Chrome Metal Powder Market — Strategic Briefing for 2026 Decision-Makers

Executive snapshot

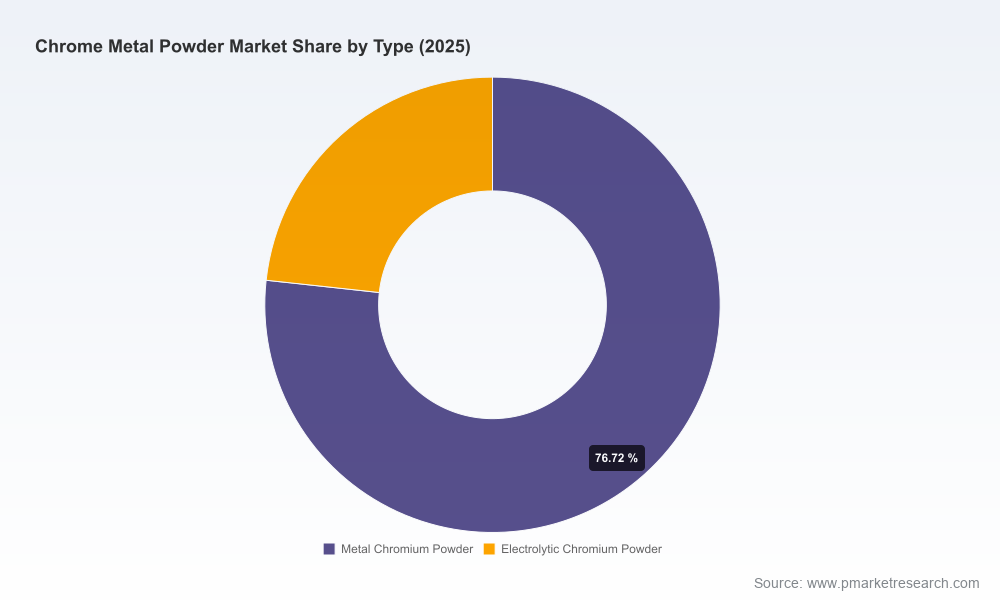

As the chrome metal powder market enters a decisive phase, PW Consulting’s latest study (base year 2025; historical window 2020–2025; forecast 2026–2032) synthesizes macro trajectories, operating dynamics, and competitive playbooks that will determine winners and losers through the remainder of this decade. The market expanded from approximately USD 125 million in 2020 to roughly USD 189 million in 2025, and is projected to reach about USD 325 million by 2032 — an implied compound annual growth rate of 8.1% across the forecast. This profile signals a market that is neither niche stagnation nor hyper-scale; it is a structurally growing industrial material market driven by selective end-market adoption, raw material cycles, and regulatory inflection points.

Chrome Metal Powder Market

Why this report matters for 2026 strategic planning

Corporate leaders planning 2026 investments face three concurrent pressures: capture growing demand in advanced manufacturing segments, protect margin against raw-material and compliance cost inflation, and de-risk supply chains in a moderately concentrated supplier landscape. Our research translates those pressures into actionable options — not just descriptive metrics. For executives evaluating capacity investments, JV partners, or M&A targets, the study provides the risk-weighted signals and scenario-conditioned thresholds you need to commit capital with conviction.

Chrome Metal Powder Market

What the study delivers (operationally-focused contents)

- Market sizing and validated growth pathways — historical reconciliation and a transparent forecast architecture for 2026–2032 that links demand by broad application buckets to production economics.

- Supply-demand model with sensitivity analysis — includes short-cycle price shock and long-cycle raw-material scenarios to stress-test margins and cash-flow for manufacturers and buyers.

- Regulatory risk matrix — granular assessment of hexavalent chromium-related compliance across advanced jurisdictions, enforcement trajectories, and estimated CAPEX/OPEX impact bands for cleaner processing.

- Technology and cost roadmap — mapping of incumbent production routes vs. lower-emission alternatives, with unit-cost breakpoints and adoption timelines relevant to 2026 investment decisions.

- Competitive benchmarking and capability maps — capability, footprint, product-grade breadth, and strategic intent scoring for the market’s leading players (detailed profiles and valuation heuristics included in the full report).

- M&A and go-to-market playbooks — target prioritization, integration risk checklists, and revenue synergy calculators built for market consolidation and downstream integration strategies.

- Commercial playbook for buyers — supplier risk heatmaps, contract negotiation levers, and inventory policy prescriptions aligned to price volatility regimes.

- Primary interview evidence — operator-level insights from plant managers, procurement chiefs, and regulatory advisors to ground our modeling assumptions.

Market dynamics — what is really moving the needle

Three structural themes underpin the market’s 8.1% CAGR and should shape corporate choices in 2026.

Chrome Metal Powder Market

- Raw-material cycles and cost pass-through: Chromite ore fundamentals tightened in 2024 with a measurable uplift in mine production but also higher realized ore prices into late 2025. The combination of modest production growth and stronger ore pricing has shifted cost curves upward — compressing margins for processors that cannot fully pass-through costs to downstream buyers.

