Battery Innovation Trends Drive the EV Battery Testing Market at a Robust 21.73% CAGR

Other |

2026-06-18 09:14:47

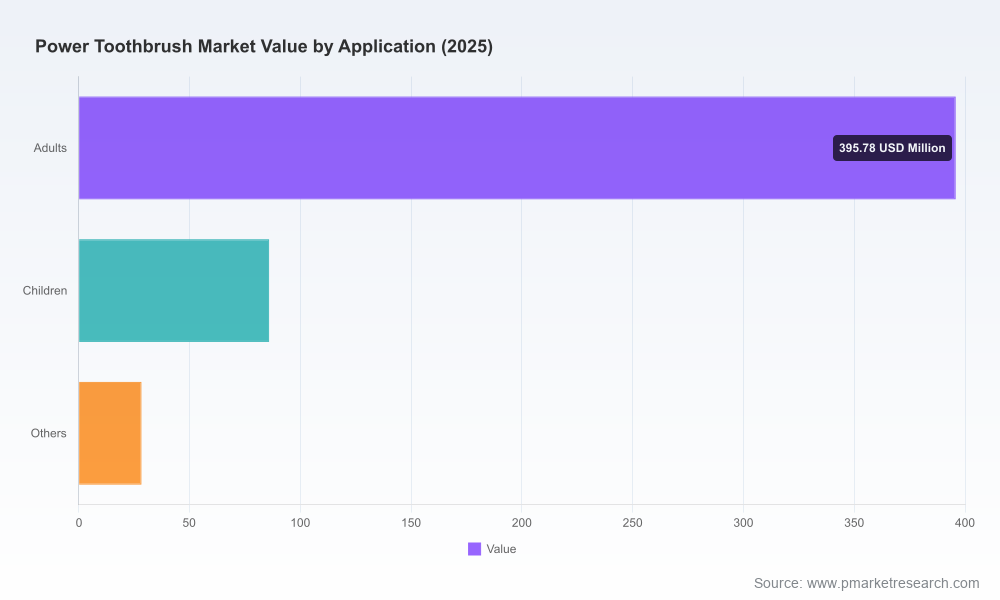

PW Consulting’s new Power Toothbrush Market study (base year 2025; historical 2020–2025; forecast 2026–2032) is designed as an operational intelligence package for executive teams setting strategy in 2026. The global market reached USD 510 million in 2025 and, at a modeled compound annual growth rate (CAGR) of 5.5% across the forecast window, is projected to approach three‑quarters of a billion dollars by 2032. Those headline numbers matter: they justify renewed investment in product innovation, channel expansion and regulatory programs — but only when backed by the right tactical playbooks. This preview explains the strategic value of the full study without disclosing the granular segmentation tables reserved for subscribers.

Power Toothbrush Market

The market’s expansion is being driven by the intersection of clinical validation, consumer premiumization and digital engagement. Premium electric offerings continue to capture share of wallet as consumers trade up from basic hygiene to devices positioned as delivering superior clinical outcomes or integrated oral‑health experiences. Simultaneously, integration with mobile apps and service layers (brush head subscription, clinical tracking) is creating recurring revenue pathways that change the economics of acquisition.

Power Toothbrush Market

Regulation and standards are a structural influence. In the U.S., powered toothbrushes commonly fall under FDA Class II pathways, and testing to ANSI/ADA standards is a market access and trust gate in multiple markets. Emerging sterilization master files and pilot programs also open possibilities to reduce reliance on legacy sterilants and to meet sustainability goals — a competitive differentiator for larger manufacturers and an operational requirement for OEMs supplying clinical channels.

Power Toothbrush Market

Manufacturing geography matters. Component and assembly clusters in China (notably Guangdong) supply the majority of handles and heads to global brands; this concentration enables cost efficiency but also amplifies supplier concentration risk and intellectual property leakage concerns. Smart sourcing and quality‑assurance frameworks are therefore strategic rather than tactical choices.

The market shows significant concentration at the top (three‑ and five‑firm concentration metrics indicate an upper‑tier oligopoly). That said, the field is not static: established multinational consumer health leaders sit alongside fast‑growing challengers and specialized clinical brands. The report synthesizes strategic positioning across a cross‑section of market actors to reveal where advantaged plays exist.

Recent developments underscore how quickly competitive dynamics can change. Notable industry events — including product certifications and major new range launches from global incumbents — repeatedly reset expectation levels for both consumers and dental professionals. The report’s competitive chapter maps these events to probable share and margin outcomes under multiple scenarios.

The full PW Consulting study is built to be immediately actionable for corporate teams. Highlights of the deliverables include:

These deliverables are supported by proprietary forecasts and an interactive dataset that allows modelers to test assumptions against alternate growth paths. Note: while the report contains granular segmentation and regional breakdowns, those detailed cells are intentionally omitted from this public preview; premium subscribers receive the full tables and the downloadable financial model.

Corporate leaders should treat this report as both a diagnostic and an implementation toolkit. Use the forecasting models to stress‑test capital allocation scenarios, the regulatory roadmap to align R&D and legal timelines, and the supplier heatmaps to prioritize procurement contingencies. For BD and M&A teams, the report’s acquisition screening reduces search cost by identifying capability gaps where bolt‑on deals deliver near‑term payback.

In practice, we recommend a 90‑day planning sprint: align product development and regulatory resources within month one; finalize supplier contingencies by month two; and run pilot go‑to‑market tests in months two to three to validate price and subscription assumptions ahead of a full roll‑out in H2 2026.

This preview demonstrates the scope and actionable nature of PW Consulting’s Power Toothbrush Market research: a forecasted market expansion from a solid 2025 base, a predictable growth trajectory at a mid‑single‑digit CAGR, and a competitive environment where regulatory plays, supply chain design, and clinical differentiation determine winners. We intentionally withhold the full segmentation cells and granular regional/application figures here to preserve the value of the primary dataset and to provide subscribers with exclusive, downloadable models that support immediate decision‑making.

To access the full dataset, downloadable financial models, competitor scorecards and the regulatory playbook that turn these strategic observations into executable plans for 2026, please visit the PW Consulting report page and request the Power Toothbrush Market study.

For detailed analysis of this topic, please visit the official page:Power Toothbrush Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com