How to Choose the Perfect Mangalsutra for Women

Shopping |

2026-06-02 05:45:15

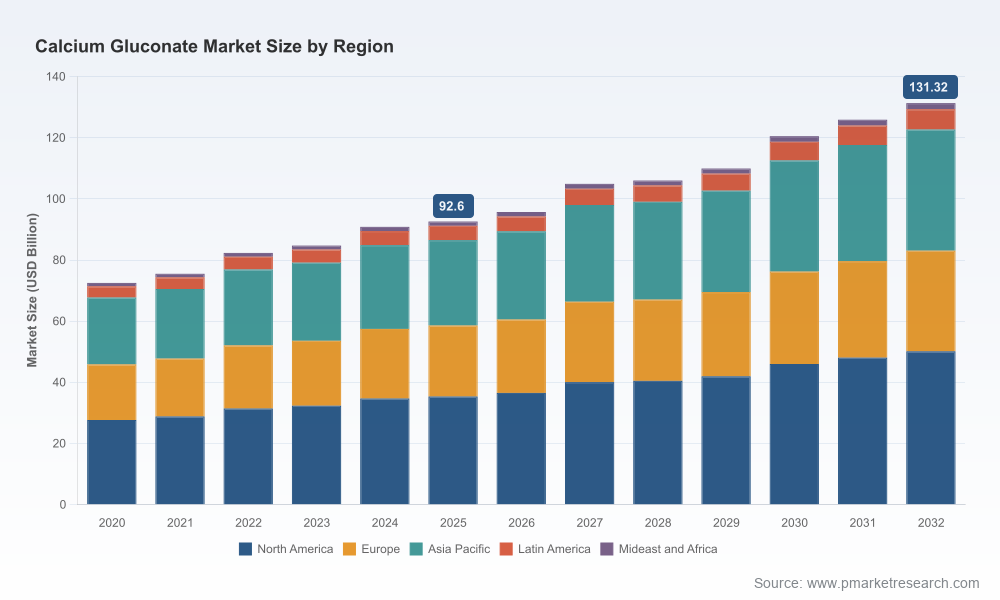

As pharmaceutical supply chains and specialty-chemical markets normalize after several years of volatility, calcium gluconate stands out as a commodity with both defensive demand and episodic supply risk. PW Consulting’s new market study (base year 2025) synthesizes historical performance (2020–2025) and forward-looking scenarios (2026–2032) to give commercial and operational leaders a practical playbook for 2026 decision-making. The market expanded from approximately USD 72.5 Billion in 2020 to USD 92.6 Billion in 2025 and is projected to grow to roughly USD 95.7 Billion in 2026, continuing to USD 131.32 Billion by 2032 at a 5.02% CAGR. These macrodrivers frame near‑term procurement choices, regulatory investment priorities, and M&A targeting through the rest of the decade.

Calcium Gluconate Market

Purchasers and manufacturers face a market that is large, growing steadily, and structurally segmented between API suppliers and finished-dose producers. That combination creates opportunities for margin capture through vertical integration, contract reconfiguration, and portfolio optimization.

Calcium Gluconate Market

Regulatory and raw-material shocks remain the primary short‑to‑mid term risk vectors. Firms that align sourcing strategy to mitigate glucose-feedstock volatility and tariff exposure will preserve continuity and price competitiveness.

Calcium Gluconate Market

Market concentration metrics indicate meaningful scale advantages among the leading firms but enough fragmentation to reward focused consolidation, especially in specialty finished-dose and regulated injectable segments.

From 2020 to 2025 the market recorded robust expansion driven by steadily rising pharmaceutical and supplement demand. The 2026 outlook projects continued growth to about USD 95.7 Billion, with an intermediate-term trajectory that reaches approximately USD 131.32 Billion by 2032 under the base case—implying a compound annual growth rate of about 5.02% across the forecast window. These aggregate figures reflect combined activity across API manufacture, food/ingredient applications, industrial uses, and finished-dose products.

Upstream feedstock economics: Gluconic acid—produced primarily via microbial fermentation—remains the dominant upstream feedstock. Glucose inputs account for a substantial portion of production cost. Volatility in glucose availability or price feeds directly into margin compression for producers, and into pricing swings for buyers.

Trade and tariff headwinds: Recent tariff measures affecting glucose‑related products from major exporters have altered trade flows and increased landed cost for some manufacturers. These changes reconfigure short-term supplier selection and contractual terms for 2026‑era procurement.

Geopolitical logistics risk: Broader geopolitical disruptions—exemplified by regional conflicts—have intermittently constrained supply of certain chemical inputs and freight capacity. These events amplify the value of contingency inventory, multi‑source agreements, and near‑shore capabilities.

Regulatory and quality thresholds: For pharmaceutical applications, dossier coverage (e.g., DMF/CEP/other filings) is a gating factor for market access. Firms that maintain up‑to‑date regulatory filings and quality certifications secure premium access to regulated buyers and can command supply-preference in crisis windows.

