Portrait Photography – Professional Headshots That Build Confidence and Credibility

Other |

2026-07-03 04:24:49

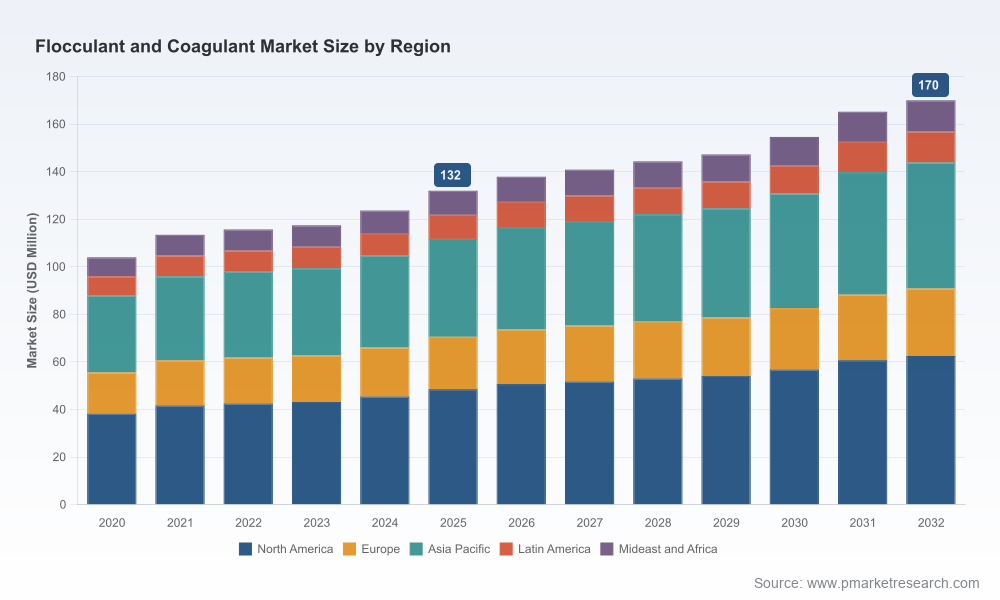

As PW Consulting’s Chief Industry Analyst, I present a focused strategic preview of our full Flocculant and Coagulant Market study — designed to inform critical 2026 investments, commercial plans, and M&A choices. The market has demonstrated steady expansion over the first half of the decade, and our modelling shows continuing growth through the 2026–2032 forecast window at a compound annual growth rate of approximately 3.95%. Under baseline assumptions, the global market is projected to rise from a mid-three-digit million-dollar level in 2025 to the high end of that band by 2032, reflecting a combination of regulatory-driven capex cycles, raw material volatility, and technology-led product displacement.

Flocculant and Coagulant Market

Timing: 2026 is a pivot year when legacy product portfolios and new regulatory standards collide — creating both risk and opportunity for suppliers, utilities, and industrial consumers.

Flocculant and Coagulant Market

Investment clarity: The report translates macro growth (multi-year market expansion and a c.3.95% forecast CAGR) into actionable near-term needs: incremental capacity, targeted product rollouts, and procurement hedging strategies.

Flocculant and Coagulant Market

Competitive positioning: Market concentration is meaningful but not prohibitive; the three- and five-firm concentration metrics indicate leaders retain influence while niche and regional players can still capture value through specialization.

Operational impact: Rising input costs and energy shocks are already changing dosing strategies, sludge management economics, and total cost of ownership calculations — critical inputs for CapEx and O&M planning in 2026.

We built our forecast from a detailed historical base (2020–2025) and project through 2032. The market’s trajectory is shaped by two structural vectors: stable, regulation-led demand in municipal water treatment and cyclical, application-dependent demand in industrial wastewater and mining. Although overall growth is moderate, the mix is shifting — low-dose high-value chemistries, bio-based formulations, and specialty mining flocculants are growing faster than commodity salts.

Regulatory pressure: Recent drinking water standards (notably U.S. EPA actions on PFAS) have initiated renewed investment cycles in treatment and monitoring equipment. This sustains baseline coagulant demand and unlocks opportunities for product differentiation that demonstrably reduce trace contaminants.

Raw material volatility: Q4 2025 saw steep ferric chloride pricing pressure that amplified supply-side risk. Concurrent constraints in iron ore and sulfuric acid markets, and intermittent logistics friction, create a volatile feedstock cost environment — pressuring margins unless mitigated through procurement strategies or product reformulation.

Energy and operating cost shocks: Utility price spikes in parts of Europe during 2024 accelerated adoption of low-dose regimes and process optimization measures that reduce sludge volumes and operational footprint — altering value propositions for chemical suppliers.

