2‑Ethylhexanoic Acid Market: Strategic Briefing for 2026 Decision‑Makers

As PW Consulting’s senior industry analyst, I present an executive introduction to our full 2‑Ethylhexanoic Acid Market study. This briefing synthesizes the practical, decision‑critical insights that corporate strategists, procurement chiefs, and portfolio managers need to act confidently in 2026. We demonstrate the analytic depth of the full report while deliberately withholding granular segment-level tables — a purposeful “trailer” designed to show what’s actionable and to invite access to the full dataset and models on our site.

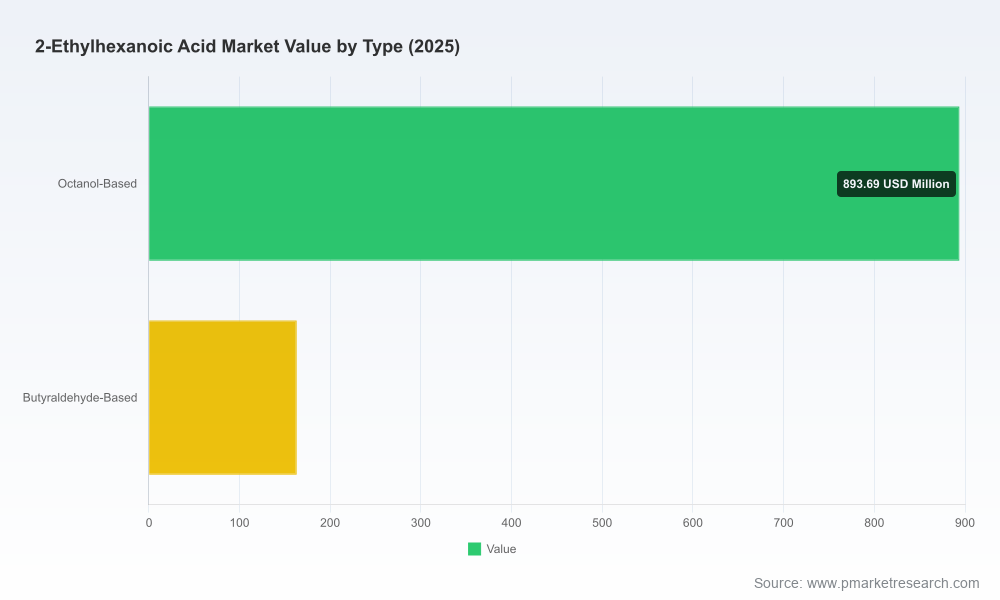

2-Ethylhexanoic Acid Market

Market snapshot — the macro facts that drive strategy

Our analysis uses 2025 as the base year and examines historical performance from 2020–2025 with a forward outlook through 2026–2032. At the macro level the market shows steady, resilient expansion: total industry revenues expanded from roughly USD 899 million in 2020 to about USD 1,057 million in 2025. Under our central scenario the market continues to grow at a compound annual growth rate (CAGR) of approximately 5.12% across the 2026–2032 forecast window, reaching a projected market size near USD 1.5 billion by 2032.

2-Ethylhexanoic Acid Market

Those headline numbers matter because they shift the strategic calculus for capital allocation: the market is neither hyper‑disruptive nor stagnant. Instead, it offers a mid‑cycle, investment‑grade growth profile where scale, cost competitiveness, and regulatory agility determine winners.

2-Ethylhexanoic Acid Market

Why this study matters for 2026 decisions

- Capex prioritization: With growth predictable and sustained, manufacturers and tollers must decide whether to pursue incremental expansions, brownfield debottlenecking, or targeted greenfield projects. Our report quantifies time-to-payback ranges and sensitivity to feedstock and tariff shocks.

- M&A and partnership targeting: Moderate market concentration and clear pockets of regional specialization create opportunities for bolt‑on acquisitions and JV structures. We identify the capability gaps that premium buyers should prioritize (technical grade diversification, downstream salt manufacturing, logistics footprint).

- Commercial strategy: Procurement and offtake negotiations should reflect not only volumetric supply-demand balances but also emerging regulatory cost components. We provide commercial playbooks that align pricing, contract duration, and penalty structures to market cyclicality.

- Risk and compliance planning: Recent regulatory developments change product stewardship obligations. Our regulatory heat‑map enables companies to prioritize testing, labeling, and substitution R&D budgets.

Report contents — what you will find in the full study

The full PW Consulting report is structured to be directly operational for leadership teams. Highlights include:

- Top‑level market sizing and a transparent forecast model (historical 2020–2025; forecast 2026–2032) with scenario toggles for feedstock volatility, regulatory shocks, and demand slippage.

- Demand drivers and end‑use analysis across plasticizers, stabilizers, coatings, lubricants and specialty niches — including growth vectors and substitution risk assessments. (Note: we intentionally do not disclose segment tables in this preview.)

- Comprehensive supply landscape: global production capacities, recent and planned expansions, and an interactive supplier map for rapid sourcing decisions.

