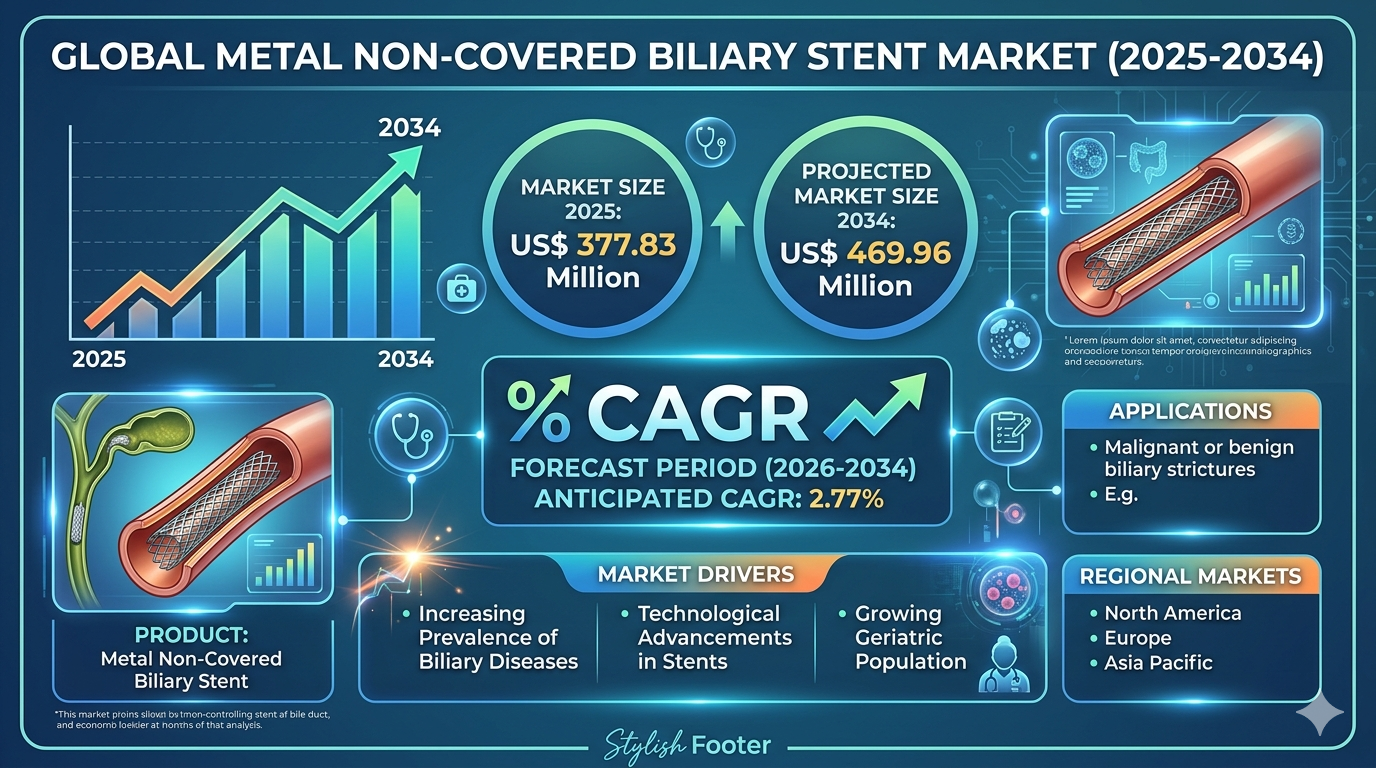

Clinical Demand Trends Driving the Global Metal Non‑Covered Biliary Stent Market

Health |

2026-05-06 12:56:28

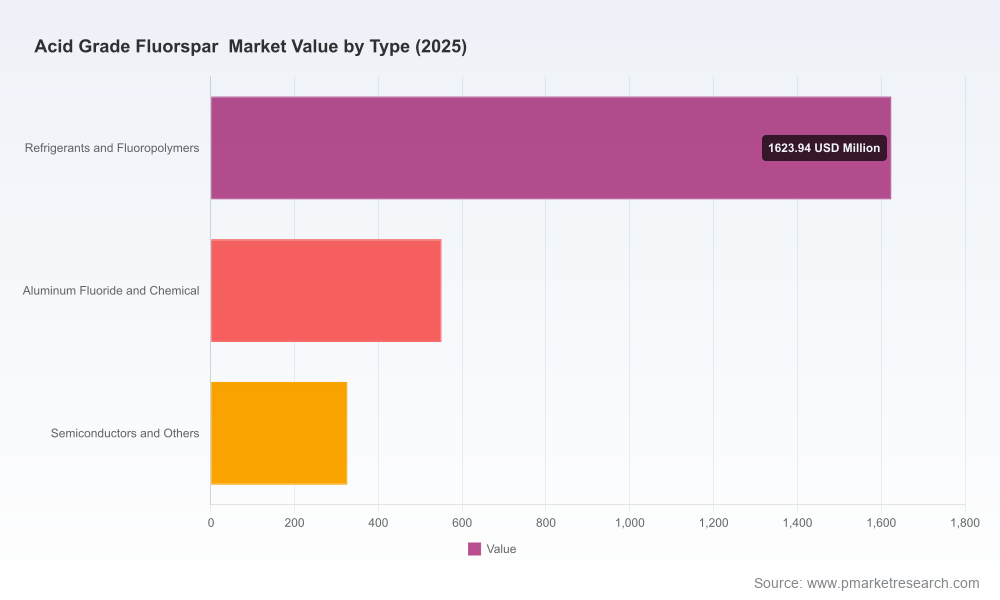

As companies prepare strategy for 2026 and beyond, acid‑grade fluorspar (acidspar) has moved from a background commodity to a strategic raw material that demands active portfolio management. PW Consulting’s latest market study — based on a 2025 base year and a 2026–2032 forecast window — models a steady recovery and structural re‑rating of the acidspar market. The global market is projected to grow from an estimated USD 2,500.12 Million in 2025 to approximately USD 3,289.99 Million by 2032, reflecting a compound annual growth rate (CAGR) of 4.0% through the forecast period. Historical context (2020–2025) shows a resilient rebound from pandemic and regulatory disruptions, and our scenarios highlight how policy, downstream price dynamics and new supply entrants will shape commercial outcomes.

