Dental Laboratory Micromotor Market 2034: Current Trends Reshaping Precision Dental Equipment

Health |

2026-05-26 12:02:37

As companies and public utilities enter 2026, sodium hypochlorite has re-emerged as a strategic intermediate: central to municipal water treatment, sanitation, household cleaning, and a range of industrial bleaching and synthesis applications. PW Consulting’s market study (base year 2025; historical window 2020–2025; forecast 2026–2032) captures this inflection with a detailed, actionable toolkit for commercial, operational and investment decisions.

Sodium Hypochlorite Market

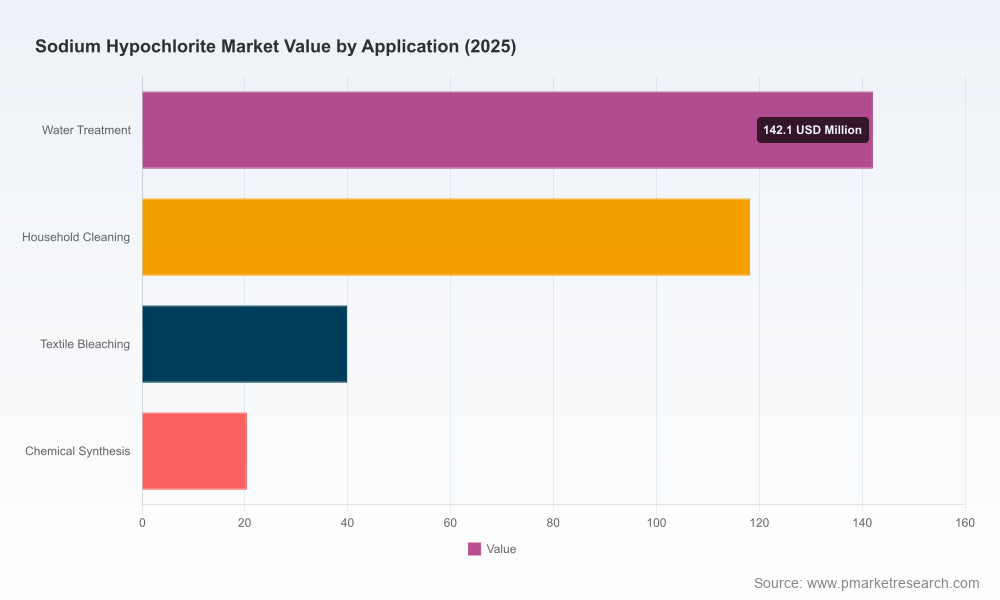

At a macro level the market has shifted materially over the past half‑decade. Following a period of recovery and demand acceleration from 2020 onward, global revenues registered meaningful growth to reach roughly USD 320.5 Million in 2025. Our projection through the 2026–2032 forecast horizon anticipates a steady compound annual growth rate of 4.9%, taking the market to approximately USD 445.7 Million by 2032. These headline multiples underpin the operational and strategic choices firms must make in the coming 12–36 months.

Sodium Hypochlorite Market

Growth momentum: The market’s recovery and steady forecasted CAGR reflect persistent demand from municipal water treatment and hygiene-driven consumption, combined with pockets of industrial uptake. Executives should treat this as an expansion window rather than a short-lived spike.

Sodium Hypochlorite Market

Volatility vectors: Growth masks important volatility drivers — upstream feedstock swings, regulatory interventions, and regional supply constraints — that will determine value capture across supply chains.

Strategic timing: 2026 is a planning inflection: near‑term decisions on contract terms, hedging, and tactical capacity should be aligned with medium‑term CAPEX and M&A plans informed by scenario‑based forecasting.

Feedstock dependency and input cost pass‑through — Chlorine feedstock and caustic soda remain primary cost drivers. Regional cost differentials and trade measures can quickly compress margins or create arbitrage opportunities for exporters/importers.

Regulatory pressure on chlor‑alkali operations — Environmental restrictions and permitting constraints — particularly in North America and parts of Europe — are tightening available chlorine capacity and can precipitate supply tightness.

Tariff and trade shocks — Recent tariff measures on caustic soda imports into Europe illustrate how trade policy alters competitive dynamics and requires rapid sourcing re-evaluation.

Labor and operational constraints — Staffing and operational limits at some chlor‑alkali facilities cap throughput, creating a hard constraint even where nominal capacity exists.

Product differentiation and sustainability — Demand is bifurcating toward formulations that balance efficacy with lower corrosivity and improved environmental profiles, creating premium niches.

The sodium hypochlorite market exhibits a moderate degree of concentration: the top three producers account for roughly 45% of supply, while the top five approach the mid‑50s percentage range. That structure creates a dual dynamic — sufficient scale among incumbents to influence feedstock sourcing and pricing, alongside meaningful headroom for regional and specialty competitors to win share through service, formulation, and distribution agility.