- ROI and NPV templates for capacity projects calibrated to prevailing capex and operating cost assumptions.

- Regulatory and safety matrix detailing compliance timelines, required testing, labeling implications, and cost estimates for mitigation pathways.

- Competitive benchmarking, vendor scorecards, and an M&A playbook with valuation multiples consistent with current market realities.

- Procurement levers and contract archetypes for offtake, tolling, and captive vs merchant supply strategies.

Market dynamics driving near‑term action

- Feedstock and cost environment: Propylene feedstock price stability across Asia through 2025 materially supported synthetic production economics, compressing one key source of margin volatility. Our stress tests show the degree to which a 10–20% swing in propylene impacts producer cash cost curves across regions.

- Supply shifts: Capacity moves in the region have already altered operational sourcing logic for many buyers. The installation of new production lines and debottlenecking initiatives are reshaping lead‑times and spot availability.

- Regulatory overlay: A wave of regulatory action is converging on this chemistry: a US EPA final TSCA test rule announced in January 2026, California’s Proposition 65 listing for reproductive toxicity in 2025, Oregon’s inclusion on its High Priority Chemicals of Concern list effective January 1, 2025, and the application of a 2.5% MFN tariff on the relevant HTS code effective January 2026. Together these increase compliance costs, elevate reputational risk, and nudge some end‑use buyers toward substitution or reformulation strategies.

For manufacturers and downstream users the implication is clear: regulatory risk is no longer theoretical. It is a cash‑flow consideration that should be incorporated into product costing, contract design, and R&D prioritization in 2026.

Competitive landscape — who matters and why

The sector structure combines global scale players, specialized producers, and regional champions. Overall market concentration is moderate: the top three firms account for a meaningful but not dominant share, and the top five consolidate less than a majority — a structure that creates space for agile challengers.

- BASF SE (Ludwigshafen, Germany): A global leader with integrated Verbund capabilities and recent capacity expansion via a joint‑venture line in Kuantan. These moves materially increase Asia‑Pacific supply optionality and strengthen BASF’s leverage in downstream plasticizer and lubricant value chains.

- Perstorp Holding AB (Perstorp, Sweden): Owner of the world’s largest single production capacity for this chemistry, Perstorp is a natural anchor for buyers seeking volume and technical grade breadth.

- The Eastman Chemical Company (Kingsport, TN, USA): Positions the acid as a strategic intermediate in specialty chemistries — a role that supports higher‑margin derivatives and closer customer relationships.

- OXEA GmbH & OQ Chemicals (Oberhausen, Germany): Both leverage distinct process routes; their economics and feedstock linkages differ in ways that matter under stress scenarios.

- KH Neochem, Shenyang Zhangming, Beijing Lys, Elekeiroz, Jiangxi JYT and others: Regional and national champions — especially in Asia and Latin America — supply industrial and specialty grades, often with tailored logistics and salt‑making capabilities that multinational buyers rely on for continuity.

Recent corporate developments offer a practical cue: the BASF PETRONAS Chemicals inauguration of a second 2‑ethylhexanoic acid line at Kuantan (October 2024), which doubled that site’s annual capacity, exemplifies how targeted capacity moves can recalibrate regional supply balances and pricing dynamics.

Strategic plays we recommend for 2026

- For producers: Prioritize flexibility over sheer scale. Small brownfield debottlenecks and tolling partnerships deliver faster paybacks than long‑lead greenfield projects in the current regulatory environment. Invest in compliance labs and product stewardship capabilities to reduce trade friction and preserve margin.

- For buyers: Diversify contractual mix: combine short‑term spot flexibility with medium‑term fixed offtake and a small share of strategic reserves. Renegotiate price indexation clauses to reflect feedstock linkages and tariff pass‑through.

- For investors: Target assets that provide integration into downstream salt and additive manufacturing — these capture more of the value chain and insulate returns from feedstock cycles.

- For regulators and compliance teams: Accelerate testing and substitution roadmaps where feasible; early engagement reduces product withdrawal risk and avoids costly last‑minute reformulations.

How PW Consulting supports execution

Our full report is accompanied by executable tools: an interactive Excel model with scenario toggles, supplier scorecards, an M&A due‑diligence checklist specific to this chemistry, and an implementation timeline matrix for compliance actions. We also offer a bespoke advisory package that bundles our data models with on‑site workshops to align commercial, technical, and regulatory teams.

Next steps — where to find the full intelligence

This briefing is a preview of the depth and operational focus of the full PW Consulting 2‑Ethylhexanoic Acid Market study. To access the complete datasets — including full segment breakouts, regional tables, capacity maps and downloadable financial models — please visit our report page. The full materials provide the granular inputs your CFO, head of strategy, and operations chief will need to finalize 2026 capital and commercial plans.

For bespoke questions or to commission a tailored scenario analysis, contact PW Consulting and request the industry briefing package. Our team is prepared to convert the report’s insights into a 90‑day action plan that aligns with your organization’s risk tolerance and growth objectives.

For detailed analysis of this topic, please visit the official page:2-Ethylhexanoic Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com