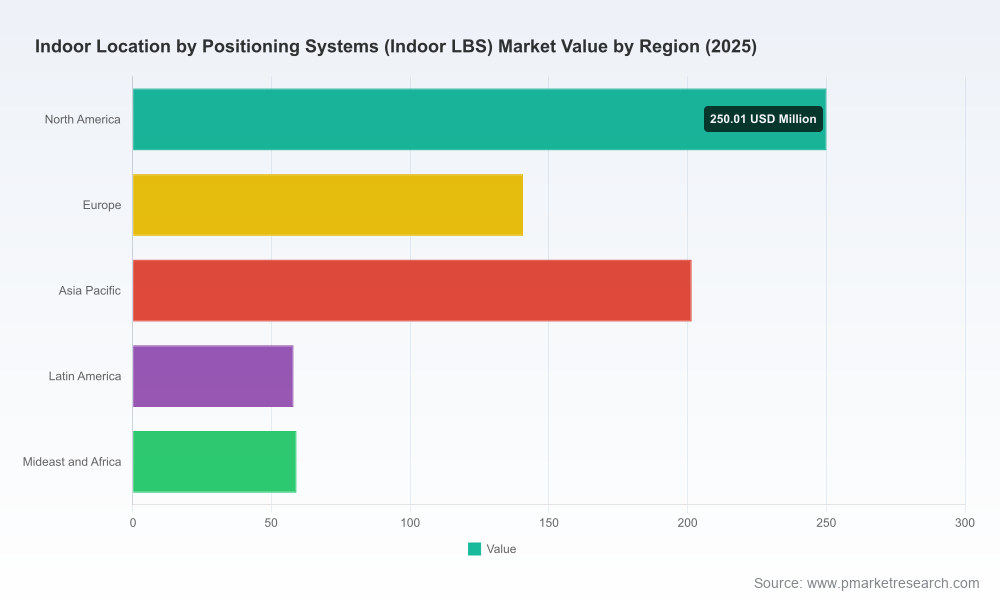

Indoor Location by Positioning Systems (Indoor LBS): Strategic Primer for 2026 Decision-Makers

As enterprises and public institutions plan capital and product roadmaps for 2026, Indoor Location by Positioning Systems (Indoor LBS) is moving from niche experimentation to scalable deployment. PW Consulting’s latest market study — with a 2025 base year and a forecast through 2032 — synthesizes the commercial, technical, and regulatory inflections that will determine winners and losers in the next planning cycle. This preview highlights the report’s strategic value for boards, CTOs, and corporate strategists while preserving the full depth and proprietary split data for subscribers.

Indoor Location by Positioning Systems (Indoor LBS) Market

Market Trajectory: What executives need to know

The Indoor LBS market is in a high-growth phase driven by converging forces: densification of edge compute and communications, maturation of centimeter- and sub‑meter positioning technologies, and enterprise demand for operational visibility across people, assets, and premises. Our modeling — using 2020–2025 historical data and a 2026–2032 forecast horizon — indicates an aggressive compound annual growth rate of 23.8%. By the 2025 base year the market size reached a mid‑three‑digit million-dollar level, and the projection shows the market scaling rapidly through the forecast window, reaching multiple billions in nominal revenue terms by 2032.

Indoor Location by Positioning Systems (Indoor LBS) Market

For decision-makers, the practical takeaway is straightforward: Indoor LBS is no longer a peripheral IT investment. With near‑term revenue and adoption trajectories accelerating, 2026 is a make‑or‑break year for moving from pilots to enterprise rollouts or for carving defensible niche leadership.

Indoor Location by Positioning Systems (Indoor LBS) Market

Why 2026 is an inflection year

- Standards and interoperability: Recent releases from industry bodies have clarified integration points and testing regimes for technologies such as UWB (Ultra‑Wideband). These updates materially reduce implementation ambiguity for vendors and integrators.

