Saccharin Market — Strategic Outlook for 2026 Decision‑Makers

Executive snapshot

As companies plan investment and commercial strategies for 2026, saccharin re-enters boardroom conversations not as a legacy sweetener, but as a strategically relevant ingredient across food & beverage, pharma, and specialty industrial uses. Our PW Consulting Saccharin Market study (base year 2025; historical window 2020–2025; forecast 2026–2032) shows the market resuming robust expansion: the global saccharin market grows from a 2025 revenue base (USD, Million) to materially higher levels by 2032 under a 7.84% compound annual growth rate. This trajectory is driven by stable regulatory authorizations in major markets, renewed product launches, and structural supply‑chain dynamics originating in Asia.

Saccharin Market

Why this study matters in 2026

Three macro truths underpin the advice firms need for 2026 decisions:

Saccharin Market

- Growth momentum is measurable and sustained. The market recorded steady expansion over 2020–2025 and, on our forecast path, increases meaningfully through 2032. For commercial planning this means demand visibility for sourcing, pricing and capacity investments over a multi‑year window.

- Regulatory stability unlocks deployable strategies. Authorities in principal jurisdictions continue to maintain saccharin within authorized food additive frameworks (for example, longstanding FDA controls and a recent EU re‑evaluation that maintained authorization under current specifications). That legal clarity eliminates a major “showstopper” and permits tactical moves—new SKUs, label claims, or private‑label commitments—without binary regulatory risk in the near term.

- Supply‑side concentration and cost dynamics create opportunities and vulnerabilities. Production advantages in certain countries and the availability of low‑cost raw materials mean buyers can engineer near‑term margin improvements, while sellers can pursue selective value capture by differentiating on quality, certifications and traceability.

High‑level market health (what the numbers imply)

Using the 2025 base year and our 2026–2032 forecast run, the study quantifies the growth conditions companies will confront in 2026: markets that are expanding at an annualized rate in the high single digits, with total addressable revenue rising significantly by the end of the forecast horizon. For procurement and commercial leaders this implies a planning environment where volume commitments can be locked in with predictable upside, yet pricing dynamics remain sensitive to raw material cycles and regional capacity movements.

Saccharin Market

Strategic imperatives for 2026

- Reassess sourcing strategy from a total cost and resilience perspective. The report provides a supply‑risk heatmap and supplier segmentation framework that supports shifting from transactional buys to bilateral or multi‑sourced contracts incorporating inventory buffers, take‑or‑pay elements, and conditional price collars.

- Match product positioning to regulatory and consumer signals. With regulatory frameworks stable in major markets, companies should test higher‑value claims (clean‑label, high‑purity grades for pharmaceuticals or specialized beverage blends) in pilot geographies before scaling globally.

- Design capex and M&A playbooks around purity and certification. Firms with aspirations to move up the value chain should prioritize assets or partners that hold food‑grade and pharmaceutical certifications, or that can demonstrate backward integration in raw materials to secure margins.

- Embed scenario planning in commercial contracts. Given the supply concentration in certain geographies and potential raw material volatility, commercial teams should use the report’s scenario models to size flexible contract language and to calibrate hedging strategies for 12–36 month horizons.

Competition and supplier landscape — what matters

The competitive landscape is mixed: a base of specialized regional producers, a handful of global exporters, and laboratory/reagent suppliers serving niche industrial or R&D demand. The market is not a monopolistic arena; it remains accessible to well‑positioned mid‑sized players that can differentiate through quality, certifications, or logistics. The report contains deep profiles and strategic assessments of the following representative companies (select examples):

- Blue Jet Healthcare Ltd (Mumbai) — India’s largest saccharin sodium manufacturer by installed capacity; notable for backward integration of raw materials and a focus on global healthcare and food channels.

- HENAN KAIFENG PINGMEI SHENMA XINGHUA FINE CHEMICAL CO., LTD. (Kaifeng) — a large‑scale Chinese producer with multiple product forms, broad export reach and several ISO certifications, underscoring scale and regulatory compliance advantages.

- NS Chemicals (Navi Mumbai) — a manufacturer with product breadth across saccharin and chlorinated intermediates, serving pharmaceuticals and agro‑related customers, emphasizing regulatory approvals and FDA credentials.

- CDH Fine Chemical, Foodchem, JMC Fine Chemicals (KISCO), Spectrum Chemical, Otto Chemie — each brings complementary strengths: purity credentials, global distribution networks, laboratory‑grade offerings, or long‑standing trade relationships in food and pharma channels.

Recent corporate moves reinforce these themes: late‑2025 product launches and awards underscore continued innovation and a focus on high‑purity grades for food and pharmaceutical use. These actions signal that incumbents are aiming to capture premium segments even as broader demand grows.

Operational playbook included in the report (practical deliverables)

PW Consulting’s report intentionally prioritizes tools that teams can act on in 2026. Highlights include:

- Supply risk heatmap with tiered mitigation actions (supplier diversification, contract language, inventory policy).

