landscape for interface bridge ICs is defined by a mix of global semiconductor leaders and specialist vendors. Each has a distinct playbook:

- Toshiba (Tokyo, Japan): Leverages system-level relationships in automotive and mobile to supply display, camera, HDMI bridge solutions and I/O expanders. Strategic implication: incumbency with Tier‑1s and strong system integration capability—good partner for suppliers seeking automotive entry but demanding of qualification and support commitments.

- Silicon Labs (Austin, USA): Focuses on USB‑to‑UART and driverless USB solutions with recent product iterations that emphasize USB‑C support, low power consumption, and simplified integration for IoT and embedded OEMs. Strategic implication: attractive partner for device makers accelerating Type‑C transitions and aiming to reduce driver burdens.

- FTDI (Glasgow, UK): Maintains leadership in high‑performance USB bridge silicon, with automotive‑grade offerings and Power Delivery support showcased at key trade events. Strategic implication: strong position for differentiated, automotive and embedded applications where reliability and PD integration matter.

- NXP Semiconductors (Eindhoven, Netherlands): Plays the bridge role within zonal controller and vehicle networking roadmaps, offering discrete solutions compatible with distributed vehicle architectures. Strategic implication: NXP’s integrations make it a natural partner in multi‑domain automotive architectures.

- Texas Instruments (Dallas, USA): Offers bridge components oriented around high‑speed data conversion and industrial robustness, positioning TI well for industrial and harsh‑environment use cases.

- Microchip Technology (Chandler, USA) and Holtek (New Taipei City, Taiwan): Focus on low‑to‑mid market segments with cost‑effective USB‑to‑serial bridges and serial conversion parts. Strategic implication: competitive pressure on margins at the low end, but also distribution breadth for rapid design wins.

Recent moves underscore the bifurcation of the market: Silicon Labs’ launch of an integrated USB‑C, driverless CP21xx class product family and FTDI’s prominent showcase of automotive-grade bridge devices and PD solutions are emblematic of a market where feature-driven differentiation (USB‑C, power delivery, and automotive qualification) is the primary route to defend pricing and attain design wins.

Market dynamics and risks

- Commoditization pressure: Low-cost alternatives and second‑source parts are increasingly used in high-volume consumer applications, limiting price elasticity for many vendors.

- Qualification and certification timelines: Automotive and industrial segments impose long lead times and costly qualification programs—this can lock suppliers into long contracts but raises barriers for entrants without domain experience.

- Supply chain distortion: Distributor arbitrage and gray‑market sourcing create operational risk for OEMs. Strategic procurement must balance cost and traceability when selecting suppliers.

- Technology convergence: As system vendors demand combined power/data features (Type‑C, PD), single‑chip integration becomes a differentiator—and a potential force for consolidation.

Strategic recommendations for 2026

For suppliers, OEMs, investors, and procurement teams, our synthesis yields practical, near‑term actions:

- Prioritize differentiated feature sets: Invest in driverless connectivity, Type‑C/PD integration, and certified automotive/functional safety stacks to sustain premium pricing and secure Tier‑1 relationships.

- Dual‑track go‑to‑market: Maintain a low‑cost product line for volume consumer wins while channeling R&D and customer‑engagement resources to premium, high‑margin verticals (automotive, industrial control, medical).

- Harden procurement and inventory strategies: Build qualified multi‑sourcing for key bridge families, require traceability in distributor contracts, and employ rolling safety stock during critical design‑win phases.

- Pursue targeted M&A: Buyers should shortlist assets that bring certification expertise, driverless USB stacks, or complementary transceiver IP—these are the most accretive in the near term.

- Leverage software to extend value: Offer firmware, reference boards, and certification support as bundled services—this both accelerates OEM adoption and creates stickiness that resists commoditization.

How PW Consulting supports execution

Our full Interface Bridge ICs Market study is explicitly structured to convert insight into action in 2026. Clients receive: a scenario‑ready financial model, vendor heatmaps tied to qualification timelines, a supplier due‑diligence checklist, communication templates for OEM negotiations, and a prioritized M&A target short list with integration and valuation guides. We couple this with a bespoke workshop option to align internal stakeholders on roadmap tradeoffs and supplier selection criteria.

Next step — where to get the full intelligence

This briefing highlights the strategic contours and the practical choices that will shape outcomes in 2026. For procurement teams that must lock down supplier strategies, product teams identifying bridge ICs for new BOMs, and corporate development groups sizing acquisition targets, the granular segment tables, vendor scorecards, and scenario models in the full report are essential. Accessing the complete study provides the precise segment-level demand, price‑curve assumptions, and vendor share breakdowns necessary to operationalize the recommendations above.

PW Consulting stands ready to present the full findings in a tailored briefing and to support implementation planning. Contact our research desk to schedule a guided walk-through of the model and to receive a version of the report with appendices matched to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Interface Bridge ICs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com