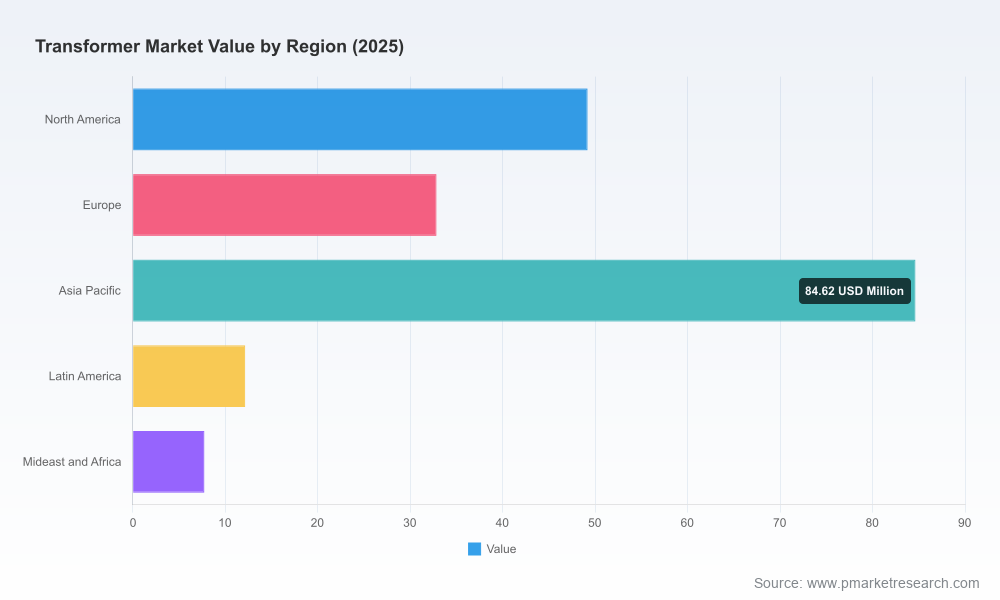

Transformer Market — 2026 Strategic Preview

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present this executive preview of our in-depth Transformer Market study. This article is a strategic “trailer”: it demonstrates the analytical depth and decision-ready frameworks embedded in the full report while deliberately withholding granular segmentation tables and proprietary scorecards. Use it to orient 2026 investment, procurement, and M&A decisions — then consult the full report for the detailed inputs you’ll need to execute.

Transformer Market

Why this research matters for 2026 decisions

The transformer market is in a structural phase shift. Using 2025 as the base year, our historical series (2020–2025) shows a steady rise from a post‑pandemic trough to a robust market size in 2025. From that base, our forecast for 2026–2032 models a compound annual growth rate (CAGR) of 7.0% (USD, revenue denominated in Million), projecting marked expansion through 2032. This trajectory reflects the combined effects of grid modernization, electrification of industry and transport, hyperscale data center growth, and the accelerating pace of renewable integration.

Transformer Market

For executives evaluating capital allocation in 2026, three implications are immediate: (1) near‑term procurement and lead‑time risk will influence supplier selection and inventory policies; (2) product mix and material strategies will materially affect margin trajectories as raw material cost volatility persists; and (3) competitive positioning and consolidation dynamics create specific windows for strategic M&A and partnerships. Our report quantifies these dynamics and translates them into decision frameworks you can operationalize this year.

Transformer Market

Macro drivers and sector stress points

- Demand drivers: Grid expansion, renewables and storage interconnections, industrial electrification, and data center rollouts are the core growth engines. These factors are persistent through our 2026–2032 forecast horizon and underpin the 7.0% CAGR.

- Regulatory push: Efficiency rules finalized by the U.S. Department of Energy are reshaping design choices. The standard’s real‑world effect forces a portion of the market toward higher‑efficiency core materials and manufacturing techniques — an outcome we model across multiple scenarios.

- Trade and tariff exposure: Recent trade measures have raised effective import costs on core inputs, tightening the margin calculus for globally sourced cores and laminations. These policies create short‑term pricing pressure and favor onshore capacity investments in several markets.

- Raw material volatility: Copper and electrical‑steel price movements are primary translatable risks. Elevated copper prices in 2025, and GOES (grain‑oriented electrical steel) cost inflation from 2020–2025, have already contributed to higher unit prices and are included in our sensitivity models.

- Supply chain & lead times: Lead times for large power transformers and generator step‑up units have ballooned under the dual stresses of demand spikes and constrained manufacturing capacity. Our operational playbooks prioritize lead‑time mitigation strategies that procurement and program managers can implement immediately.

What the full report delivers (practical, action‑oriented contents)

The PW Consulting Transformer Market study is designed for executives and functional leaders who must make measurable choices in 2026. We organize the report around three practical pillars: intelligence, options, and execution.

- Intelligence: Transparent market sizing and top‑down/ bottom‑up reconciled forecasts (base year 2025; historical 2020–2025; forecast 2026–2032), market concentration measures, and scenario analyses that stress test demand and price paths against regulatory and material‑cost shocks.

