What Is Driving the Carbon Neutral Oil and Fuel Market Toward USD 78.9B by 2034 at 9.5% CAGR?

Other |

2026-06-22 12:47:44

As OEMs, tier suppliers and chemical manufacturers prepare budgets and roadmaps for 2026, the automotive grease market presents a paradox: steady, predictable top-line expansion alongside accelerating technical and regulatory disruption. PW Consulting’s latest market study — anchored on a 2025 base year and a 2026–2032 forecast window — quantifies that the global market has grown from roughly USD 46.5 million in 2020 to USD 58.2 million in 2025 and is projected to reach approximately USD 79.2 million by 2032 at a compound annual growth rate (CAGR) of 4.5%. Those headline figures mask a dynamic landscape where product chemistry, OEM approval pipelines, supply-chain tightness and regulation together dictate winner and loser scenarios for 2026 decisions.

Automotive Grease Market

Actionable timing: 2026 is the inflection year for multiple external shocks — tighter Group III base-oil availability, revised SAE classifications and escalating restrictions on PFAS and certain lithium compounds. Businesses that align product roadmaps and procurement strategies now will avoid margin erosion and lost OEM access later in the year.

Automotive Grease Market

Innovation vs. compliance trade-offs: Reformulation choices driven by regulatory thresholds (for example, new reproductive-toxicity-related limits on lithium hydroxide) are not merely technical; they change supply-chains, test cycles and time-to-approval. Our analysis converts those trade-offs into prioritised R&D and commercial paths.

Automotive Grease Market

Portfolio optimization: With the automotive greases market growing at a mid-single-digit CAGR, incremental growth alone won’t sustain total-return expectations. Success requires targeting high-value use cases (e.g., actuator and EV steering systems) and securing OEM approvals — the differentiator between commoditised volume and premium value capture.

Regulatory-driven reformulation: International and automotive-specific lists (including updates to GADSL and SAE J2695) plus new substance thresholds have pushed leading formulators to accelerate PFAS-free and lithium-reduced solutions. The practical implication for 2026: companies must choose between accelerated reformulation investments (and certification timelines) or targeted product-line pruning.

Raw material pressure: The 2026 tightening of Group III base oil supply created immediate price and availability stress. Procurement teams must move from spot buying to multi-year fixed contracts, diversify across base oil groups and evaluate synthetic alternatives. Our scenario models show the sensitivity of gross margins to a 10–25% base-oil premium over crystallised contract cycles.

Functionality shifts from ICE to EV: Electric powertrains concentrate different lubrication needs — actuators, high-speed low-torque bearings and sealed-for-life units require low-PFAS, thermally-stable chemistries and packaging formats compatible with electrified vehicle assembly lines. OEM approval cycles now weigh life-cycle emissions and recyclability of lubricant packaging alongside classical performance metrics.

Consolidation and concentration: The market exhibits meaningful concentration among global majors and OEM-preferred suppliers. This creates both barriers (OEM access) and opportunities (targeted carve-outs and bolt-on acquisitions for specialist formulators or regional distributors).

The competitive map is best read as three archetypes: global integrated majors, specialty formulators and regional/multi-local suppliers. Integrated majors (examples include global oil & gas and lubricant platform leaders) leverage broad OEM libraries of approvals and global logistics networks to defend premium automotive accounts. Specialty players and technology houses concentrate on niche performance chemistries — e.g., high-temperature synthetic greases or PFAS-free complexes — and are attractive partners for co-development programs. Regional producers provide agility, price-competitive supply and local OEM relationships that are often decisive for mid-tier vehicle programs.

Global majors: Firms with deep OEM approval libraries are defending by expanding low-risk reformulation corridors and investing in supplier traceability to meet evolving substance lists.

Specialty innovators: Companies focusing on hybrid thickeners, PFAS-free and lithium-light chemistries are moving fastest to capture new EV actuator and steering-system specifications.

Regional challengers: Price discipline and nearshoring give regional producers runway in aftermarket and tier-2 supply — an area ripe for consolidation or strategic partnership for 2026 market share gains.