- Go‑to‑market templates for food & beverage formulators and pharma CDMOs to accelerate product launches while managing compliance.

- Pricing elasticity and margin sensitivity models linked to raw material cost scenarios and FX exposure.

- Regulatory tracker with checklists for FDA, EFSA and EU REACH obligations—useful for product registration and cross‑border exports.

- M&A screening filters and valuation heuristics for buying capacity versus buying capability (e.g., purity, certifications, backward‑integration).

- Commercial negotiation playbooks tailored to both buyers and sellers, including sample contract clauses and KPIs for long‑term supply agreements.

Regulatory and supply‑chain dynamics to watch in 2026

Regulatory clarity in principal markets reduces headline legal risk, but operational compliance remains a differentiator. Key items covered in the report:

- Longstanding FDA regulation (21 CFR 180.37) and recent EFSA re‑evaluations provide a stable acceptance baseline for formulated food and pharmaceutical applications—however, label and claim policy remains market‑sensitive.

- Customs and chemical compliance (including HS code obligations and REACH requirements for EU trade) require integrated legal and logistics workflows to avoid delays and added cost on cross‑border shipments.

- China’s role as a supply hub: large production volumes, low raw‑material cost structures and capacity expansion plans materially influence global pricing and availability. Procurement teams must monitor capacity builds and export policy shifts to anticipate spot‑market swings.

Where the report stops — and why you should get the full study

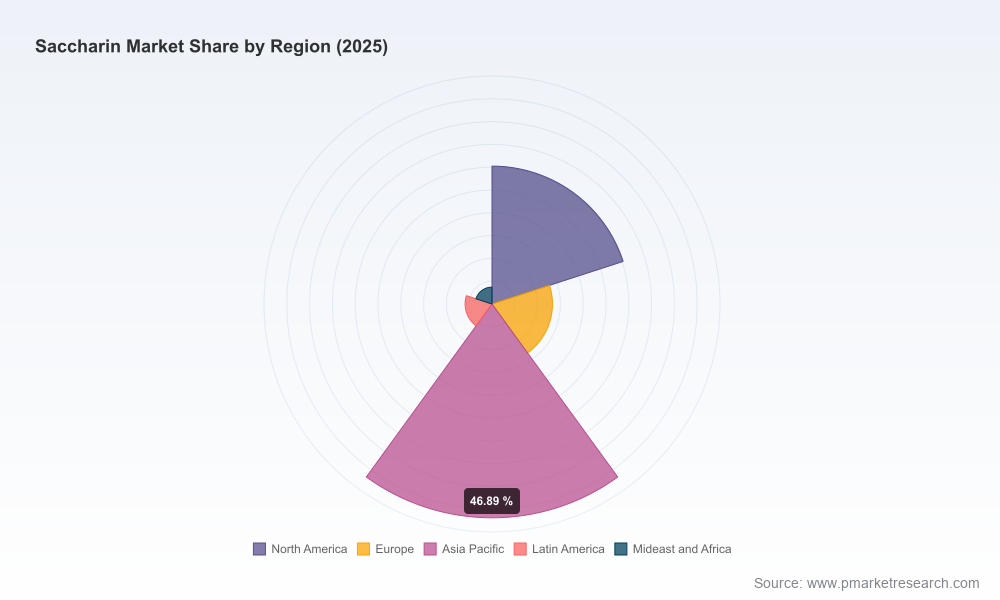

This introductory brief is designed as a strategic “trailer”: it surfaces the key market trajectory, the strategic implications for 2026, and the operational levers that drive value. To preserve the commercial sensitivity of tactical segmentation — regional and application splits, fine‑grained price curves, contract comparators and full company financials — those core data tables and proprietary models are available only in the full report.

If your team needs executable guidance (detailed supplier scorecards, SKU‑level margin impact analysis, curated M&A target shortlist, or a 12‑month tactical procurement plan built from the dataset), the full PW Consulting Saccharin Market report contains the necessary quantitative detail and templates to move from strategy to execution.

Action checklist for corporate leaders in 2026

- Procurement: commence dual‑track supplier qualification now (shortlist low‑cost producers and high‑quality pharmaceutical‑grade suppliers) and test small bilateral agreements to validate logistics and quality.

- Commercial/R&D: pilot value‑added formulations leveraging high‑purity grades to differentiate in food and pharma segments—use the report’s claimability matrix when constructing labels.

- Finance/M&A: run valuation scenarios using our market growth path and price sensitivity models to decide between greenfield capacity, bolt‑on acquisitions, or long‑term tolling agreements.

- Regulatory/Legal: align cross‑functional teams on REACH/HS compliance and maintain a regulatory watchlist for regional variations in labeling or additive limits.

PW Consulting’s Saccharin Market study equips decision‑makers with the macro view and the operational tools needed to act confidently in 2026. For the complete dataset, including full regional and application splits, company financials, and downloadable contract templates, access the full report on our site or contact our advisory team to schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Saccharin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com