Synthetic Pesticide Inert Ingredients Market Overview: Key Drivers and Challenges

Other |

2026-04-30 06:35:24

The LNG‑as‑bunker market is entering a material inflection point that demands board‑level attention in 2026. Our PW Consulting baseline shows the market expanding from USD 90.0 Million in 2020 to USD 112.0 Million in 2025 (base year), with an anticipated acceleration as the sector transitions from pilot deployments to commercial scale. Under our central forecast (2026–2032), the market grows at a compound annual growth rate (CAGR) of 28.0%, reaching an estimated USD 646.37 Million by 2032. In other words, 2026 is not merely the next year on the calendar — it is the year when strategic choices made by shipowners, ports, fuel suppliers and financiers will determine who captures the dominant share of a rapidly expanding value pool.

LNG as a Bunker Fuel Market

Timing matters: the forecast jump from USD 112.0 Million in 2025 to a substantially larger market in 2026 signals a window in which first‑mover investments (in infrastructure, contracting frameworks and fleet retrofits) are likely to achieve outsized returns.

LNG as a Bunker Fuel Market

Infrastructure is the choke point: industry data show LNG bunkering availability across roughly 191 ports worldwide and a bunker vessel fleet measured in the low‑dozens today, with additional units on order. These constraints mean that capacity deployment and logistical design will determine commercial reach more than simple fuel pricing.

LNG as a Bunker Fuel Market

Regulatory tailwinds are real: policy shifts — for example, the removal of restrictions on ship‑to‑ship LNG transfers by a national energy authority in early 2025 and the opening of additional bunkering licenses by a major port authority in January 2026 — are lowering entry barriers and changing the calculus for investment versus partnership.

Fleet adoption is accelerating: by the end of 2025 the number of LNG‑fueled vessels in operation had expanded materially, reflecting both newbuilds and retrofits; this creates sustained, predictable demand that underpins project bankability.

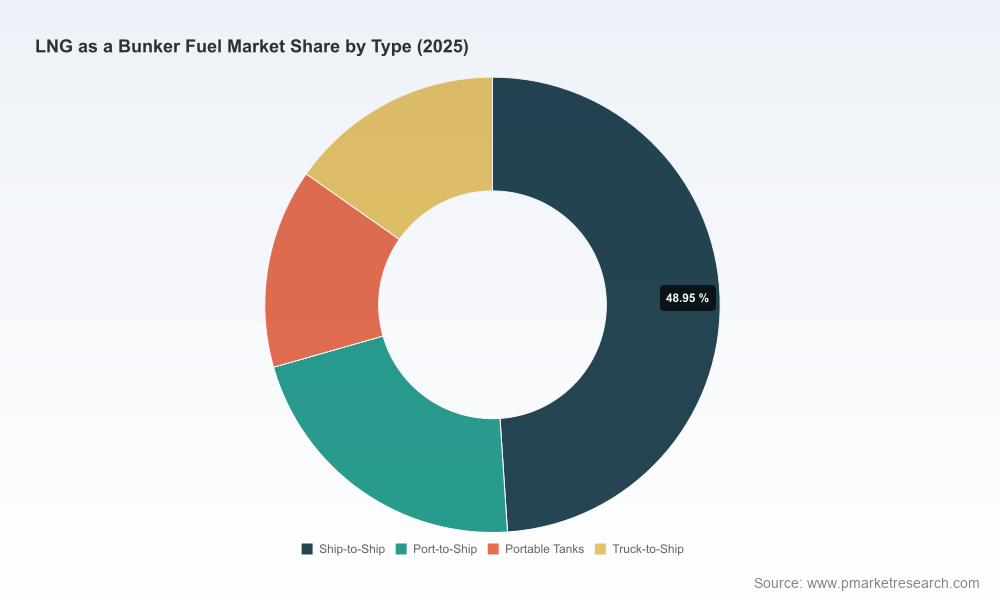

Strategic complexity: choices around asset mix (shore tanks, barges, truck‑to‑ship), fuel type (conventional LNG vs bio‑LNG) and commercial structures (term supply, spot, hybrid contracts) will define margins and competitive positioning.

This research is built as an operator’s toolkit, not a high‑level PowerPoint. Key deliverables designed to support 2026 execution include:

Clear, auditable market sizing and a seven‑year forecast (2026–2032) that allows CFOs to test capital deployment timings against multiple adoption curves.

Port readiness and logistics playbooks that map infrastructure bottlenecks and recommended interventions for shore‑side operators, ports and local authorities.

A decision matrix for asset selection (small‑scale liquefaction, shore storage, dedicated barges, truck‑to‑ship solutions) that ties technical choices to commercial models and regulatory regimes.

