Phosphoric Acid Market: A Strategic Primer for 2026 Decision-Makers

As senior advisors at PW Consulting, we prepared this strategic introduction to our 2026 Phosphoric Acid Market study to orient C-suite and operational leaders to the near-term decisions that will determine competitive position through the end of this decade. The industry sits at the intersection of resource geopolitics, fertilizer economics, industrial-grade differentiation and emerging high-purity demand—making 2026 a pivotal year for capacity commitments, off-take strategies and ESG-driven portfolio reconfiguration.

Phosphoric Acid Market

Executive snapshot

- The study base year is 2025, with a historical window covering 2020–2025 and a forecast horizon extending 2026–2032.

- The global phosphoric acid market expanded steadily through the COVID recovery period and into 2025, reaching an estimated USD 36.5 Billion in 2025. Our baseline forecast assumes a compound annual growth rate (CAGR) of 4.7% over the forecast window, reaching approximately USD 50.1 Billion by 2032 under the central scenario.

- Market concentration is meaningful: the three largest producers account for a significant share of global merchant and integrated supply (CR3 ~42.5%), while the top five collectively control a majority (CR5 ~56.2%).

Why this research matters for 2026 decisions

Companies making investment, sourcing, and product-strategy decisions in 2026 face three overlapping inflection points:

Phosphoric Acid Market

- Supply-chain reconfiguration due to raw-material and intermediate feedstock constraints;

- Premiumization of product grades driven by electronics, battery, and food/pharma end markets; and

- Heightened regulatory and environmental constraints that materially affect operating cost and permitting risk.

Our report translates these inflection points into concrete decision frameworks—when to commit to greenfield capacity, how to price grade-differentiated product slates, and where to seek strategic partnerships to de-risk feedstock access. This is the actionable intelligence executives need before capital is allocated in 2026.

Phosphoric Acid Market

Market trajectory and what the numbers tell you

The market grew from roughly USD 29.5 Billion in 2020 to USD 36.5 Billion by 2025. Our modeled 4.7% CAGR reflects a mix of steady fertilizer demand, step changes in high-purity segments, and cyclical fertilizer pricing dynamics. The baseline path projects a continuation of moderate growth through 2032, with upside scenarios driven by accelerated adoption of battery-related phosphoric chemistries and downside scenarios tied to raw-material export controls or a sharper correction in agricultural commodity prices.

Crucially for 2026 planning, the aggregate numbers mask important structural differences between commodity merchant acid, integrated fertilizer supply, and small-but-fast-growing specialty grades. Our executive playbook quantifies these dynamics while preserving the commercial confidentiality of granular segment shares—insightful for strategy without disclosing the proprietary splits that competitors prize.

Key dynamics shaping 2026 strategic choices

- Feedstock and geopolitics: Continued phosphate rock export restrictions from major suppliers and the addition of phosphate rock to the EU Critical Raw Materials list have elevated perceived supply risk. Firms that secure long-term rock access or vertically integrate will gain durable advantage.

- Sulfuric acid cost volatility: Recent transport surcharges and higher sulfuric acid costs in key origin markets are prompting buyers to re-evaluate supplier footprints and localize critical intermediates. Expect procurement strategies to prioritize dual-sourcing and regional buffering.

- Environmental and permitting pressure: Phosphogypsum disposal constraints and stricter permitting regimes mean life-extension and optimization of legacy wet-process plants are now cost-effective alternatives to new builds—if corporations can navigate remediation obligations.

- Regulatory nuance: Evolving exemptions and tolerances—such as inert ingredient exemptions in certain jurisdictions—create windows for product innovation in antimicrobial and food-contact formulations, but also raise vigilance for cross-border compliance complexity.

Demand-side shifts and the premiumization of grades

Commodity-grade acid used in fertilizers remains the volume backbone, but differentiated demand is reshaping value pools. High-purity electronic and battery-grade phosphoric acid are drawing disproportionate investment as semiconductor, AI hardware and battery manufacturers seek local, low-impurity sources. Food- and pharma-grade streams maintain steady, quality-driven demand. For 2026 buyers and producers, the imperative is to match capital intensity with margin uplift—upgrading production trains where feedstock and water quality permit or securing contracts with premium offtakers to justify new purification units.

Competitive landscape: practical reading for strategists

The sector comprises integrated fertilizer majors, specialty-chemical firms, and emerging pure-play purified acid developers. Below we synthesize the strategic posture of core players—you’ll find detailed supplier scorecards and SWOT analyses in the full report.

- Prayon Group (Belgium) — Positioned at the high end with capabilities in purified and electronic-grade acid. Recent capital deployment to expand electronic-grade capacity signals an aggressive bet on semiconductor and AI-related demand; prime partner for technology-led grade differentiation.

- Jordan Phosphate Mines Company (JPMC, Jordan) — Running large integrated wet-process operations and expanding capacity through new sulfuric and phosphoric units. JPMC is a strategic supplier for regional fertilizer markets and a potential anchor for long-term merchant contracts.

- Arianne Phosphate Inc. (Canada) — Emerging as a battery-grade developer; the Quebec option for a purified facility is a high-signal move for North American high-purity supply that could become a regional secure source for battery chemistries.

- The Mosaic Company & Nutrien — North American fertilizer leaders whose phosphoric acid production is tightly linked to integrated fertilizer economics; effective at optimizing scale but exposed to agricultural cyclicality.