- Options: Supplier benchmarking and capability mapping, product technology roadmaps (material and design tradeoffs), and commercial models that show where premium pricing vs. high‑volume strategies are appropriate.

- Execution: Procurement playbooks, manufacturing footprint decision tools, inventory and hedging templates, and an M&A playbook with valuation sensitivities tailored to the transformer business.

Each section includes reproducible models and templates — from unit‑cost build‑ups that capture copper and steel price pass‑through to lead‑time impact matrices for multi‑year project planning. The report deliberately stops short of publishing proprietary client scorecards; instead, it supplies the methodology and anonymized benchmarks so buyers can apply them to vendor selection immediately.

Competitive landscape: the tactical view for 2026

The market exhibits moderate concentration: the leading three and five suppliers do not dominate the sector in the way seen in some heavy‑equipment markets. Instead, a mix of global engineering majors and specialized regional manufacturers creates a marketplace where technological differentiation, delivery reliability, and service footprint matter as much as scale.

- Virginia Transformer Corporation (Roanoke, VA): As a sizeable U.S.‑owned custom transformer manufacturer with a strong North American focus, Virginia is positioned to capture demand tied to localized procurement and fast response projects. Recent contract wins with utilities illustrate the value of domestic manufacturing and rapid commissioning capabilities — an increasingly important commercial lever as lead times extend.

- ERMCO (Dyersburg, TN): A leader in low‑voltage distribution solutions, ERMCO’s strength is its deep distribution expertise and component manufacturing. For buyers prioritizing distribution reliability and replacement cycles, ERMCO remains a logical anchor supplier.

- Foster Transformer Company (Cincinnati, OH): Specializing in isolation and low‑voltage control transformers, Foster is a niche operator with stable demand from industrial and commercial segments. Their value lies in application‑specific customization and rapid engineering cycles.

- Global engineering majors (Hitachi Energy, Siemens Energy, ABB, GE Vernova, Eaton, Schneider Electric): These players combine broad product portfolios with global delivery footprints and substantial R&D capacity. Their strategies differ: some compete on high‑voltage, grid‑scale systems and complex turnkey solutions; others emphasize digital services, lifecycle management, and integrated grid offerings. Recent activity (for example, acquisitive moves to bolster medium‑voltage capabilities) signals continued consolidation at particular capability nodes rather than across the whole value chain.

Strategic takeaways: partnerships with global OEMs are the quickest route to access turnkey solutions and lifecycle services; regional specialists offer speed and price advantages for replacement and retrofit work. Our supplier scorecards and tactical sourcing rules (in the full report) map these tradeoffs to contracting templates and risk allocation clauses.

Operational and strategic recommendations for 2026

- Hedge material exposure and redesign for substitution: Implement tiered sourcing for copper and electrical‑steel, and accelerate design work that can substitute higher‑cost materials without sacrificing regulatory compliance. Model the cost–benefit of amorphous alloy vs. GOES choices under multiple tariff and price scenarios.

- Lock in critical lead times: Prioritize long‑lead items and formalize backlog hedges with preferred suppliers. Where flexibility is paramount, evaluate modular or factory‑assembled substation solutions to compress schedule risk.

- Revisit footprint decisions: Tariffs and localized procurement preferences make near‑market capacity attractive. Use our footprint decision tool to compute NPV under scenarios that include tariffs, labor cost shifts, and capital intensity.

- Pursue targeted consolidation and capability M&A: Given the market’s mid‑level concentration, bolt‑on acquisitions that expand service networks or specific medium‑voltage capabilities can be value‑accretive. Use the provided valuation sensitivities to prioritize targets with predictable aftermarket revenue.

- Embed digital aftermarket and performance guarantees: Performance‑based contracts and remote monitoring extend lifetime value. OEMs and utilities that combine hardware with analytics capture higher lifecycle margin and reduce unplanned outages.

- Engage regulators and shape standards: Actively participate in efficiency and grid‑interconnection rulemaking to anticipate compliance costs and potential incentives. Regulatory clarity materially reduces capital‑planning uncertainty.

How to use this preview and next steps

This preview synthesizes the strategic contours you need to act in 2026: a clear growth path captured by our 7.0% CAGR forecast, material‑driven margin risk, extended lead times, and a competitive field defined by both global majors and specialized regional players. The full PW Consulting Transformer Market report contains the proprietary segmentation tables, regional and application breakdowns, downloadable financial models (USD, Million), supplier scorecards, and contract templates that we intentionally do not publish here.

If your 2026 agenda includes capital projects, supplier consolidation, or targeted M&A, the full dataset and executable playbooks will accelerate decision cycles and reduce execution risk. Contact PW Consulting to access the complete report, scenario model packages, and a tailored briefing for your organization’s strategic priorities.

— PW Consulting, Strategy & Industry Insights

For detailed analysis of this topic, please visit the official page:Transformer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com