Leaders should treat 2026 as a window for defensive reinforcement and selective expansion. Recommended strategic moves include:

Supply‑chain redesign: Prioritize dual-sourcing and develop alternative feedstock pathways. Where prices or tariff exposure are material, pursue backward integration into gluconic acid or structured off‑take agreements with glucose suppliers to stabilize cost of goods sold.

Regulatory harmonization: Accelerate cross‑jurisdictional dossier updates for key products. For API suppliers, maintaining a portfolio of current regulatory filings is not discretionary—it's a market access lever that preserves revenue and reduces time-to-market for customers.

Manufacturing footprint optimization: Evaluate near‑shoring or regional contract manufacturing partnerships for finished-dose injectables. The premium for localized, ready‑to‑administer sterile formats increases in times of acute hospital demand and procurement preference.

Commercial contracting: Move from short-term spot buying to blended contracting models—mixing firm volume commitments with indexed spot tranches—to share risk with suppliers while retaining upside optionality if prices soften.

M&A and JV playbook: Given the market’s moderate concentration, 2026 is well-timed for targeted acquisitions—particularly of mid‑sized API producers with regulatory assets or of sterile contract manufacturers with hospital-channel relationships. Focus on assets that close strategic gaps rather than generalist scale alone.

Scenario planning & stress tests: Run at least three supply‑chain stress scenarios (base, tariff‑shock, and feedstock‑scarcity) and bake outcomes into 18‑ to 36‑month inventory and capex plans. Adopt trigger points for contingency activation tied to concrete price or lead-time thresholds.

The competitive map splits into two broad clusters: API and raw-material specialists, and finished-dose/critical-care suppliers. Leading API producers and chemical manufacturers have invested in regulatory dossiers and export capabilities, while the established hospital- and critical-care manufacturers focus on sterile formulations and service continuity. Market concentration figures show that the top three firms command a notable share of market volume, with the top five holding a larger but non‑dominant portion—leaving room for nimble challengers to differentiate on quality, lead time and regulatory coverage.

API and commodity suppliers: Several firms headquartered in major manufacturing hubs offer Calcium Gluconate for pharmaceutical and supplement uses. These companies typically compete on regulatory completeness (filings such as USDMF, CEP/other regional filings), consistent quality, and export reach.

Finished‑dose and critical‑care suppliers: Major hospital-supply players differentiate on sterile filling capacity, emergency preparedness (e.g., compounding/503B readiness), and established procurement relationships with health systems.

Competitive advantage levers: The most consequential differentiators are (1) breadth of regulatory dossiers across jurisdictions, (2) secure and low-cost feedstock access, (3) sterile manufacturing and supply continuity, and (4) agility to re-route logistics during geopolitical disruptions.

Our full study is structured as an actionable decision-support suite for executive teams, procurement leads, and investors. Key deliverables include:

Proprietary demand model calibrated from 2020–2025 and projected through 2032 with scenario overlays and sensitivity analyses.

Forward-looking pricing curves, input‑cost pass‑through models, and margin impact matrices under alternative feedstock and tariff assumptions.

Regulatory heatmaps and dossier‑gap audits by jurisdiction to prioritize filing investments and supplier selection.

Supplier mapping and capability scoring—covering regulatory coverage, quality systems, geographic location, and logistic resilience—designed to accelerate shortlist formation in sourcing events.

M&A screening playbook with valuation heuristics for target selection, integration risk checklists, and post‑deal value capture levers (procurement synergies, cross‑selling, capacity rationalization).

Operational playbooks for contingency inventory sizing, contract structures (fixed, indexed, hybrid), and capex decision templates for sterile fill/finish investments.

Procurement teams: Implement a three‑tier supplier strategy immediately—primary, secondary, and emergency—with contract terms that include price indexation and force‑majeure clauses aligned to trade disruption risk.

R&D and regulatory: Prioritize filing updates for any product lines where dossier gaps exist in strategic markets; moving filings up the queue will materially shorten time‑to‑supply windows.

Corporate development: Authorize a focused diligence pipeline for two types of targets—(a) regional API leaders with regulatory assets; (b) sterile fill/finish facilities servicing hospitals—as these bring the fastest route to durable revenue enhancements.

Finance: Stress test working capital models against glucose price shocks and tariff scenarios; consider options like supplier finance and inventory financing to smooth earnings volatility.

The high‑level figures, dynamics and strategic guidance above are a curated extract of PW Consulting’s comprehensive market intelligence. Our full report contains the granular, transaction‑grade datasets, supplier scorecards, and scenario models that operational teams will use to build contracts, capital plans, and M&A cases in 2026. Access to those line‑level forecasts, regional and application splits, and supplier performance matrices is available through PW Consulting’s report distribution—these datasets are intentionally withheld here to preserve the research’s actionability for clients and decision-makers.

For procurement, regulatory, and corporate development leads preparing their 2026 roadmaps, we recommend commissioning a bespoke briefing and scenario run using your internal sourcing and product portfolios. PW Consulting can provide tailored stress tests, supplier diligence, and an implementation roadmap aligned to the timing and budget of your strategic plan. Contact our Calcium Gluconate market advisory team to schedule a briefing and obtain the full dataset and playbooks.

For detailed analysis of this topic, please visit the official page:Calcium Gluconate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com