- OCP, PhosAgro, Ma’aden, EuroChem, ICL — Large integrated producers with strategic positions in merchant and upgraded product channels; their global footprint and feedstock access create both competitive advantage and geopolitical exposure.

- Innophos, Solvay — Specialty-grade producers focused on food, pharma and industrial segments; suited for partnerships where technical specifications and regulatory documentation are critical procurement criteria.

Recent project news underscores an industry in active reconfiguration: Prayon’s electronic-grade unit construction, JPMC’s multi-phase capacity projects and national-scale investments such as Egypt’s Abu Tartour initiative collectively signal supply-side modernization. These developments validate our view that 2026 is a window for strategic capacity plays—particularly in purified streams—but they also increase the importance of timing and offtake certainty.

Strategic implications and an actionable playbook for 2026

- Prioritize feedstock contracts and vertical options: Pursue long-term phosphate rock and sulfuric acid agreements, strategic equity in upstream projects, or JV structures to mitigate export restriction risk.

- Differentiate product portfolios: Map your customer base to grade elasticity and concentrate investment where premiumization yields durable margins—especially in electronics and battery sectors.

- Optimize legacy assets under stricter environmental regimes: Invest in process optimization, phosphogypsum management, and permit modernization to extend asset life while preserving community license to operate.

- Hedge price and availability risk cleverly: Use a mix of forward contracts, regional buffer inventories, and blended sourcing strategies to insulate downstream plants from intermediate price spikes.

- Scan for M&A and partnership windows: Mid-sized specialty players and regional producers with offtake relationships present high-leverage acquisition or partnership targets to accelerate entry into premium segments.

What our full report delivers (practical contents)

The full PW Consulting Phosphoric Acid Market study translates the macro narrative above into operationally useful deliverables, including:

- Proprietary demand-models by grade (commodity, purified, electronic, food/pharma) with scenario sensitivity to fertilizer cycles and high-purity adoption rates;

- Supplier scorecards that rank companies on feedstock security, ESG exposure, purification capability and capex runway;

- Capex mapping and project pipeline visualization through 2032, including timelines for commissioning risk;

- Regulatory impact matrices and a permitting risk dashboard tailored by major jurisdiction;

- Commercial playbooks for buyers and sellers that include contract templates, pricing levers, and transition timelines for upgrading product trains;

- Scenario-driven decision trees for greenfield vs. brownfield investment choices, and for pursuing vertical integration versus off-take contracts.

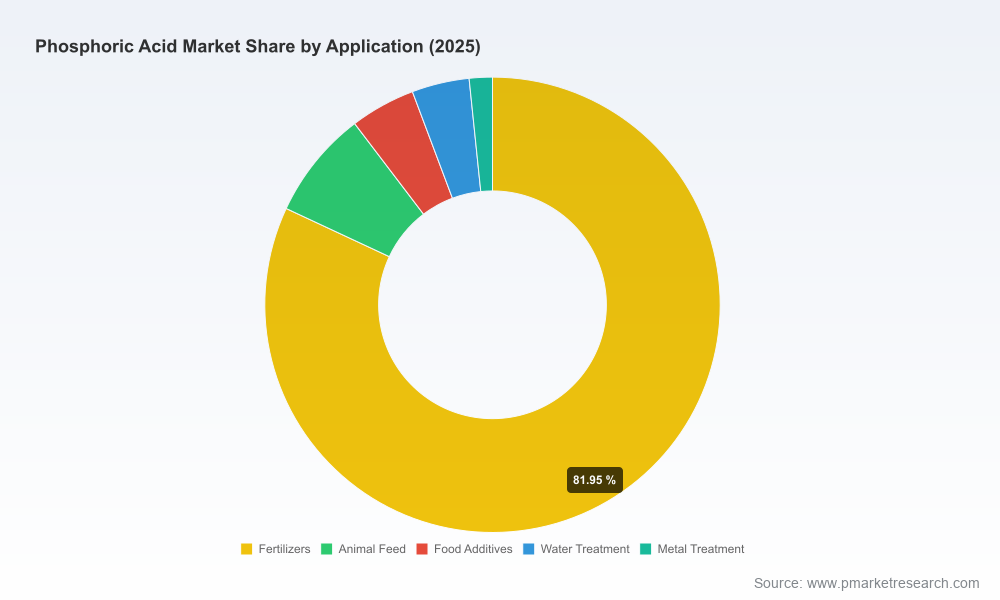

We intentionally withhold granular regional and application-level splits from this primer to preserve the competitive value embedded in our proprietary segmentation. The full report contains those detailed breakouts and the underlying data tables you will need to build business cases in 2026.

Conclusion: A narrow window for decisive action

As the market moves from volume-driven growth to a more complex landscape of grade-differentiated value pools, 2026 represents a strategic hinge year. Firms that secure feedstock, selectively upgrade to high-purity lines, and actively manage environmental liabilities will capture the most value over the forecast horizon. Conversely, firms that delay will face higher entry costs and constrained options as projects and offtake capacity lock up.

PW Consulting’s full study empowers executives with the granular data, supplier diagnostics, and transaction-ready playbooks to act in 2026 with conviction. For access to the complete dataset, regional and application-level segmentations, supplier scorecards and model assumptions, visit our report page or contact your PW Consulting representative to arrange a briefing.

For detailed analysis of this topic, please visit the official page:Phosphoric Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com