Isotridecyl Alcohol (ITDA) Market — Strategic Preview for 2026 Decision‑Making

Executive snapshot

As PW Consulting’s lead industry analyst, I present a strategic preview of our new Isotridecyl Alcohol (ITDA) Market study — designed specifically to inform capital allocation, commercial strategy, and regulatory positioning for calendar year 2026. This preview synthesizes the most consequential findings without disclosing the proprietary, segmented datasets reserved for the full report. Use this briefing to align executive priorities with the highest‑impact opportunities and risks in the ITDA value chain.

Isotridecyl Alcohol (ITDA) Market

Macro picture you can act on

The ITDA market has seen steady expansion through the mid‑2020s. On a historical basis, the market grew from roughly USD 120 million in 2020 to about USD 162 million by the base year 2025, reflecting resilient demand across surfactants, lubricants, and industrial intermediates. Our model projects continued expansion through the forecast period (2026–2032), reaching approximately USD 255 million by 2032. That trajectory corresponds to a compound annual growth rate (CAGR) of 6.5% for the 2026–2032 forecast window.

Isotridecyl Alcohol (ITDA) Market

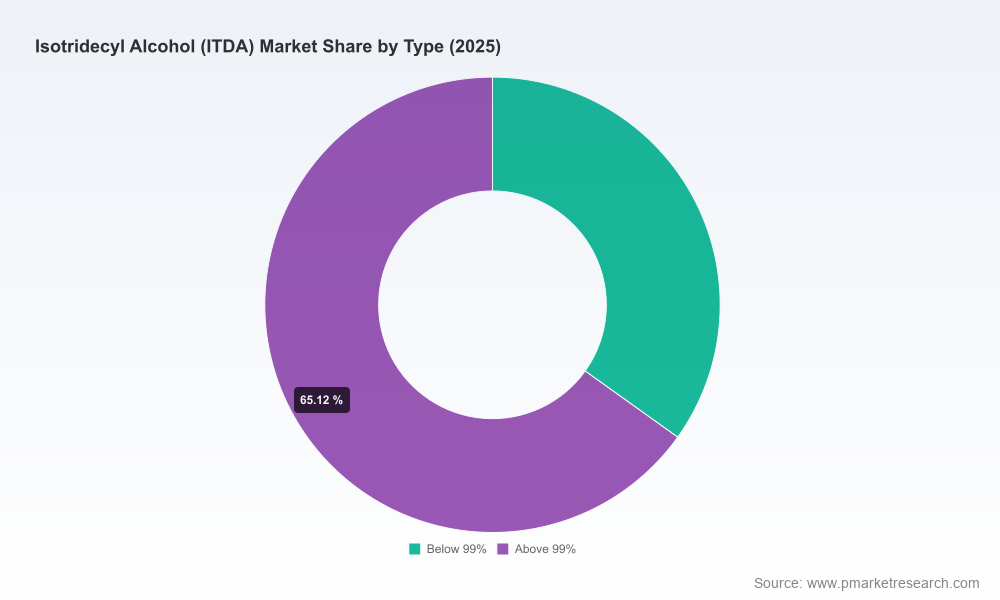

What these headline numbers imply for management teams: the market is large enough to justify targeted investments by specialty chemical players, yet sufficiently concentrated to reward strategic differentiation (product purity, odor profile, regulatory compliance) and disciplined commercial execution.

Isotridecyl Alcohol (ITDA) Market

Why this matters for 2026 decisions

- Investment prioritization: A mid‑single‑digit CAGR with clear pockets of premium demand suggests returning capital to higher‑margin, specialty segments (e.g., high‑purity grades, ester intermediates) will likely outperform broad commodity plays.

- Supply‑chain resilience: Upstream feedstock volatility and logistical disruptions are a primary near‑term risk. Firms that secure diversified feedstock sources or integrate upstream will enjoy meaningful margin stability.

- Regulatory preparedness: Accelerating VOC and chemical compliance regimes — especially under the EU Green Deal/REACH and tightened reporting expectations under U.S. frameworks — will raise the cost of non‑compliance and create premium demand for compliant ITDA variants.

- M&A and partnership timing: The market concentration metrics indicate significant market share held by a handful of global players. This creates strategic windows for bolt‑on acquisitions to capture scale in regional pockets or to acquire specialized formulations and supply agreements.

Demand drivers, near‑term catalysts and structural risks

Demand is driven by legacy end uses — surfactants for detergents and cleaners, lubricant additives, and resin/coating intermediates — but two structural themes dominate strategic planning:

- Sustainability and regulatory reformulation: Stricter VOC limits and lifecycle emission expectations are accelerating reformulation cycles in coatings and plastics. Buyers are demanding low‑VOC or REACH‑compliant grades, creating a premium tier.

- Downstream value capture: As formulators seek differentiated surfactants and specialty esters, suppliers who can offer consistent high‑purity grades, odor‑managed products, and technical co‑development will capture pricing power.

