Electronic Lab Notebook Market Trends: Cross-Platform Integration

Other |

2026-04-08 07:19:31

As utilities, meter manufacturers, and system integrators plan capital allocation and product roadmaps for 2026, the AC current transformer (CT) segment that feeds electrical meters presents both steady baseline demand and selective pockets of technical disruption. PW Consulting’s forthcoming market research synthesizes seven years of historic performance (2020–2025) with a seven-year forecast (2026–2032) to equip business leaders with the context they need to prioritize investments, manage supply chains, and shape go-to-market strategies. This preview outlines the strategic value of that research without disclosing the proprietary segment-level datapoints reserved for subscribers.

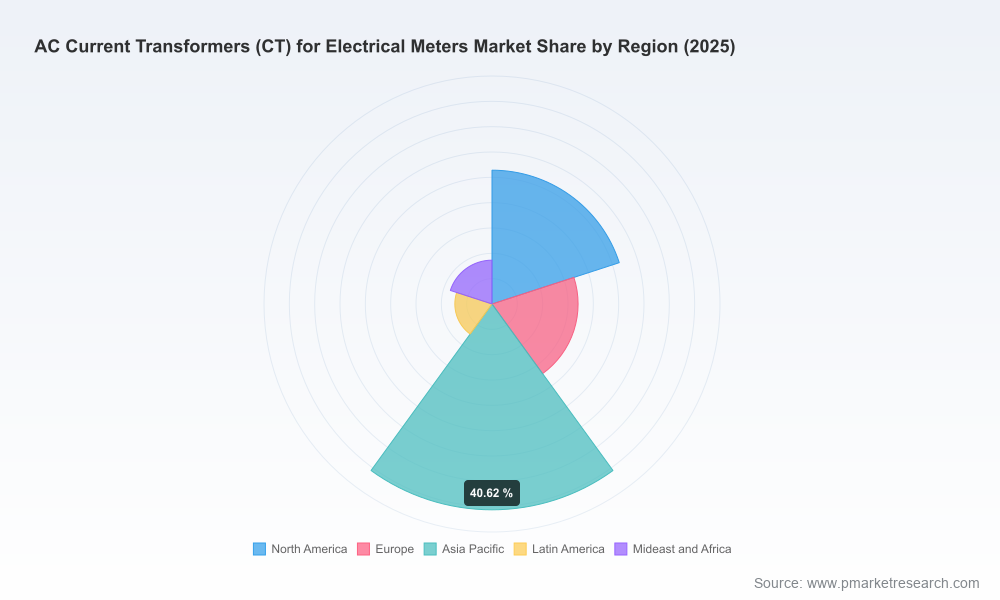

AC Current Transformers (CT) for Electrical Meters Market

Timing matters. With the market at an inflection point—household and commercial meter replacement cycles accelerating in some regions while infrastructure modernization continues elsewhere—companies that move in 2026 can lock-in design wins and supply relationships that compound over the forecast period.

AC Current Transformers (CT) for Electrical Meters Market

Regulatory updates are altering technical specs. ANSI’s 2026 refresh of meter performance criteria and several national amendments to smart-meter rollout policy are changing what qualifies as compliant, revenue-grade metering. Procurement and R&D plans that ignore these changes risk rework or certification delays.

AC Current Transformers (CT) for Electrical Meters Market

Technology differentiation matters more than ever. Materials (e.g., nanocrystalline cores), form factors (split-core, solid-core, Rogowski coils), and the ability to manage RF immunity and low-current accuracy are decisive in securing design-in for smart meters and retrofit markets.

Market sizing and trajectory are material but not dramatic—growth is predictable. Our base-year (2025) market analysis and the forecast to 2032 show consistent expansion at a mid-single-digit CAGR, reflecting steady but selective demand drivers: meter upgrades, grid modernization programs, and targeted electrification projects.

Using 2025 as the base year, PW Consulting quantifies a resilient market that has expanded through the last half-decade and is forecast to grow at approximately a 4.5% compound annual rate through 2032. That trajectory reflects a balance of tailwinds—smart meter rollouts, increasing metering accuracy requirements, and regional grid investments—and headwinds, such as component commoditization, supply-chain volatility, and competitive pricing pressure. For 2026 strategy, the implication is clear: the market will reward firms that combine technical differentiation with disciplined cost-to-serve.

Standards and compliance: ANSI C12.1-2026 revises accuracy and immunity testing that directly affect CT specifications for revenue meters. Complementary guidance from facility and national standards, including recent amendments aimed at accelerating smart meter deployment, mean that compliance cycles will dominate product roadmaps and procurement timelines in 2026.

Technical stability in real deployments: Field guidance published in 2026 by leading CT suppliers highlights real-world metering failure modes—temperature drift, RF susceptibility, and mechanical stress at installation—that influence selection criteria for meter manufacturers and installers.

Product form factor convergence: Split-core solutions remain attractive for retrofit work, while nano-material core technologies are preferred where high accuracy at low currents and minimal saturation are required. New multi-function meter introductions increasingly integrate vendor-supplied CTs, changing buyer-supplier relationships.

Fragmented supply base: The segment remains fragmented—several specialized suppliers supply high-precision cores and assembled CTs, while many regional players compete on cost and availability. That fragmentation creates both pricing pressure and ample acquisition targets for consolidation-minded suppliers.

