Skin Care Product Market Market Dynamics and Future Opportunities Analysis

Other |

2026-01-16 11:59:55

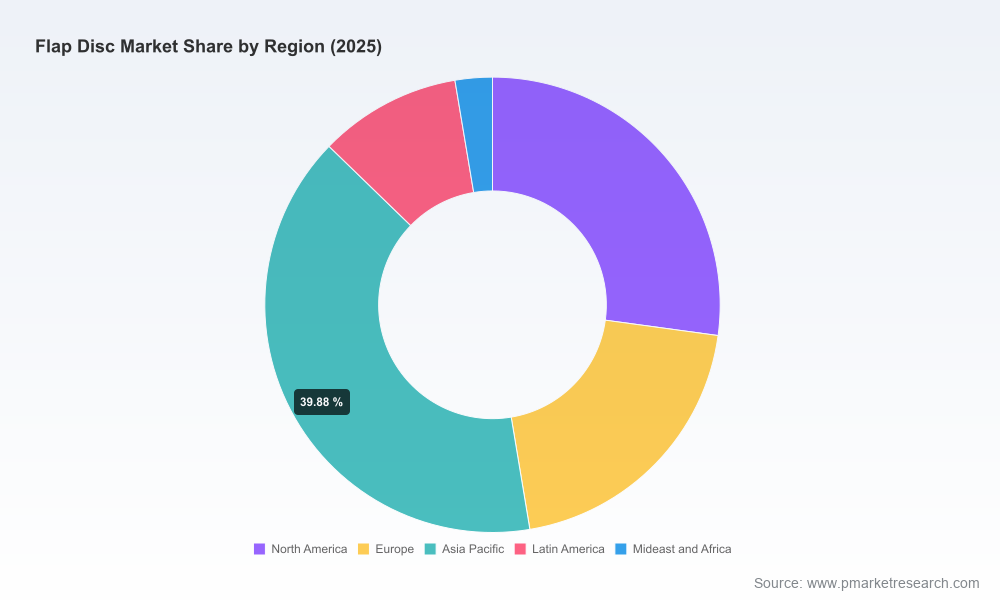

As organizations set strategy for 2026, the flap disc market presents a rare blend of steady growth, concentrated competitive dynamics, and accelerating product- and channel-level disruption. This market note — a strategic “trailer” drawn from PW Consulting’s full Flap Disc Market study — summarizes the macro trajectory, competitive architecture, and decision-focused implications you need to frame investments, partnerships, and portfolio moves next year. To preserve the commercial value of our primary intelligence, we intentionally omit the granular regional and application splits found in the full report; access to that segmented data is available in the complete study.

Flap Disc Market

Using 2025 as the base year, our market model traces the flap disc market from a measured recovery phase in the early 2020s through a structurally expanding market. Measured in USD Million, the market expanded from roughly 4,023 in 2020 to about 5,329 in 2025. Our scenario-based forecasts for 2026–2032, driven by demand linked to metalworking, industrial maintenance, and advanced manufacturing, project continued growth to nearly 7,948 by 2032. The compound annual growth rate underpinning the forecast horizon is 5.88%.

Flap Disc Market

Why this matters for 2026 planning: the market is large enough to justify scale investments, but growth is not so hyperbolic that first-mover, high-risk gambits are required. Instead, disciplined, capability-focused moves (innovation in abrasives chemistry, channel modernization, selective capacity expansion) will disproportionately capture share versus broad, undifferentiated expansion.

Flap Disc Market

The flap disc market shows a skewed competitive landscape where top firms hold a majority share of organized demand. Our concentration metrics indicate meaningful market power residing with the three- and five-firm groups (CR3 ≈ 55%, CR5 ≈ 65%). From a practical standpoint, this creates a two-speed field:

For incumbents, concentration supports margin preservation through premiumization, but it also elevates the value of distribution intimacy and specification-level influence with OEMs. For challengers or new entrants, opportunities exist in niche technical differentiation (e.g., low-dust formulations, non-woven/phazer offerings), aftermarket service bundling, or as bolt-on targets for established players seeking faster route-to-market in underserved subsegments.

The competitive set can be read as three overlapping archetypes, each with distinct 2026 implications:

As you evaluate 2026 tactics, consider how the following representative company profiles map to these archetypes (profiles available in the full study): global leaders with premium product lines; European specialists delivering custom-engineered discs; U.S. firms focused on performance and durability for metalworking; and Chinese OEMs with extensive contract-manufacturing footprints. Each group carries different M&A, channel, and pricing dynamics that will shape partner selection and competitive response strategies.

Our research highlights four pockets of near-term value capture:

For leadership teams preparing budgets and M&A pipelines in 2026, PW Consulting recommends prioritizing three actionable levers:

The market’s apparent stability masks concentrated risks that can materially alter outcomes if unhedged:

PW Consulting’s comprehensive Flap Disc Market study goes beyond this preview to provide the operational intelligence that underpins confident 2026 decisions. Key deliverables include:

We designed the report to be a decision-support tool: downloadable models, executive-ready slides, and a prioritized roadmap for near-term pilots and longer-term capability investments.

The flap disc market in 2026 is large, growing at a mid-single-digit CAGR, and sufficiently concentrated to reward strategically coherent moves. Success next year will not come from generalized scale alone, but from carefully sequenced investments — product innovation that captures total-cost advantage, channel modernization that secures demand visibility, and targeted M&A that closes capability gaps. With sensible scenario planning around raw materials and trade, leaders can convert the predictable growth profile into differentiated margin expansion.

To unlock the full segmentation matrices, supplier scorecards, and downloadable forecast models that inform precise capital allocation and commercial plans, consult the full PW Consulting Flap Disc Market report. The granular intelligence and proprietary datasets within that study are intentionally curated to support the high-confidence decisions your leadership team will make in 2026.

For detailed analysis of this topic, please visit the official page:Flap Disc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com