Adjustable Bed Base and Bed Market Dynamics: Key Drivers and Restraints

Other |

2026-04-22 10:23:13

As companies prepare capital allocation, supply-chain redesigns, and product strategy refreshes for 2026, accurate visibility into the float glass market’s trajectory is no longer optional — it is strategic. This preview of PW Consulting’s comprehensive Float Glass Market study synthesizes the macro trajectory, competitive dynamics, regulatory inflections, and the operational levers that will determine winners and losers over the 2026–2032 horizon. It is intended as a tactical roadmap for executive teams planning near-term investments, M&A, pricing plays, and decarbonization pathways.

Float Glass Market

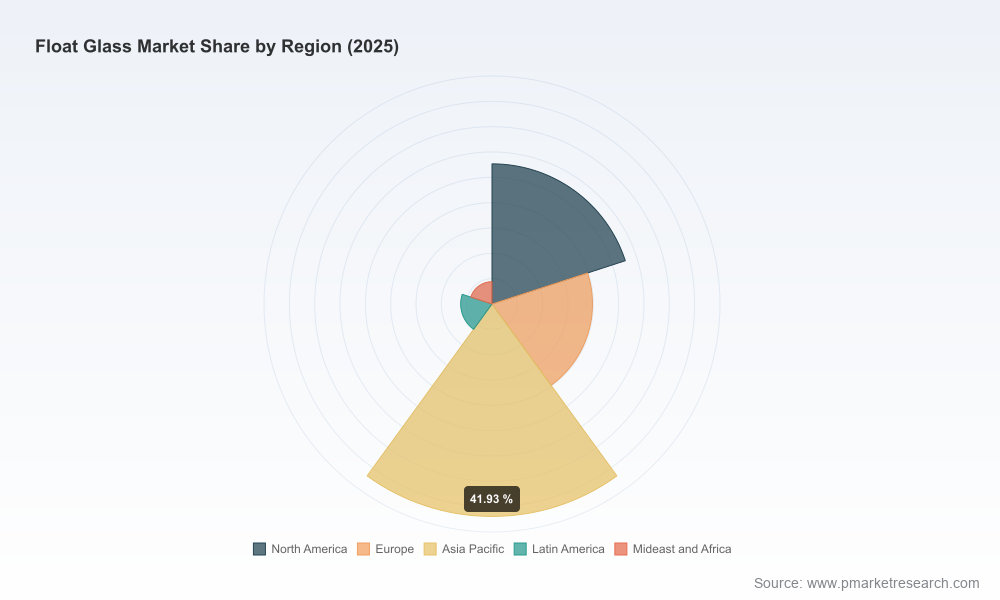

Between 2020 and 2025 the global float glass market more than expanded by half in nominal terms, rising from an approximate USD 113.6 Million in 2020 to a base-year (2025) valuation of about USD 172.3 Million (USD, Million). Our forecast models, driven by demand recovery in construction and automotive glazing, increasing solar-glass adoption, and gradual product premiumization, project the market to grow to roughly USD 254.1 Million by 2032. The modeled scenario set reflects an average compound annual growth rate of 5.8% through the 2026–2032 forecast window.

Float Glass Market

These topline figures mask important structural shifts: value is increasingly concentrated in higher-margin specialty products (coated, solar-integrated, and energy-efficient glazing) and in production footprints tied to local content preferences and trade-policy sensitivities. For 2026 decisionmakers, the market is large enough to justify both brownfield capacity optimization and selective greenfield projects — but timing, technology selection, and tariff exposure will determine return on invested capital.

Float Glass Market

Investment timing and location: With cost inflation (notably soda ash and silica sand) and energy tariffs exerting upward pressure on unit costs in early 2026, the window for economically attractive greenfield capacity is narrowing in regions with high input-cost volatility. Our report quantifies the sensitivity of unit operating cost to raw-material and energy changes and offers break-even timelines for new lines under multiple energy-price scenarios.

Trade and regulatory risk management: Final determinations in trade investigations completed in early 2026 have already shifted sourcing economics for several buyer groups. The full study provides a tariff-exposure matrix, scenarios for retaliatory or defensive trade measures, and mitigation options — from contractual hedges to nearshoring strategies — that are actionable in 2026 board cycles.

Product and margin optimization: Premium segments (solar, coated, energy-efficient glazing) are outpacing commodity float in margin expansion. The report contains pricing-elasticity curves and commercialization playbooks designed to help manufacturers quantify the uplift from product mix shifts and identify the minimal technology upgrades required to access premium channels.

Decarbonization and ESG as value drivers: Early adopters of low-carbon technologies (electric furnaces integration, green hydrogen feedstocks, and waste-heat recovery) are already securing premium contracts in key markets. We model payback periods for common decarbonization investments under prevailing 2026 energy and carbon-pricing assumptions.

Robust market sizing & forecast framework: Transparent methodology covering historicals (2020–2025) and scenario-based forecasts for 2026–2032, with build-ups by demand driver and product archetype. Forecast sensitivity to energy, raw-material, and trade-policy shocks is explicitly modeled.