- Regulatory tightening accelerates capital intensity: Newer and stricter regulations focused on hexavalent chromium emissions, especially across advanced markets, are forcing producers to invest in cleaner processing technologies. The near-term consequence is elevated CAPEX and incremental OPEX for compliance; the medium-term effect is a higher structural cost of supply and a bias toward suppliers that have already de-risked emissions.

- Selective end-market demand and technology substitution: Demand growth is being driven by a handful of advanced manufacturing applications where chrome’s properties are mission-critical. At the same time, technology substitution and material-efficiency programs in some end-markets create pockets of lower demand elasticity — making product-grade differentiation and value-added services (e.g., tight particle distribution, low contamination) a decisive commercial lever.

Supply structure and competition — reading the competitive map

The market exhibits moderate concentration: the top three suppliers capture a substantial but not dominant share, and a broader set of five players increases that share further — a structure that favors nimble challengers and selective consolidation. In practice, this means:

- Regional manufacturing footprints matter: Producers with flexible multi-site production can respond to local regulatory requirements and shorten lead times into critical aerospace and electronics customers.

- Scale + technical depth wins in premium segments: Firms that combine larger-scale supply capability with advanced product grades are best positioned to serve high-value applications where quality tolerance is low and switching costs are high.

- Mid-size producers can specialize: Several mid-market manufacturers are competing effectively by focusing on cost-competitive grades for welding, pigments, and powder metallurgy, or by offering bespoke services such as pre-alloyed powders.

Company-level implications — positioning the core players

Our competitor analysis examines manufacturers ranging from diversified chemical groups to specialized powder producers. High-level takeaways include:

- Large, diversified chemical companies with non-ferrous portfolios — they bring balance-sheet strength and the ability to invest in cleaner processing. Their strategic playbooks center on securing feedstock and expanding into higher-margin value chains.

- Specialized powder producers — these companies compete on product purity, particle engineering, and customer intimacy. Their defensibility rests on technical differentiation and closer ties to OEMs in aerospace and electronics.

- Regional metal and alloy manufacturers — they often serve domestic industrial demand and can be acquisition targets for players seeking local market access or throughput expansion.

- Newer entrants and niche players — they drive process innovation and can re-shape grade economics if their lower-emission or lower-cost routes scale successfully.

Our full profiles score each company across capability dimensions (technical, regulatory readiness, feedstock security, commercial reach) and include a short list of near-term strategic moves we expect each type of player to pursue in 2026. These insights are presented to help buyers and investors identify credible partners and targets without sifting through unverified claims.

Strategic implications and recommended 2026 actions

Based on the synthesis of supply dynamics, regulatory pressure, and competitive behavior, PW Consulting recommends executives consider the following portfolio of actions for 2026:

- Prioritize feedstock contracts with flexibility: Locking in supply is necessary, but so is optionality. Structure contracts with indexed pricing collars and capacity release clauses to balance security and responsiveness to ore price swings.

- Accelerate compliance-focused CAPEX selectively: Target investments that both reduce emissions and lower long-run unit costs (e.g., recovery improvements, closed-loop processes). Prioritize upgrades that deliver a clear payback under plausible ore-price and regulatory scenarios.

- Differentiate on product-grade and service: For producers, technical differentiation (particle control, contamination limits) will create defensible niches. For buyers, supplier selection should weight technical capability and regulatory readiness as heavily as price.

- Use M&A to buy time and capability: Acquiring regional capacity with compliant operations or specialized grades can be faster and less risky than greenfield builds when near-term demand is material and capacity timelines are tight.

- Adopt a multi-horizon sourcing strategy: Combine spot, committed, and strategic partnership channels to cover immediate needs while preserving upside exposure to potential downward price corrections.

How to use this study in boardroom and operating planning

For corporate directors and operating executives, the study is structured as a decision tool rather than a reference file. Practical uses include:

- Board-level investment memos: use our scenario outputs to stress-test payback and downside risk before approving new capacity or transformational M&A.

- Procurement playbooks: adopt our supplier-risk heatmaps and contract templates to reduce exposure to short-term price shocks and regulatory surprises.

- R&D prioritization: align material and process development budgets to the grade and emission targets that unlock premium end-market demand.

- Integration planning: use our M&A checklists and synergy calculators to size realistic revenue and cost upside for any consolidation moves considered in 2026.

Conclusion — the 2026 strategic inflection

The chrome metal powder market is entering a phase where operational discipline, regulatory foresight, and targeted capability plays will determine relative performance. Our forecast to 2032, coupled with sensitivity testing, shows meaningful upside for companies that both secure feedstock at disciplined economics and invest purposefully in compliance and product differentiation. The full PW Consulting study contains the underlying models, the granular segmentation, and the supplier-level intelligence you need to translate this briefing into executable plans. For executives who must make capital and commercial decisions in 2026, the detailed report is designed as the single source to accelerate confident, risk-aware action.

Next step

Access the full report page to review the detailed segmentation tables, scorecards, and downloadable scenario models that underpin these strategic recommendations.

For detailed analysis of this topic, please visit the official page:Chrome Metal Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com