Primary risks include raw material price volatility, potential feedstock shortages tied to olefin markets, and regulatory developments that may restrict certain oxo alcohol applications absent reformulation. These are central to the scenarios we model in the full study.

Supply structure and competitive implications

The ITDA supplier base displays moderate to high concentration: the top three players control a significant share of global capacity, and the top five account for the lion’s share of production. That concentration matters for strategic buyers and new entrants alike — it affects negotiation leverage, spot availability, and the dynamics of capacity expansions.

Company positioning — what we observe (high‑level)

The market is populated by several incumbent multi‑national chemical producers and regional specialists. Each brings a distinct strategic posture:

- Evonik Industries AG — Emphasizes a high‑purity branded product (ELUCARE® TD) tailored as a feedstock for surfactants and specialty esters. Evonik’s strengths are formulation support and downstream integration into specialty chemicals portfolios.

- ExxonMobil Chemical Company — Markets a mass‑market, industrially robust Exxal™ 13 product. ExxonMobil’s scale and feedstock integration make it a reliable supplier for large formulators that prioritize continuity of supply.

- BASF SE — Offers C13‑rich alcohol grades positioned at the intersection of commodity and specialty applications. BASF’s advantage lies in its broad industrial customer base and capability to co‑develop intermediates.

- Sasol Limited — Produces a C13 alcohol derived from trimerized n‑butene (MARLIPAL® O13) marketed for its mild odor profile — a differentiator in consumer‑facing formulations.

- KH Neochem Co., Ltd. — A regional supplier with emphasis on raw material supply for plasticizers, surfactants and lubricants. KH Neochem offers flexibility for regional customers and niche applications.

- Dow Inc. — Offers a branded high‑purity iso‑tridecyl alcohol designed for specialty uses; Dow leverages global channels and application development capabilities to secure formulations wins.

For sourcing teams, this means supplier selection should weight product attributes (purity, odor, supply reliability) and the supplier’s capability to support reformulation under tightening environmental rules.

Regulatory and market friction items to prioritize

- EU Green Deal + REACH: Expect continuous tightening around emissions and use‑classification. Firms should conduct portfolio screening for REACH compliance and invest in registration or substitution strategies where required.

- U.S. reporting regimes: EPA TSCA reporting and data governance obligations are material for companies handling C11–C14 iso‑alcohols; ensure data readiness and traceability to avoid enforcement risk.

- VOC restrictions in coatings and plastics: These create a commercial advantage for low‑VOC or reformulated products and may limit demand for legacy grades in developed markets.

Tactical plays for 2026 (prioritized)

- Immediate (0–6 months): Perform a supplier risk audit focusing on feedstock sourcing, contractual exposure to price swings, and regional availability. Initiate pilot reformulation trials for key customer accounts exposed to VOC limits.

- Near‑term (6–18 months): Secure strategic off‑take or tolling agreements with one or two global suppliers to hedge supply risk. Launch a premium product development track (high‑purity, low‑odor, regulatory‑ready) and price it with clear value metrics.

- Medium term (18–36 months): Evaluate bolt‑on acquisitions to add regional capacity or proprietary formulations, and establish a roadmap for vertical integration where feedstock cost volatility materially threatens margin.

What the full PW Consulting report delivers

The full market study is built to convert insight into action. Highlights include:

- Proprietary historical and forecast market sizing (2020–2032) by region, type and application (note: detailed segment tables are accessible only in the full report).

- Scenario‑based outlooks that stress‑test demand and price under alternate regulatory and feedstock scenarios, including sensitivity analyses around VOC restrictions and olefin price shocks.

- Supplier scorecards and benchmarking across quality attributes, capacity, feedstock exposure, and strategic intent.

- Commercial playbooks for upstream integration, portfolio reorientation toward specialty esters, and customer co‑development approaches for detergent and coatings formulators.

- M&A heat maps and a prioritized target list (including regional specialists and technology‑owner profiles) aligned to defined strategic objectives.

- Detailed methodology and primary research notes, including interviews with incumbent producers, formulators, and regulatory experts.

How to use this preview

Consider this briefing the strategic trailer: it validates the direction and scale of opportunity, highlights the levers that matter for 2026 decision‑making, and identifies the near‑term tactical plays that deliver defensible advantage. To execute with conviction you will need the full segmented datasets, supplier‑level financial overlays, and the price‑supply scenarios contained in the paid report.

Closing

In markets like ITDA, information timing and granularity determine winner and also‑ran status. The market’s projected progression from a robust base in 2025 through a mid‑single‑digit CAGR to 2032 creates multiple strategic inflection points in the next 12–18 months. PW Consulting’s full ITDA Market report equips leaders to convert those inflection points into measurable value — from product strategy through M&A and regulatory compliance. For proprietary segment breakdowns, supplier models, and the complete scenario set that underpins the USD 162 million base year and the 6.5% forecast CAGR, request the full study on our publication page.

For detailed analysis of this topic, please visit the official page:Isotridecyl Alcohol (ITDA) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com