Understanding the Benefits of IPTV for Today's Connected Viewers

Other |

2026-07-07 23:11:03

As governments, utilities, and capital providers reassess their 2026 investment roadmaps, biomass power generation re-emerges as a strategically nuanced option: mature in technology, dynamic at the supply-chain level, and materially affected by policy design and grid constraints. PW Consulting’s new market study (base year 2025, historical 2020–2025, forecast 2026–2032) models market-scale evolution under multiple regulatory and supply scenarios and shows a steady compound annual growth rate of 5.3%. The global market — measured in USD billions — expands meaningfully from the early-2020s baseline through the early 2030s, but with episodic softness driven by policy, interconnection and feedstock cycles. This introduction explains why the study matters to corporate decision-makers in 2026, what actionable insights the full report contains, and how to prioritize next moves without revealing the fine-grain segmentation reserved for subscribers.

Biomass Power Generation Market

A complementary low‑carbon dispatchable option: Biomass plants can provide baseload or flexible firming to balance variable renewables. For buyers seeking firm renewable profiles or for projects exposed to capacity and ancillary market dynamics, biomass remains among the limited options that combine large-scale dispatchability with renewable fuel qualification under many regimes.

Biomass Power Generation Market

Policy levers create asymmetric value windows in 2026: Technology‑neutral incentives and investment tax credits—structured at small per‑kWh rates—materially change project IRRs for assets that meet prevailing wage and other eligibility gates. The study models these policy levers across jurisdictions and quantifies the sensitivity of developer returns to policy design and compliance costs.

Biomass Power Generation Market

Supply-chain and fuel security are strategic rather than operational problems: Pellet production, densified fuel logistics, and long‑haul maritime movements underpin project viability. Recent, large‑scale pellet production milestones and transoceanic deliveries underscore industrial-scale logistics’ importance; PW’s report provides fuel-supply stress tests for senior management and procurement teams planning multi-year off‑take commitments.

Grid access is a key gate: Interconnection backlogs in several major markets now exceed realistic build-out horizons for new plants. Our scenario analysis quantifies the value of early queue accession, repowering of existing sites, and hybridization options (co‑firing, flexible thermal plus storage) as practical mitigants to queue risk.

Using 2025 as the base year, our topline sizing shows the market expanding from a mid‑tens of billions (USD) in the early 2020s to a projected figure in the low hundreds of billions by the end of the study horizon, driven by a mix of capacity additions, higher utilization in regions that qualify biomass as renewable, and price inflation in energy markets. The modeled 5.3% CAGR reflects the compound effect of these drivers. Crucially, the path is non‑linear: the forecast includes short periods of market softness reflecting regulatory uncertainty and temporary supply constraints. Executives can use the timing windows in the report to optimize capital deployment and capture policy arbitrage.

Transparent, reproducible market sizing and forecast model (historical 2020–2025; forecast 2026–2032) with scenario toggles for policy, feedstock cost, and interconnection lead times.

Fuel-supply playbook: off‑take structuring templates, counterparty risk matrices, and logistics optimization for densified and loose biomass streams—presented as contract clauses, staging strategies, and contingency plans.

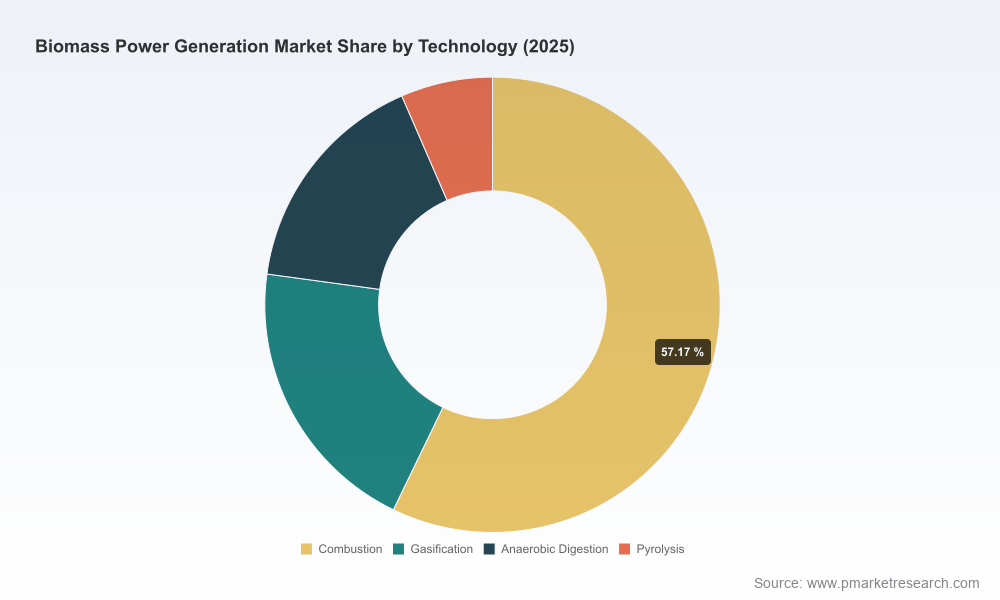

Technology and CAPEX/OPEX benchmarks for combustion, gasification and anaerobic pathways, plus modularity and retrofit cost curves to assess repowering and hybridization choices.