Acid Grade Fluorspar Market

Supply composition is changing: 2024–2025 policy and safety enforcement actions in major producing countries, combined with new domestic projects in North America and restarts in other regions, have materially altered short‑term availability and trade flows. Buyers and processors should assume a more segmented and policy‑sensitive supply base going into 2026.

Acid Grade Fluorspar Market

Defense and strategic procurement are elevating demand profile: Recent contract awards signal that authorities are treating acidspar as a critical mineral for specific industrial and national security applications, creating pockets of non‑market demand that will influence spot and long‑term pricing dynamics.

Acid Grade Fluorspar Market

Downstream price pressure and substitution risk: Anhydrous hydrofluoric acid (AHF), whose feedstock is fluorspar, shows price volatility that transmits upstream — our sector tracking recorded an average AHF price in the United States at USD 2,565/MT in Q1 2026 — reinforcing the need for integrated commercial risk management across mining, beneficiation and chemical processing.

Regulatory acceleration: European critical‑raw‑materials policies and tariff treatments in key markets are creating incentives for local sourcing, domestic processing investment and supply‑chain reshoring. These factors are reshaping incentives for both greenfield projects and brownfield upgrades in 2026.

This study is engineered for executives, commercial teams, and corporate development groups who need actionable intelligence, not just descriptive analysis. Key deliverables include:

The competitive map for acidspar is evolving rapidly. A mix of incumbent producers, regional champions and new entrants is reshaping counterparty risk and bargaining power. PW Consulting’s qualitative supplier assessment identifies several strategic archetypes:

Domestic strategic supplier — Ares Strategic Mining Inc. (Delta, Utah) has moved from developer to a contracted strategic supplier, accelerating construction and winning a significant Department of Defense indefinite delivery/indefinite quantity (IDIQ) contract in January 2026 (initial award USD 168.9 million with uplift potential). For buyers targeting sovereign assurance of supply, such producers represent a premium but non‑fungible source of product and an important alternative to traditional trade flows.

Regional restart and scale ramp — Canada Fluorspar Inc. (St. Lawrence) executed first commercial shipments in 2025 and is in ramp‑up toward large annualized volumes. Projects that achieve first‑shipment proof points in 2025–2026 materially reduce execution premium for offtakers and create optionality for regional supply contracts.

Integrated and specialty producers — Producers with vertically integrated upstream and fluorochemical assets provide downstream offtake synergy, tighter quality control and price pass‑through mechanisms. Several Asian and European integrated groups remain pivotal to global fluorochemical supply chains and can act as both supplier and strategic partner for market participants pursuing vertical integration.

High‑capacity regional operators — Established mines with demonstrated processing capacity remain essential to balancing markets, although their incentive to export versus satisfy domestic conversion needs depends on local policy and margin differentials.

For commercial managers and BD teams, the immediate implication is straightforward: prioritize a small set of strategic relationships that balance sovereign risk, price exposure and logistics complexity. Our supplier matrices in the report map these trade‑offs at transaction scale.

Diversify exposure through layered contracting. Combine long‑form offtake agreements for strategic volume with flexible spot purchase corridors to capture upside when downstream margins improve. Include quality and assay clauses that reflect processing tolerances.

Explicitly model policy shocks. Run scenario tests that assume further production curtailments in one or two large producing jurisdictions, and specify trigger‑based procurement clauses linked to declared force majeure and strategic stockpile releases.

Link procurement to processing commitments. Where possible, negotiate co‑investment or tolling arrangements with processors to capture downstream margin and manage feedstock quality risk.

Use price signals to time capex. Our forecast shows steady expansion through 2032 against a 4.0% CAGR from 2026; use these modeled price trajectories to time beneficiation upgrades, brownfield debottlenecking and targeted exploration.

Engage with regulators and standards bodies early. The landscape of trade classifications and critical‑minerals policy—including tariff treatments and EU‑level incentives—means permitting timelines can be compressed or extended by active stakeholder engagement.

The report’s core market model provides the following ready‑to‑use outputs for corporate planning cycles in 2026:

For executive teams preparing 2026 plans, our recommendation is to convert insight into action across three parallel tracks:

Acid‑grade fluorspar is no longer a passive line item: it is an operational choke point for fluorochemicals, a component of strategic inventories for certain jurisdictions, and a priced input whose volatility can compress downstream margins quickly. PW Consulting’s Acid‑Grade Fluorspar Market study provides the integrated market and commercial intelligence required to turn this raw material from a risk into a managed element of competitive advantage. We reveal the demand and supply dynamics underpinning our 4.0% forecast CAGR and provide transaction‑ready tools; the full dataset and granular segmentation are available in the complete report for firms ready to build or defend 2026 strategies.

To review the underlying datasets, scenario outputs, supplier scorecards and contract playbooks that power these conclusions, visit PW Consulting’s full report page. The detailed segmentation, country‑level flows and downloadable models are provided there to inform procurement, commercial and capital allocation decisions in 2026.

For detailed analysis of this topic, please visit the official page:Acid Grade Fluorspar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com