Business Valuation Services in India | Accurate Company Valuation Solutions

Other |

2026-05-27 09:54:52

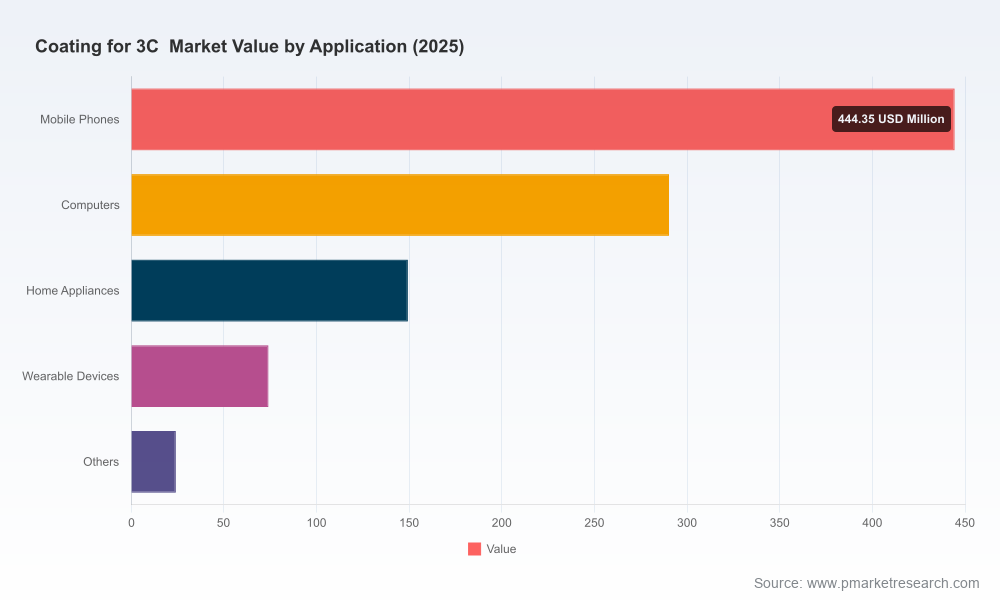

As consumer electronics, communications and computing (the “3C” segment) continue to demand thinner, more durable, and more sustainable surface finishes, coating manufacturers and downstream OEMs face a narrow window in 2026 to reset product, sourcing and M&A strategies. Our new PW Consulting study, anchored on 2025 as the base year and projecting through 2032, synthesizes macro trajectories, supply-chain stressors, regulatory inflection points and supplier strategy so corporate leaders can make high-confidence decisions this year. The market has expanded meaningfully since 2020 and — growing at a steady mid-single-digit rate (CAGR 4.6% over the forecast period) — will require targeted investments to capture premium value pools. This article previews the strategic value of the full report while preserving the proprietary segment-level detail that unlocks transaction- and plant-level decisions.

Coating for 3C Market

Timing: 2026 is the year when regulatory requirements, raw-material cycles and product innovation align. Companies that act now will avoid cost shocks and capture adoption of next-generation chemistries.

Coating for 3C Market

Clarity: The overall 3C coatings market rose from roughly USD 780 million in 2020 to approximately USD 982 million by 2025, and is on a path toward the mid-2030s range under our base-case assumptions. That trajectory supports continued investment — but only where margin pools are expanding.

Coating for 3C Market

Consolidation risk: Market concentration shows the top three vendors control just over half the market, and the top five account for roughly three-fifths. These dynamics create both partnership opportunities and competitive threats for mid-sized manufacturers and materials suppliers.

Actionability: Our report turns market forecasts into executable plans — not only “what” will happen but “how” to operationalize strategies in procurement, R&D and commercial execution.

Proprietary market sizing and outlook: a validated historical series (2020–2025) and scenario-based forecasts (2026–2032) with sensitivity runs tied to raw material and regulatory variables.

Decision-ready playbooks: step-by-step templates for licensing, co-development, and contract manufacturing, including negotiation levers and typical capex payback profiles.

Supply-chain and input-cost models: material-flow maps for key chemistries, supplier risk scores, and inventory optimization heuristics calibrated to typical 3C production cadences.

Regulatory impact toolkit: mapping of EPA/EU low-VOC and eco-label requirements to formulation choices, certification timelines, and estimated compliance costs.

Technology and product roadmaps: evaluation of UV-curing, polyurethane, in-mold and other coating technologies against durability, cycle time, sustainability and unit-cost criteria.

Commercial strategy modules: pricing frameworks, channel and OEM segmentation approaches, and go-to-market options for premium vs. cost-optimized coatings.

M&A and partnership due diligence templates: playbooks to assess target synergies, integration risks and how concentration metrics (top-3/top-5 dynamics) influence deal valuation.

Interactive appendices: supplier scorecards, sample RFP language, and anonymized case studies that illustrate successful transitions to waterborne and eco-certified product lines.

We examine incumbent global producers and regional challengers through the lens of capability, route-to-market and strategic intent. Representative players covered include well-established multinational suppliers and high-focus regional specialists. Profiles emphasize technological strengths (e.g., low-solvent or water-borne systems, Resicoat-style IP, UV-curing platforms), vertical reach into consumer electronics assemblies, and recent initiatives that shape competitive positioning.