Market participants can be grouped, at a high level, into vertically integrated chlor‑alkali majors, merchant producers with regional footprint strength, and downstream formulators/distributors who control local aggregation and logistics. Notable incumbents and recent strategic moves include:

Olin Corporation — North America’s largest industrial bleach manufacturer; opened a new Texas facility in August 2025 to target southern municipal demand, signaling a capacity and logistics play focused on demand corridors.

Nouryon — Expanded European capacity (Sweden, May 2025) to serve water treatment and disinfection markets, reflecting regional demand prioritization.

BASF SE — Launched lower‑corrosivity, environmentally oriented grades (July 2025), demonstrating product‑level differentiation as a go‑to‑market strategy.

Solvay S.A. — Announced a strategic digital/technology partnership (September 2025) to optimize production processes, underscoring the productivity and sustainability upside of manufacturing digitalization.

The full study was structured to move beyond descriptive market sizing and provide operationally focused inputs that decision makers can deploy immediately. Key deliverables include:

High‑resolution demand forecasts across the 2026–2032 horizon, with scenario variants calibrated to feedstock price pathways and regulatory tightening assumptions.

Supply‑side mapping of global capacity, vintage, and technology (membrane vs. diaphragm vs. merchant dilution approaches), highlighting where incremental capacity can be brought online fastest.

Price‑sensitivity and margin models tying sodium hypochlorite economics to chlorine/caustic input moves and freight/tariff changes.

Supplier scorecards and a procurement playbook (tactics for short‑term spot coverage, rolling offtakes, and feedstock hedging prioritized by risk appetite).

M&A screening framework and a shortlist of archetypal targets by strategic rationale (capacity consolidation, channel access, technology uplift), supported by valuation sensitivity on EBITDA multiples under alternate demand scenarios.

Regulatory and sustainability impact maps aligned to regional permitting and environmental trends, plus a technical roadmap for lower‑corrosivity and lower‑emissions product development.

A digitalization and operations uplift template — use case ROI for process optimization, yield improvement, and predictive maintenance applied to chlor‑alkali and dilution operations.

Producers (integrated and merchant): Secure flexible feedstock sourcing, accelerate marginal capacity projects in markets with demonstrated demand resilience, and place priority on product formulations that reduce downstream handling costs for customers.

Distributors and formulators: Strengthen logistics and tank‑farm flexibility to arbitrage regional price spreads; differentiate through service (just‑in‑time delivery, custom formulations) rather than competing purely on commodity price.

Municipal buyers and utilities: Revisit allocation and rostering strategies to include multi‑year indexed contracts with volume flex, and build contingency inventories tied to clear release triggers for emergency procurement.

Investors and PE sponsors: Target bolt‑on consolidation in under‑served regional markets and evaluate assets with strong customer lock‑in and low capital intensity for rapid cash conversion.

Feedstock shortage or chlorine cluster shutdowns — Trigger: sustained chlorine supply constraints or major facility outages. Action: accelerate alternative sourcing, prioritize key accounts, and implement price‑indexed pass‑through clauses.

Tariff escalation — Trigger: additional import duties or trade barriers. Action: reconfigure supply chains, evaluate near‑shoring, and quantify landed cost shifts to support pricing decisions.

Regulatory tightening — Trigger: new emissions or discharge limits affecting chlor‑alkali operations. Action: model compliance timelines, adjust CAPEX phasing, and pursue technology upgrades or joint ventures for compliant capacity.

Demand shock (macroeconomic downturn) — Trigger: abrupt contraction in industrial demand or reduced municipal budgets. Action: convert spot exposure to contracted volumes, rationalize SKU offering, and temporarily pivot to downstream higher‑margin formulations.

This executive briefing surfaces the macro signals and strategic implications executives must consider entering 2026. To preserve the commercial integrity of actionable segmentation, granular region‑by‑region and application‑by‑application shares and pricing scenarios are intentionally omitted here. The full PW Consulting study contains those critical cell‑level datasets, supplier cost‑stacks, and proprietary scenario outputs that enable rigorous CAPEX approval, procurement renegotiation, and M&A due diligence — the very elements that convert awareness into value.

For decision teams preparing 2026 budgets, contract renewals, or strategic M&A plays, the report functions as both a map and toolkit: it identifies where risk is concentrated, where scale matters, and how to deploy capital and commercial leverage to preserve margin in the face of input and regulatory uncertainty.

Request the full report to access the granular segmentation and supplier‑level financial models that underpin the recommendations summarized here.

Schedule a workshop with PW Consulting to translate findings into a tailored 90‑day execution plan for procurement, operations, or M&A teams.

PW Consulting’s Sodium Hypochlorite Market study is built to inform the practical choices companies must make in 2026. If your mandate is to preserve margin, secure supply, or acquire differentiated assets in this space, the next action is to move from headline insight to the data‑driven scenarios and supplier models contained in the full analysis.

For detailed analysis of this topic, please visit the official page:Sodium Hypochlorite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com