Breaking: Automotive Aftermarket Glass Market Set for Steady Growth

Cyber Security |

2026-06-01 11:08:34

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise yet incisive preview of our forthcoming Polytrimethylene Terephthalate (PTT) Market study. This briefing distills the research’s strategic value for corporate leaders planning capital allocation, commercial strategy, and sustainability pathways in 2026. It demonstrates the depth of our analysis while intentionally preserving the granular, proprietary segment-level intelligence that drives immediate commercial advantage — that detail is available in the full report.

Polytrimethylene Terephthalate (PTT) Market

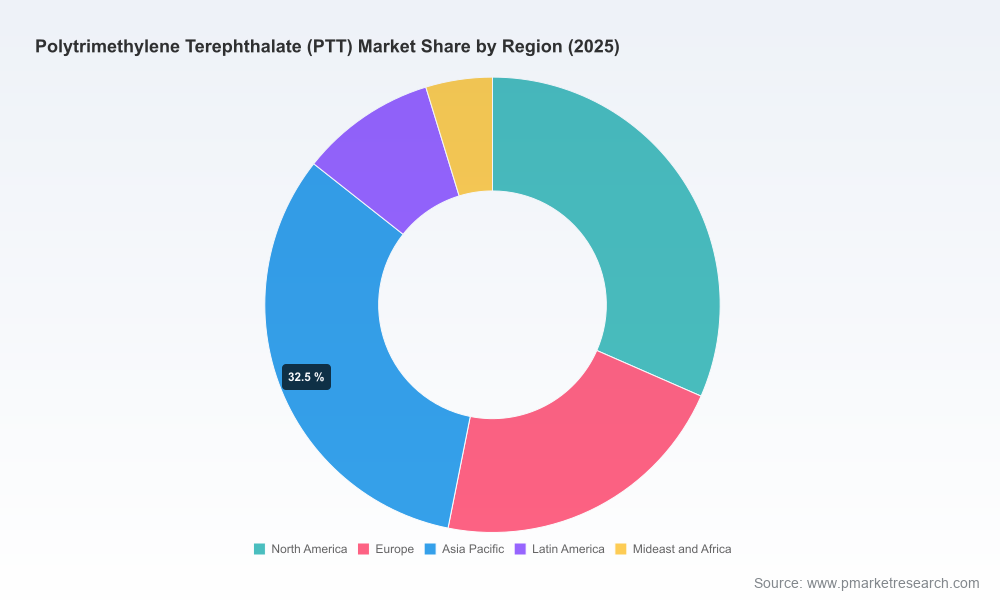

PTT is moving from a niche specialty polymer to a fast-evolving platform intersecting high-growth end markets such as advanced textiles, electronics substrates, and engineered materials. Our market model, built on 2020–2025 historical performance and forward-looking drivers, projects the global PTT market to grow at a compound annual growth rate (CAGR) of approximately 6.98% across the 2026–2032 forecast window. Measured on a dollar basis, the industry is expected to expand meaningfully from a base-year size in 2025 to materially higher levels by 2032 — a trajectory that supports renewed strategic focus on capacity investments, feedstock security, and differentiated product development.

Polytrimethylene Terephthalate (PTT) Market

Two structural features demand attention: first, the market exhibits limited top-tier concentration, leaving space for both incumbent innovators and agile new entrants; second, feedstock and regulatory dynamics are rapidly reshaping cost structures and sustainability claims. Together, these forces create a strategic runway for value capture — but also asymmetric risks for firms that delay action.

Polytrimethylene Terephthalate (PTT) Market

Feedstock economics are the proximate determinant of producer margins. In early 2026, feedstock-linked cost pressure from terephthalic acid and propanediol underpinned firmer producer offers, and bio-based PDO remains a significant cost and sourcing consideration. These dynamics translate into a dual imperative for PTT stakeholders: optimize feedstock flexibility (blend bio-based, chemically recycled, and fossil-derived streams where feasible), and institutionalize scenario-based pricing mechanisms in commercial agreements.

On the regulatory front, the European Union’s January 2026 finalization of mass-balance accreditation for chemically recycled polymers is catalytic. It permits producers to count depolymerized monomers toward recycled-content commitments, fundamentally changing the economics of recycled feedstocks and opening pathways to comply with tightening recycled-content mandates without full post-consumer streams. For PTT producers, the consequence is clear: early adoption of certified mass-balance systems creates market access and premium pricing potential, while laggards face commoditization risk.

Demand-side growth is driven by both established and emerging applications. High-performance apparel and engineered materials continue to expand, while electronics-related uses are gaining prominence. Importantly, these demand pockets vary in their willingness to pay for bio-based or recycled content, speed of qualification, and technical specifications — creating differentiated commercial strategies for PTT suppliers and compounders.

The sector is populated by a mix of global materials majors, regionally focused petrochemical groups, and specialized compounders. Market concentration metrics indicate a fragmented competitive environment, where the top few suppliers do not overwhelmingly dominate capacity — a structure that supports strategic collaboration and niche leadership.

Key players and their strategic positions:

Recent corporate developments underscore strategic themes: Teijin’s 2025 SOLOTEX® advances highlight application-led differentiation; PTTGC’s early-2026 progress on integrated biorefineries signals upstream control of bio-based chains; Toray and PTTGC collaboration on bio-adipic acid points to cross-polymer synergies; and Asahi Kasei’s plant decommissioning exemplifies the hard choices facing firms with legacy capital in a shifting raw-material regime.

The complete PTT Market study consolidates proprietary demand models, supplier benchmarking, and a deep dive into application economics. It contains:

Note: This preview is intentionally selective. The full report contains the granular regional and application-level breakdowns, detailed company revenue footprints, and executable spreadsheets that translate insights into investment and procurement decisions.

PTT is at an inflection point. The underlying market is growing at a robust mid-single-digit CAGR, with structural forces — feedstock dynamics, regulatory change, and application-driven premiumization — creating both urgency and opportunity for decisive leadership in 2026. Firms that combine disciplined capital allocation, feedstock and certification agility, and focused application strategies will capture disproportionate value as the market expands.

For teams seeking the full intelligence suite — including the granular segmentation, regional demand maps, supplier scorecards, and our proprietary financial models — the complete PW Consulting PTT Market report is available. It translates the market’s complexity into actionable choices for procurement, R&D, and corporate development leaders ready to move in 2026.

For detailed analysis of this topic, please visit the official page:Polytrimethylene Terephthalate (PTT) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com