Sustainability and chemistry shift: EU and U.S. sustainability frameworks now favor biodegradable and bio-based chemistries. Leading suppliers are responding with targeted launches and pilot programs that meet both performance and lifecycle-carbon criteria.

The competitive field combines diversified chemical majors, specialty polymer manufacturers, and regional inorganic specialists. Recent strategic moves highlight a market in selective consolidation and portfolio realignment:

Kemira: Leveraging its broad inorganic and organic portfolio, Kemira is doubling down on sustainable chemistries and localized capacity expansions to secure municipal and utility contracts. Recent acquisitions and targeted production investments demonstrate a strategy focused on downstream integration and regional supply security.

SNF Group: As the global leader in polyacrylamide-based flocculants, SNF emphasizes scale in water-soluble polymers and R&D in next-generation macromolecules — positioning itself to defend industrial and municipal channels through technical superiority and global footprint.

Solenis: Through recent asset acquisitions, Solenis is building a stronger mining-flocculant franchise. The company’s strategy is to capitalize on specialized brands and migrate them into larger integrated commercial platforms.

Ecolab/Nalco, BASF, Veolia, and SUEZ: These players operate at the intersection of chemical supply and systems integration. Their go-to-market blends product sales with bundled services, digital dosing, and lifecycle contracts that shift value capture away from unit sales toward service margins.

Regional specialists and inorganic suppliers (including several mid-market players): These firms continue to serve price-sensitive or regulation-driven local pockets, but their window for scale advantages depends on execution of cost control and differentiation via service or specialty grades.

For suppliers: Prioritize portfolio mixes that balance commodity salt volumes with higher-margin specialty flocculants and bio-based formulations. Invest selectively in capacity where regulatory-driven demand and feedstock access converge.

For utilities and industrial end-users: Re-evaluate procurement frameworks to include lifecycle TCO, sludge disposal economics, and resilience to feedstock price spikes. Consider long-term offtake arrangements or joint investments in localized production to stabilize supply and pricing.

For private equity and strategics: Identify bolt-on targets that provide either differentiated chemistries (bio-based, low-dose) or advantaged local production footprints. The market’s moderate concentration creates room for roll-up strategies that combine technical, regulatory, and distribution assets.

For technology and service providers: The shift to bundled service models and digital dosing creates opportunities for partnerships with chemical suppliers, positioning innovators as gatekeepers for efficiency-linked premium contracts.

Our full study is structured for decision-makers who need executable outputs, not just descriptive narrative. Core deliverables include:

A calibrated market-sizing model (2020–2032) with scenario toggles (baseline, downside commodity shock, regulatory acceleration) to quantify demand and revenue implications.

Price and margin sensitivity analysis tied to key raw materials and energy inputs, including an indexed price deck that reflects observed Q4 2025 stress points.

Supply-demand maps and capacity-outlook by technology family, with plant-level cost benchmarking and utilization thresholds to evaluate expansion needs.

Commercial playbooks for municipal, industrial, and mining segments — covering pricing, contracting, digital enablement, and service bundling strategies.

Regulatory impact matrix and compliance roadmaps that translate recent PFAS and sustainability frameworks into near-term capex and O&M actions.

Competitive scorecards and M&A heatmaps highlighting targets for consolidation, capability tuck-ins, or geographic expansion.

Practical tools: negotiation checklists, procurement hedging templates, and pilot evaluation frameworks for new chemistries.

90-day: stress-test supply contracts against raw material price scenarios; initiate pilot testing for low-dose and bio-based chemistries with quantifiable sludge and energy savings metrics; update price escalation clauses.

12-month: redeploy commercial resources to capture regulatory-driven municipal tenders, finalize strategic partnerships for localized feedstock or tolling arrangements, and evaluate selective capacity or capability acquisitions aligned with our M&A heatmap.

Our synthesis combines rigorous bottom-up market modelling with primary intelligence on recent asset moves, product launches, and input-cost shocks. We emphasize decision-readiness: every qualitative driver in the study maps to a numeric implication in the financial model and to a tactical recommendation for procurement, R&D, or M&A. Importantly, while this preview surfaces high-value findings, the detailed segmentation, company-level revenue breakdowns, and proprietary price decks are preserved in the full report to support confidential client analyses.

For executive teams evaluating 2026 budgets or strategic initiatives, the full PW Consulting Flocculant and Coagulant Market report provides the actionable intelligence required to prioritize investments and mitigate downside risk. Access to the complete dataset and scenario tools is available through our subscription or as a standalone advisory engagement — contact PW Consulting to arrange a tailored briefing and receive the models behind this strategic preview.

For detailed analysis of this topic, please visit the official page:Flocculant and Coagulant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com