IO-Link Market 2026: Strategic Signals for Decision Makers — A PW Consulting Preview

Executive summary

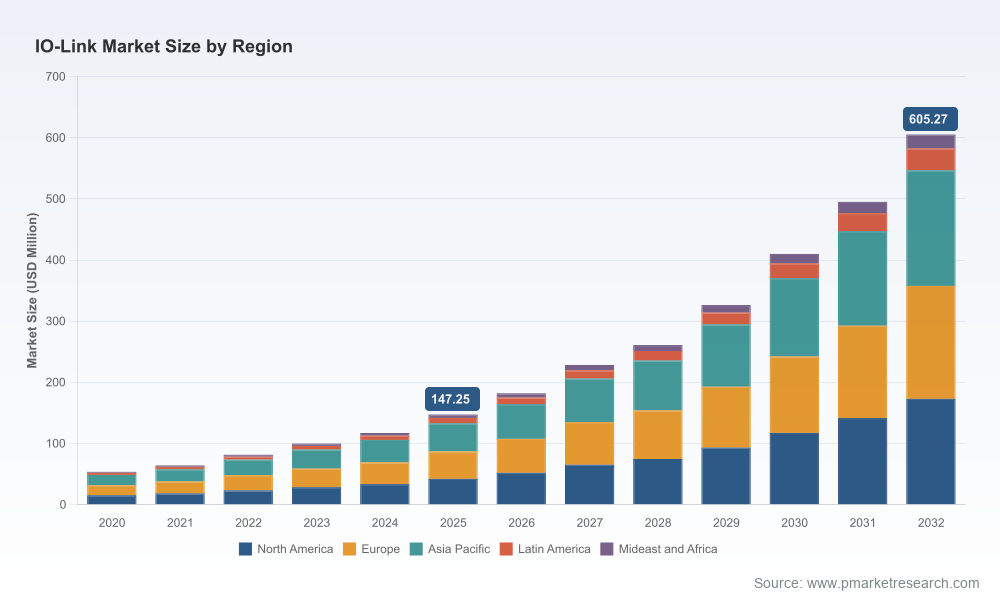

As industrial automation accelerates toward greater connectivity and software-defined operations, IO-Link has emerged as a pragmatic enabler of device-level intelligence. PW Consulting’s IO-Link Market study — built on a 2020–2025 historical base and projecting through 2032 — demonstrates that IO-Link is transitioning from niche connectivity to a mainstream element of control architectures. The market expanded rapidly in the first half of the decade and, with an expected compound annual growth rate (CAGR) of 22.54% from the 2025 base year, is projected to multiply several-fold by the end of the forecast period.

IO-Link Market

This preview outlines the strategic value of the full report for executives making 2026 decisions. It surfaces the macro trajectory, the inflection points that will shape supplier strategies and buyer economics, and the types of tactical actions that will protect and create value in 2026 — while intentionally withholding granular segment and regional breakdowns to preserve exclusive insight available in the full study.

IO-Link Market

Market trajectory and macro dynamics

PW Consulting’s topline view captures a steep growth profile: the market scaled from a modest base in 2020 to a substantially larger industry footprint by 2025, and our forecast shows continued acceleration into the early 2030s. The near-term jump between the 2025 base and the 2026 projection underscores a market entering a commercialization phase driven by three reinforcing dynamics: cost-of-integration economics, standardization around safety, and broadening device and semiconductor support.

IO-Link Market

- Cost-of-integration: Field-proven cases now quantify significant labor and wiring savings when IO-Link replaces traditional point-to-point wiring and analogue I/O. Manufacturers who move quickly can realize material reductions in per-point installation cost, reducing both upfront CAPEX and recurring maintenance expense.

- Standards and safety: The official certification of the IO-Link Safety specification and the designation of a formal test center have removed a major adoption barrier for safety-critical applications. Certification events and interoperability plugfests in 2025 validated multi-vendor strategies and accelerated readiness for safety-capable devices.

- Component and platform maturity: Semiconductor suppliers and transceiver manufacturers have broadened the ecosystem, enabling smaller OEMs and sensor specialists to offer IO-Link-enabled products without building all IP in-house. This supplier-layer maturation reduces time-to-market for integrated solutions.

Why this matters for 2026 strategic decisions

For corporate leaders — whether in manufacturing, automation supply, system integration, or investment — 2026 represents a critical pivot year. The combination of rapid market growth and recent standardization milestones turns what was previously a technology evaluation into a procurement and portfolio decision with measurable ROI within typical program timelines.

- Procurement and supplier selection: Buyers must re-calibrate vendor scorecards to weight IO-Link readiness, interoperability proofs, and safety certification roadmaps alongside price and service levels. Delaying re-evaluation risks higher retrofit costs and lost benchmarking data.

- Product roadmaps and R&D investments: OEMs of sensors, actuators, and I/O modules should accelerate IO-Link integration on roadmaps or secure ODM partnerships. Faster integration yields channel advantages as machine builders demand "plug-and-proven" IO-Link components.