Commercial contracting templates and negotiation levers for term offtake, fuel quality clauses (including biomethane blending) and liability allocations for ship‑to‑ship operations.

Risk‑weighted financial models and sensitivity analyses that let financiers and project sponsors stress‑test projects under price, demand lag and regulatory change scenarios.

A regulatory tracker and stakeholder engagement playbook, including templates for licensing applications and public‑private partnership structures in key jurisdictions.

A competitor benchmarking module and partnership roadmap to identify the right co‑development models — from EPCM partners to local port operators and fuel aggregators.

The market is already coalescing around a set of specialist operators and vertical integrators whose strategic moves signal where competition and value will concentrate.

Seaside LNG (Houston, TX) — Their integrated approach (liquefaction, storage and Jones Act‑compliant bunkering barges) illustrates the value of owning the shore‑to‑barge value chain in the U.S. market. Recent operational achievements, including a high‑profile SIMOPS bunkering of a 15,000 TEU container vessel in mid‑2025, demonstrate the feasibility of large‑vessel service and create a blueprint for rapid scale‑up.

Titan Clean Fuels (Amsterdam) — As a supplier blending conventional LNG with biomethane and operating a fleet of small‑scale bunker vessels, Titan signals that fuel quality and decarbonization credentials will be differentiators in Europe and global trade lanes.

Harvey Gulf International Marine (New Orleans) — Their focus on dedicated bunker operations at strategic Gulf ports underscores the premium on localized, reliable supply chains for offshore and nearshore operations.

JAX LNG (Jacksonville) — Small‑scale liquefaction paired with truck‑to‑ship capability illustrates an alternative commercialization path that minimizes initial capex while delivering flexible supply to regional customers.

These profiles show two persistent strategic vectors: (1) integrated, asset‑heavy players who secure margins through control of conversion and last‑mile delivery; and (2) agile, service‑oriented providers who compete on speed, fuel mix and partnership models. Both are viable — the choice depends on balance‑sheet capacity, market access and regulatory context.

Regulatory openings: Port authorities and national regulators are actively enabling more flexible bunkering arrangements. For example, a major port authority invited applications for additional LNG bunker supplier licenses in January 2026, explicitly supporting sea‑based reloading operations.

Operational milestones: New bio‑LNG supply services and the commissioning of STS bunkering facilities in emerging hubs (including recent launches in Europe and India) indicate that the supply map is expanding beyond traditional gateways.

Fleet and vessel supply: The existing global count of LNG bunkering vessels and the number on order point to a near‑term capacity expansion, yet the pace of vessel deployment is likely to lag peak demand windows without coordinated investment.

To convert market growth into sustainable advantage, organizations should prioritize five decision levers:

Network strategy: Decide where to own assets versus where to form exclusive partnerships. Use port readiness scoring to prioritize initial investments.

Asset configuration: Align asset type (shore tank, barge, trucking) to customer segmentation and contract tenure. Shorter contracts favor modular, lower‑capex solutions.

Fuel differentiation: Build a roadmap for bio‑LNG and carbon credentials. Early commitments to low‑carbon blends will create a commercial premium with certain shipowners and charterers.

Commercial architecture: Standardize contractual language for price indexation, quality, liability and emergency response. Create hybrid contracting options to manage demand variability.

Regulatory & stakeholder engagement: Proactively shape licensing and safety standards in priority ports; securing early approvals materially shortens the time to market.

Fast‑adoption: Operators that commit capital to multiple gateways and secure term offtake capture scale economies, logistics control and contracting power — but accept higher early capital intensity.

Managed growth: Firms that adopt a partnership‑led model (local liquefaction + shared barge capacity) reduce upfront capex and retain upside via variable contracts, at the cost of lower absolute margin.

Selective niche play: Suppliers focused on differentiation (bio‑LNG, specialized retrofits) command premium pricing in targeted corridors but depend on regulatory support and certification pathways.

Our report is engineered to move executives from strategic intent to executable plans. It provides the market maps, commercial playbooks, regulatory trackers and financial models necessary to underwrite projects and negotiate from a position of strength. We intentionally withhold granular segment tables and certain sensitive model outputs from this introduction to preserve strategic exclusivity — full segmentation, port‑level readiness scores, contract templates and downloadable financial models are available in the complete report.

If your organization is evaluating LNG bunkering investments, fleet conversions, or strategic partnerships in 2026, the time to act is now. PW Consulting can run an accelerated 8–12 week “Go‑to‑Bunker” engagement that delivers a prioritized investment roadmap, term‑sheet templates and a three‑year roll‑out plan aligned to your balance‑sheet and risk appetite. Contact our team to obtain the full report and the underlying data tables that support our forecasts and scenario analyses.

For detailed analysis of this topic, please visit the official page:LNG as a Bunker Fuel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com