The competitive field combines global technology leaders, regional specialists, and component-focused manufacturers. PW Consulting’s company-level analysis synthesizes product capability, materials technology, geographic footprint, and recent corporate activity to reveal where partners, acquisition targets, or competitive threats may emerge.

Vacuumschmelze (Hanau, Germany) — Strength: materials leadership. Known for nanocrystalline cores (VITROPERM/VITROVAC) that deliver superior accuracy and low-loss performance for 50/60 Hz meters. Strategic fit for OEMs that need high-end, compact CTs for revenue-grade and smart-meter applications under international standards.

Accuenergy (United States) — Strength: customization and accuracy. Offers the AcuCT series across split-core and solid-core formats with a focus on revenue-grade measurement and power-monitoring use cases. A strong partner for firms that require rapid prototyping and tailored accuracy classes.

LEM (Switzerland) — Strength: trusted industrial brand. With AT Series split-core CTs, LEM targets smart-grid and automation applications where repeatability and long-term stability matter. Their industrial pedigree makes them a reliable partner for grid and utility OEMs.

Phoenix Contact (Germany) — Strength: systems integration. PACT series CTs are designed for both new installs and retrofits, emphasizing ease of integration into broader energy-monitoring architectures—a strategic advantage for channel partners and integrators.

Electro-Meters (United States) — Strength: low-voltage metering heritage. Their series-level CTs are optimized for meter manufacturers seeking proven, cost-controlled components suitable for mass deployments in residential and commercial segments.

Flex-Core (United States) — Strength: breadth of inventory. Offers a wide range including clamp-on and Rogowski solutions—valuable to service organizations and test labs that need flexible, field-deployable sensing options.

Oswell E-Group (China) — Strength: miniature and application-focused designs. Recent technical guidance released in 2026 demonstrates intent to influence meter OEM design practices and accelerate component-level readiness for mass production.

GFUVE Group (China) — Strength: integrated product launches and deployments. Early-2026 product introductions and field installations underscore their capability to move from R&D to on-site commissioning—relevant for utility pilots in APAC and Southeast Asia.

YTL Meter (China) — Strength: vertical integration with metering product lines. Provides split-core CTs as components for its smart-meter portfolio, reducing supply chain complexity for buyers seeking integrated solutions.

Oswell E-Group published practical guidance in May–June 2026 focused on stabilizing CT performance and identifying production bottlenecks for smart meters—content that signalizes a push to influence OEM design decisions early in the procurement cycle.

GFUVE Group’s 2026 product launches and installations show an emphasis on bundled meter-plus-CT offers and on-the-ground commissioning expertise, a competitive posture that could speed customer adoption in target markets.

Trade show activity through late 2025 continues to be a sourcing and specification channel; meter component suppliers remain visible at regional industry events, creating read-across opportunities for partnership and product discovery.

Authoritative market sizing and forecast (2020–2032) with scenario sensitivity for high-growth and constrained outcomes.

Regulatory impact mapping: how recent and imminent standards (including ANSI C12.1-2026 and national smart-meter policies) change product specs, certification timelines, and procurement criteria.

Technology evaluation: materials, form factors, and electromagnetic performance trade-offs explained for product managers and procurement specialists.

Supply-chain and cost-to-serve matrix: identifying single points of failure, regional supplier capabilities, and lead-time scenarios critical to 2026 sourcing decisions.

Go-to-market playbooks for the five most commercially relevant buyer archetypes—meter OEMs, utilities, systems integrators, industrial end-users, and retrofit installers.

Vendor benchmarking and M&A heatmap: profiles of the key players, capability gaps, and M&A scenarios that can generate scale or technical differentiation.

Practical annexes: test-methodology primer, accuracy-class selection guide, and a supplier short-listing tool for RFP design.

For OEMs: Prioritize designs that simplify third-party CT validation under updated standards and build dual-sourcing strategies for critical core materials to manage lead-time risk.

For utilities and integrators: Include RF immunity and low-current accuracy requirements in procurement contracts and demand factory-level compliance evidence to avoid costly field rework.

For component suppliers: Invest selectively in materials and metrology capabilities that address field failure modes called out in recent technical guidance—these are differentiators OEMs will pay for.

For private equity and corporate development teams: The fragmented landscape coupled with predictable market growth supports roll-up strategies concentrated on value-adding technologies and regional distribution capability.

The complete study is designed as a decision-support toolkit: use the regulatory mapping to update compliance calendars; use the vendor benchmarking to inform supplier selection or acquisition screening; and apply the pricing and cost-to-serve analysis to refine margin models and to structure service-level agreements. Importantly, the report’s scenario work allows procurement and product teams to stress-test 2026 capital plans against slower and faster adoption curves.

PW Consulting’s forthcoming AC Current Transformers (CT) for Electrical Meters Market report delivers the data, context, and execution guidance that executives need to make confident, time-sensitive decisions in 2026. This preview outlines the macro picture, competitive dynamics, and the regulatory environment; the full report contains the granular segmentation and proprietary datasets that underpin supplier shortlists, RFP templates, and M&A screening tools. For teams that must convert 2026 intentions into measurable outcomes—design wins, procurement contracts, or accretive acquisitions—the full intelligence package closes the gap between strategy and execution.

To access the complete dataset, supplier scorecards, and implementation playbooks referenced in this preview, consult PW Consulting’s full report and advisory services for tailored briefings and scenario modeling.

For detailed analysis of this topic, please visit the official page:AC Current Transformers (CT) for Electrical Meters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com