- Systems and software play: Control-platform vendors and IIoT software suppliers must define clear value propositions for IO-Link data — from predictive maintenance to digital twin fidelity — and map those services to monetizable outcomes.

- M&A and partnership strategies: Given a market that remains far from fully consolidated, strategic acquisitions, minority investments, or distribution partnerships can shortcut capability gaps in device libraries, safety testing, or regional certification.

Competitive landscape — categories and companies to watch

The ecosystem is heterogeneous: global automation giants, specialized sensor OEMs, semiconductor innovators, and connector/fieldbus specialists each play a distinct role. Market concentration is moderate, with leading groups collectively holding a substantive but not dominating share — an environment that rewards both scale and focused specialization.

- Automation platform and system integrators: Large automation vendors are integrating IO-Link masters and device support into broader control platforms. Watch firms that can bundle IO-Link into PLC/edge strategies and offer migration tools for legacy I/O.

- Sensor and device OEMs: Established sensor manufacturers are moving quickly to ensure IO-Link compatibility across key product lines. Their advantage is channel trust and installed-base replacement cycles.

- Semiconductor and transceiver suppliers: Companies providing the silicon and transceiver IP are enabling a wave of new entrants and lowering the cost of entry for smart devices.

- Fieldbus/connectivity specialists and ecosystem enablers: Providers of masters, hubs and certified interoperability test services are central to multi-vendor deployments and to reducing integration risk.

Among the companies in this ecosystem, some are best watched for platform plays, others for device breadth, and several for enabling technologies (semiconductor IP, masters, certification services). The full report profiles the capabilities, go-to-market approaches, and strategic options for the market’s most consequential players — helping executives prioritize partner and procurement lists for 2026.

Recent industry milestones that change actions in 2026

- Certification and interoperability: The official certification of the IO-Link Safety specification and the first designated safety test center mark a shift from "emerging" to "approved" for safety applications. This reduces adoption friction in sectors where safety validation was previously a bottleneck.

- Community-driven validation: Record attendance at interoperability events and expanded certification centers reflect faster vendor alignment and shorter lead times for certified devices.

- Economic evidence: Published field data quantifying per-point labor savings and the demonstrable cost-effectiveness of multi-port masters provide procurement teams with quantifiable ROI levers to use during vendor negotiations.

What the PW Consulting IO-Link Market report delivers (practical contents)

The full study is designed as an operational toolset for strategists and practitioners. Highlights include:

- Topline market sizing and a year-by-year projection through 2032, with scenario analyses reflecting different adoption speeds.

- Demand-driver modelling linking labor, infrastructure and regulatory variables to adoption curves and ROI timelines.

- Vendor assessment frameworks and scorecards that evaluate technical capability, certification readiness, channel strength, and scale.

- Go-to-market playbooks for device OEMs, automation platforms, and system integrators — including recommended pricing and bundling approaches.

- Deployment and retrofitting decision tools for asset owners: build vs. buy matrices, TCO models, and pilot-to-scale roadmaps.

- Risk register and mitigation strategies covering supply-chain constraints, interoperability risks, and certification timelines.

- Use-case exemplars (e.g., machine tools, handling & assembly, intralogistics, packaging) that translate technical benefits into measurable KPIs and payback periods.

To preserve the competitive value of the dataset, the report intentionally concentrates detailed regional and segment splits, supplier-specific revenues, and certain tactical benchmarks within the members-only content suite.

How executives should act in 2026 — a prioritized checklist

- Immediate (0–3 months): Run a supplier audit to map current and near-term device roadmaps against IO-Link compatibility and safety certification status. Use procurement leverage to require interoperability proofs for 2026 bids.

- Near-term (3–9 months): Launch pilot projects focusing on high-return use cases identified in the report’s ROI models. Target pilots that can be scaled within 12 months and that validate both cost and data-value hypotheses.

- Strategic (9–18 months): Decide on platform plays — whether to partner, acquire, or license transceiver/IP technology — depending on whether your core differentiator is hardware, software, or systems integration.

- Organizational: Invest in certification and test-lab capabilities or partner with designated test centers to shorten time-to-certified-product and reduce go-to-market friction.

Conclusion — why PW Consulting’s IO-Link research matters in 2026

The move from experimental deployments to certified, multi-vendor IO-Link ecosystems redefines what it means to compete in device-level automation. Firms that align procurement, product roadmaps, and channel strategies to this transition will capture disproportionately more value as the market expands. PW Consulting’s IO-Link Market report equips leaders with the data, scenarios, and executable playbooks required to make those choices with confidence in 2026.

For a complete view of the datasets, supplier profiles, and actionable templates referenced in this preview, access the full report and member resources on our website. The detailed segment and regional breakdowns, supplier-specific assessments, and downloadable implementation tools are available exclusively there.

For detailed analysis of this topic, please visit the official page:IO-Link Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com