Regulatory scenario library: modeled impacts of tax credits, CfD-style mechanisms, carbon intensity accounting changes and low‑carbon fuel standards across major markets—mapped to project-level economics.

Commercial due diligence toolkit for M&A and JV activity, including valuation sensitivity matrices, play-by-play integration risks, and a shortlist of value creation levers for different deal archetypes.

Operational risk dashboards: pellet and feedstock price stress tests, workforce and logistics labor-risk triggers, and interconnection queue heatmaps (red/amber/green) for developer prioritization.

Note: As per our “trailer” approach, the report demonstrates the methodology and sample outputs in ways that allow buyers to validate quality, while detailed regional and application splits are available only in the full report and dataset.

The market structure is moderately concentrated at the top: a small set of integrated producers, large utilities and OEMs capture a material share of capacity and supply‑chain control. PW’s analysis triangulates public disclosures, project pipelines and recent corporate milestones to produce a POV on strategic posture.

Drax Group: An archetype of vertical integration — large‑scale pellet production married to utility‑scale offtake. Their recent production milestones and transatlantic shipments underline the strategic premium of owning feedstock logistics when demand is global. For competitors, Drax demonstrates both the opportunity and difficulty of scaling a captive supply chain.

ACCIONA Energía and regional developers: Project developers that combine EPC and O&M capabilities are accelerating grid‑connected projects. Recent grid connections show how developers can win local permitting and community engagement advantages; they also highlight the need for tight cost control during commissioning.

Industrial owners and integrated forest companies (e.g., Rayonier Advanced Materials): These actors leverage industrial symbiosis to convert process residues into on‑site generation or local exports. Their strategic edge is securing low incremental feedstock costs and co‑location logistics.

OEMs and systems integrators (Mitsubishi Heavy, Babcock & Wilcox, Siemens Energy, GE Vernova, ANDRITZ): Their competition centers on efficiency, retrofitable modularity, and lifecycle service contracts. Recent project deliveries confirm demand for proven, turn‑key systems and aftermarket services.

Large utilities and energy groups (Engie, Vattenfall, Ørsted): These players deploy biomass as part of broader renewables portfolios and emphasize portfolio-level emissions accounting and offtake structuring—for example, combining biomass with PPAs and CfDs to stabilize revenues.

The competitive implication for 2026: incumbents with integrated supply chains and access to policy levers will continue to defend margin pools; mid‑tier players can win by specializing (fuel processing, regional logistics, retrofit services) or by partnering with capital that understands interconnection and long‑dated revenue risks.

Capture policy windows but price in compliance: Technology‑neutral production and investment credits materially improve project economics when assets meet administrative requirements. Structuring teams should build compliance timelines and wage/benefit verification into their project schedules to avoid retroactive disqualification.

Hedge feedstock and logistical exposure: Given recent industrial-scale pellet production expansion, securing multi‑tier supply (captive production + third‑party offtakes + regional buffer stock) will reduce downside risk from episodic price spikes and port/logistics disruptions.

Prioritize interconnection and site reuse: With queue backlogs and grid constraints, repowering existing thermal sites or co‑locating on brownfield sites with established grid access can accelerate time to market and reduce permitting friction.

Design for optionality: Investments that allow co‑firing, partial electrification of thermal processes, or integration with carbon management open more revenue pathways as policy evolves.

Adopt a staged capital allocation: Move from optionality to commitment via milestone‑based capital tranches tied to interconnection milestone and supply contracts.

Pursue targeted M&A for supply-chain control: For organizations seeking scale, focus on bolt‑on acquisitions that provide feedstock processing, local logistics capability, or offtake diversity rather than broad, high‑capex greenfield bet‑the‑company projects.

Stress-test project economics under at least three regulatory outcomes and two fuel‑price scenarios; embed these into sanctioning thresholds and covenant language for project financing.

Invest in commercial capabilities: Structured finance, origin/source verification, and market access teams will deliver outsized returns relative to incremental plant efficiency improvements in this horizon.

The study is built to be used by transaction teams, corporate strategy units, and asset operators. It converts high-level market dynamics into decision-grade outputs: project-level NPV sensitivities, supplier and counterparty scorecards, and an executable 12‑month transition plan for organizations pursuing biomass expansion. We intentionally present rich methodology and sample outputs in the public summary while retaining the granular regional and application splits for subscribers—this keeps the value proposition clear and ensures competitive confidentiality for our clients.

Executives preparing capital allocation, M&A, or large‑scale procurement decisions in 2026 should request the full PW dataset and scenario model to run project- or portfolio-level tests. The dataset contains the full regional and application segmentation, policy‑by‑jurisdiction impact matrices, and the quantitative scorecards referenced above. Given the market’s uneven growth cadence and dependency on policy and grid access, early access to these granular levers allows teams to convert uncertainty into competitive advantage.

For detailed analysis of this topic, please visit the official page:Biomass Power Generation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com