Plant-level economics and benchmarking: A comparative cost curve across equipment vintage, furnace technology, and location, enabling operators to benchmark OPEX and CAPEX and prioritize retrofit vs. replacement investments.

Supply-chain and raw-material risk mapping: Detailed supplier concentration analysis, logistics cost stress-testing, and mitigation strategies (alternative sourcing, long-term off-take, vertical integration scenarios).

Trade, regulatory, and tariff playbooks: Country-level exposure matrices, scenario templates for tariff shifts, and tactical actions (e.g., contractual clauses, strategic stockpiling, or capacity reallocation) tailored for 2026 political calendars.

Commercial and pricing toolkits: Price-index models, channel-margin ladders, and tender-optimization templates for selling into construction, automotive, and renewable-energy markets.

M&A and JV candidate screening: Acquisition scorecards and integration checklists to identify targets whose synergies with incumbent platforms generate fastest payback in a post-2026 trade landscape.

The float glass market is characterized by a mix of large integrated incumbents with global footprints and agile regional players that exploit local advantages. Leading manufacturers combine scale with technology differentiation: low-carbon production lines, coated and solar-capable products, and vertically integrated supply chains. In practice, this means competitive dynamics will revolve around three vectors in 2026:

Capacity play and footprint realignment: Major groups continue to expand selectively in high-growth or strategically important markets. Recent starts and planned lines indicate incumbents are prioritizing proximity to rapidly urbanizing demand centers while hedging tariff exposure through localized capacity.

Decarbonization as competitiveness: Firms that have invested in green hydrogen, energy recovery, or lower-carbon furnaces are able to tender for projects with ESG-linked premiums and secure longer-term offtake agreements. This is increasingly a differentiator in new construction and public-sector procurement.

Product upgrading and backward integration: The move towards coated, solar, and safety-glass variants creates margin pools that smaller commodity-focused producers may struggle to access without partnerships or targeted CAPEX.

Notable developments through 2025–early 2026 underscore these trends: large firms have initiated capacity expansions in strategic geographies; some regional players have commissioned new facilities to enter solar-glass segments; and trade investigations concluded in early 2026 have reweighted the economics of cross-border supply chains. For commercial leaders, the implication is clear — 2026 is a year to accelerate structural readjustments rather than to postpone them.

Raw-material and energy cost volatility: Q1 2026 movements in soda ash and silica sand prices in Europe, combined with regional energy tariff adjustments, already impacted margins across several producers. Our scenario work shows how a sustained shift in feedstock pricing alters the attractiveness of different manufacturing hubs.

Policy and trade interventions: The conclusion of high-profile trade investigations in early 2026 has reintroduced policy risk into procurement decisions, prompting buyers to demand clearer source declarations and longer-term security of supply assurances.

Capital allocation and technology risk: With a limited number of attractive brownfield sites available, firms face trade-offs between rapid market entry (brownfield expansion) and longer-term cost competitiveness (green technology adoption). The report’s CAPEX-prioritization model helps quantify these trade-offs.

Stress-test capital plans against three scenarios: base-case demand recovery, a higher-energy-price scenario, and an accelerated ESG premium scenario. Use these to set go/no-go thresholds for new lines and retrofits.

Lock down feedstock and energy supply arrangements: pursue multi-year off-take agreements for soda ash and silica where possible, investigate green-hydrogen partnerships for longer-term decarbonization and pricing stability.

Prioritize product upgrades with fastest payback: target coated and solar-capable lines in markets where demand trajectories and pricing premia align to deliver sub-4-year paybacks under conservative assumptions.

Build tariff-resilient supply chains: evaluate nearshoring, tolling, or JV manufacturing models to mitigate short-term trade shocks revealed by 2025–2026 regulatory activity.

Use M&A selectively to fill capability gaps: prioritize targets that provide immediate access to premium product lines, local market channels, or decarbonization know-how rather than purely capacity increases.

2026 will be a year in which decisions compound: capacity additions, trade rulings, and energy-price moves will lock in competitive positions for the better part of a decade. The float glass market’s headline expansion — an expected climb from a mid-2025 baseline to a materially larger market by 2032 at roughly a 5.8% CAGR — creates opportunity, but the path to sustainable returns requires alignment across site selection, product mix, and decarbonization strategy.

This preview highlights the kinds of insight PW Consulting delivers in full. To preserve the decision advantage of our clients, core segment tables, granular regional and application-level splits, and unit-level facility economics are presented in the full report and supporting data annexes. For executives preparing 2026 capital and commercial plans, the full study offers the quantified scenarios, plant-level benchmarks, and tactical playbooks needed to convert market growth into shareholder value.

Contact PW Consulting to receive the complete Float Glass Market study, including the detailed data annex, scenario models, and a tailored executive briefing focused on your portfolio.

For detailed analysis of this topic, please visit the official page:Float Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com