- Spectrum and infrastructure moves: Regulatory approvals toward terrestrial beaconing and dedicated spectrum assignments have broadened the feasible design space for indoor/outdoor continuity solutions, enabling new hybrid architectures.

- Commercial availability of advanced positioning platforms on major vendor roadmaps signals that precision indoor location will be a deployable capability for service providers and large enterprises in 2026 and beyond.

Technology inflection points — what to watch

- UWB and standardization: The maturation of UWB certification programs and successive core releases are unlocking richer device ecosystems and improving certainty around device interoperability — a prerequisite for broad enterprise adoption.

- 5G Advanced and distributed radio: Commercial launches of 5G Advanced indoor location services enable sub‑meter positioning at scale when paired with enterprise RAN and distributed antenna systems, creating new options for telco‑led indoor LBS offerings.

- Metropolitan beaconing and spectrum plays: Terrestrial, lower‑band beacon systems provide indoor/outdoor continuity and vertical‑scale coverage models that will reframe how emergency services, navigation, and device vendors approach resilience and backup positioning.

- Multi‑modal positioning stacks: The future is hybrid. Best practice architectures blend Wi‑Fi, BLE, UWB, cellular, inertial sensors, and map anchoring to manage cost, privacy, and accuracy tradeoffs across verticals.

Competitive landscape — strategic implications

The vendor landscape combines global platform players, specialist RTLS vendors, chipset suppliers, and mapping and services providers. Market concentration remains low to moderate: incumbency exists, but meaningful share is distributed among a range of specialists and large system integrators. That dynamic favors coalitions and ecosystems over single‑vendor dominance in the near term.

- Zebra Technologies — Strengths: deep heritage in RFID and BLE RTLS hardware and enterprise software stacks for retail, healthcare, and manufacturing. Strategic posture: leveraging hardware-to-cloud bundles that reduce deployment friction in asset‑intensive settings.

- HID Global — Strengths: moves into UWB‑enabled RTLS following targeted acquisitions; focus on industrial and smart factory asset tracking. Strategic posture: converting identity and access management relationships into location services revenue streams.

- Cisco Systems — Strengths: enterprise network integration and Wi‑Fi anchored positioning. Strategic posture: embedding location as a value‑add within campus networking, with clear advantages for existing Cisco customers and managed service models.

- Ericsson — Strengths: 5G Advanced indoor positioning capabilities and Radio Dot System integrations. Strategic posture: operator and neutral‑host deployments that target service providers and large campus environments.

- NextNav — Strengths: metropolitan beacon system building on lower‑band spectrum for 3D indoor/outdoor continuity. Strategic posture: spectrum acquisitions and field testing to create alternative location backplanes for emergency and commercial services.

- HERE Technologies, Google, Apple — Strengths: indoor mapping, navigation platforms, and ecosystem positioning services. Strategic posture: mapping and consumer/device integration that bridge consumer navigation with enterprise LBS use cases.

- Qualcomm — Strengths: UWB chipsets and FiRa‑aligned silicon. Strategic posture: enabling device vendors and OEMs to ship certified hardware that supports high‑precision positioning.

- CenTrak — Strengths: healthcare‑focused Wi‑Fi and BLE solutions. Strategic posture: deep vertical specialization with clinical workflows and regulatory compliance services.

Recent industry moves underline how vendor strategies are crystallizing: standards bodies are accelerating certification programs; key players are commercializing 5G‑based indoor positioning; and spectrum assignments and field trials are validating alternatives to purely network‑based architectures. For buyers, that means procurement teams should prioritize interoperability, roadmaps for standards compliance, and end‑to‑end operational capabilities over single‑metric vendor rankings.

Use cases and value levers

Indoor LBS is being deployed against a set of recurring enterprise needs: asset and inventory visibility, workforce safety and lone‑worker protection, patient and visitor navigation, operational process optimization in manufacturing and logistics, and enhanced customer experiences in retail and hospitality. Each use case has distinct accuracy, latency, privacy, and integration requirements — and these must drive architecture, not vice versa.