Technology-oriented multinationals with broad application portfolios maintain advantage through scale, long-term OEM contracts and deep formulation libraries. Their investments in low-solvent/water-borne systems and surface-treatment platforms provide a structural moat against fast followers, but expose them to margin compression as customers demand greener and cheaper solutions.

Specialist regional players are closing capability gaps rapidly through co-development and partnerships for advanced inks and printing technologies — a dynamic accelerated by cross-border partnerships announced in 2025–2026 that connect inkjet OEMs with coating formulators.

Notable recent moves: several suppliers launched visible product innovations (for example, self-healing in-mold coatings and sustainability reports that signal portfolio reversals). These actions influence procurement conversations and can shorten OEM adoption cycles if backed by validated cycle-time and durability data.

Strategic takeaway: the market is bifurcating between suppliers who can credibly deliver eco-compliant, differentiated finishes and those who compete on price and logistics. For buyers, supplier selection must balance long-term technology roadmaps with near-term availability and certification status.

Regulatory pressure is real and immediate. Environmental regulation enforcement in major markets has shifted formulary economics toward low-VOC, water-based systems — an observable market movement where water-based coatings have widened their share materially against solvent-based alternatives. ISO 14001 and eco-label certifications have migrated from optional differentiators to near-required credentials for premium supply contracts.

Raw-material volatility: powder resin availability has experienced disruption, constraining some powder-based coating capacities and forcing manufacturers to evaluate alternative chemistries or dual-sourcing strategies.

Labor-cost inflation in Asian manufacturing hubs increases the total landed cost of certain coatings and favors higher-automation, lower-labor-intensity application processes (e.g., UV-curing and digital printing) that reduce cycle time and error.

Technology convergence: developments in inkjet printing, self-healing topcoats, and advanced UV formulations are shifting value from basic coatings to system-level solutions (materials + application technology + service).

Below are prioritized, executable recommendations for executives setting 2026 plans. Each recommendation is accompanied by the typical lead time and expected impact on margin, risk and time-to-value.

Secure critical inputs immediately (0–6 months). Negotiate multi-year supply agreements for constrained inputs (e.g., specialty resins) and create contingency inventory buffers. This mitigates stop/start production risk and gives negotiating leverage.

Fast-track eco-certification (3–12 months). Align formulations and quality systems to ISO 14001 and relevant eco-labels. For OEM suppliers, certification is now a gating factor in many procurement processes.

Invest selectively in application automation (6–18 months). Prioritize UV-curing and digital-print integration where labor-cost or throughput constraints are significant; pilot projects will justify capital investments within typical payback windows for high-volume 3C components.

Prioritize R&D for differentiated chemistries (12–36 months). Focus on waterborne, low-VOC systems with tailored functional properties (scratch resistance, sensor-friendly coatings, anti-fingerprint) and position products as system solutions rather than raw materials.

Pursue targeted acquisitions and partnerships (6–24 months). Use concentration metrics to identify strategic targets that either shore up supply, add differentiated IP, or grant access to priority OEM relationships. Our valuation templates quantify synergies and integration risks by scenario.

Redesign commercial terms to protect margin. Shift toward value-based pricing for differentiated coatings and service bundles (e.g., formulation licensing, application training, warranty-backed coatings) to avoid pure volume price competition.

Regulatory: escalating VOC limits can render legacy formulations non-compliant. Mitigation: fast-track reformulation and secure transitional waivers where available.

Supply: resin shortages and single-source dependencies. Mitigation: dual-source strategies and geographic diversification.

Commercial: OEM consolidation and extended payment terms compress cash cycles. Mitigation: structured financing, long-term contracts with price-adjustment clauses tied to input indexes.

We designed the full Coatings for 3C Market study to function as an executable toolset rather than a static document. Subscribers receive models and templates they can run with their own inputs, supplier scorecards calibrated to regional manufacturing centers, and a confidential annex of supplier capabilities and recent M&A activity. The report’s interactive scenarios allow leadership teams to test options — for example, the impact of accelerated eco-certification or a 12–18 month resin shortage — and quantify the P&L and balance-sheet implications before committing capital.

2026 will be a defining year for participants across the 3C coatings value chain. The market is mature yet dynamic — expanding from a strong 2025 base and growing at approximately 4.6% CAGR under our baseline forecast — which means there are pockets of attractive growth if companies reposition around sustainability, supply resilience and system-level offerings. PW Consulting’s full report provides the confidential segmentation, supplier-level intelligence and financial models required to make those moves with conviction. For leadership teams deciding where to deploy capital, how to source critical inputs, or which technologies to prioritize, our study converts uncertainty into a prioritized, implementable roadmap.

To access the complete report, proprietary appendices and interactive scenario tools, please visit our report landing page or contact your PW Consulting lead. The preview above demonstrates the depth of our analysis while reserving the detailed tables and supplier-level data that form the basis for transaction and plant-level decisions in 2026.

For detailed analysis of this topic, please visit the official page:Coating for 3C Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com