- Operational efficiency: location data reduces search times, informs dynamic routing, and supports process automation.

- Safety and compliance: real‑time location enables rapid emergency response and audit trails for regulated environments.

- Experience and revenue: proximity‑driven services and indoor navigation can unlock incremental customer engagement opportunities.

- Resilience: multi‑modal architectures and beaconing systems provide GPS backup and indoor/outdoor continuity for critical applications.

Deployment and commercial models

Enterprises should plan for mixed deployment models — cloud, on‑premises, and hybrid — depending on latency, privacy, and sovereignty needs. Commercial offerings range from pure SaaS subscriptions to appliance plus managed‑services bundles. Procurement teams must size total cost of ownership beyond hardware list prices, accounting for ongoing calibration, map maintenance, device lifecycle, and integration work.

Risk, regulation and interoperability

Regulatory and standards developments materially change implementation risk. Recent spectrum approvals and successive standards releases have reduced uncertainty, but operators and enterprises still face local regulatory variability, privacy compliance challenges, and liability questions for safety‑critical services. Interoperability remains the single biggest operational risk: projects that lock into proprietary stacks without credible migration paths risk premature obsolescence.

What PW Consulting’s full report delivers (practical highlights)

- Transparent methodology: end‑to‑end forecasting approach, assumptions, and scenario sensitivity for 2026–2032 planning.

- Actionable vendor intelligence: independent vendor profiles, capability maps, and decision frameworks tailored to procurement personas (CIO, Head of Facilities, Head of Safety, Head of IoT/OT).

- Technology deep‑dives: comparative assessment of UWB, BLE, Wi‑Fi, cellular/5G, beaconing, and hybrid stacks — with deployment playbooks and integration checklists.

- Commercial models and ROI templates: TCO and business case templates that non‑technical stakeholders can use to compare lease vs. buy, managed services vs. in‑house operations, and phased rollout scenarios.

- Implementation risk matrix: controls and mitigations for privacy, regulatory, and operational risks across common verticals.

- Roadmap and M&A insight: strategic options for ecosystem plays, partnership archetypes, and M&A signals to watch in 2026.

Note: This article intentionally omits the report’s granular regional, type, and vertical revenue splits to preserve the commercial value of the full research. Subscribers receive the complete segmental tables, competitor market shares, and downloadable financial models required for procurement and investment committees.

How to use this research in your 2026 planning cycle

- Board-level briefing: use the high‑level growth trajectory and industry shifts to align capital allocation and digital transformation priorities.

- Procurement and vendor selection: require vendors to demonstrate standards‑level compliance and provide clear interoperability roadmaps as part of RFPs.

- Pilot to scale gating criteria: define measurable KPIs (accuracy, uptime, integration cost, privacy compliance) that determine a pilot’s readiness for enterprise rollout.

- Partnership and M&A scouting: prioritize partners that complement your core assets (network providers for campus coverage; mapping vendors for navigation; RTLS vendors for asset‑heavy operations).

Conclusion — sharpen the decision lens for 2026

Indoor LBS is entering a commercial phase where timely strategic choices will compound over the next decade. The market’s high growth rate and the confluence of standardization, spectrum moves, and commercial product availability mean that 2026 is a pivotal year for converting strategic intent into operational capability. PW Consulting’s full report equips leaders with the revenue forecasts, vendor intelligence, technical playbooks, and decision frameworks necessary to act decisively — while protecting the detailed segment data for subscribers who require exportable models and procurement artifacts.

To obtain the full report, including segmental breakdowns, vendor market shares, and downloadable ROI templates, please visit our research portal or contact PW Consulting’s Indoor LBS practice directly.

For detailed analysis of this topic, please visit the official page:Indoor Location by Positioning Systems (Indoor LBS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com