Recent product and approval developments illustrate these trends: leading formulators launched PFAS- and lithium-free calcium-complex greases and PFAS-free actuator lubricants in 2025; hybrid PU-CSC chemistries for CV joints emerged later in 2025; and new packaged ranges for wheel bearings and CV joints were introduced in mid‑2026. OEM approvals continue to be a decisive gate — successful 2025–26 product entries often followed targeted co-validation programs with vehicle manufacturers.

PW Consulting’s Automotive Grease Market study is deliberately operational. The deliverables most cited by our advisory clients are:

A calibrated market model with base-year reconciliation (2020–2025), 2026–2032 scenarios and sensitivity testing against base-oil price shocks and reformulation timelines.

Regulatory watchlist mapped to formulation levers and approval timelines — actionable so R&D and regulatory teams know which chemistries to prioritise for qualifying cycles in 2026.

Competitive tracker and OEM-approval matrix with supplier-to-OEM mappings and time-to-approval estimates (used to prioritise commercial investment).

Supply-chain heat maps and procurement playbooks that translate base-oil tightness and additive scarcity into contract, hedging and alternative-sourcing strategies.

Go-to-market playbooks for premium greases (EV actuators, sealed-for-life bearings), including pricing frameworks, packaging innovations and distributor engagement models.

M&A and partnership screening: target profiles, valuation heuristics and integration checklists for acquiring specialty formulators, regional distributors or additive technology assets.

Technical appendix: lab comparators, typical test protocols, and a reformulation toolkit for migrating from lithium-complex and PFAS-based thickeners to compliant alternatives.

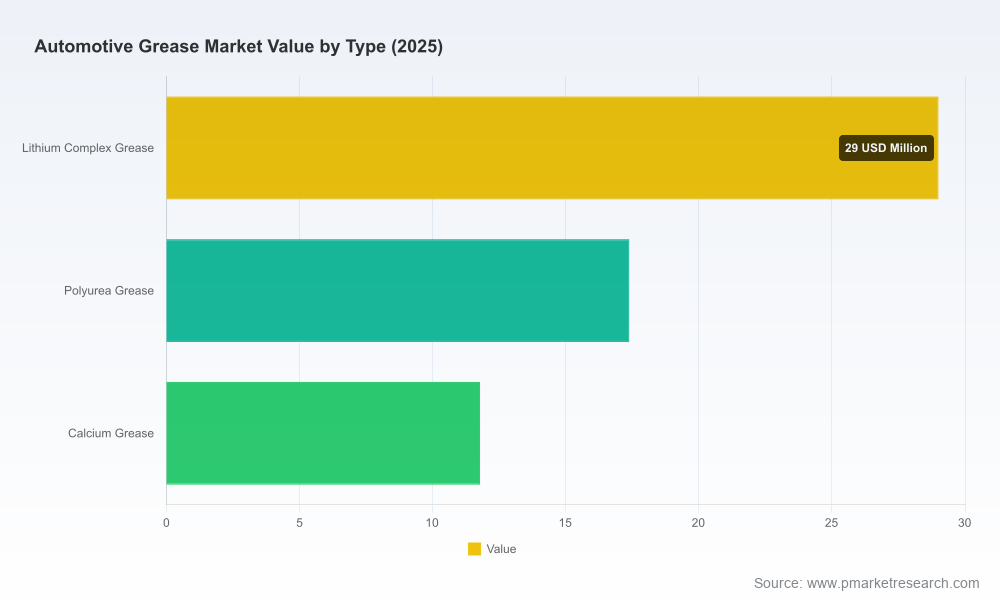

Note: to preserve the strategic value of this study for paying clients we present headline market sizing and trajectory here, while core subsegment breakouts (by region, specific grease type and application) are reserved for the full report and interactive dashboards.

Prioritise reformulation investments. For product leaders, accelerate PFAS-free and lithium-reduced chemistry dossiers for actuator and steering applications — a 6–12 month headstart reduces OEM cycle risk in 2026.

Lock supply contracts and diversify base-oil sources. Negotiate tiered take-or-pay contracts with Group II/III and synthetic suppliers; consider co-investing in toll-blending capacity where base-oil scarcity is acute.

Target OEM approvals selectively. Use our OEM-approval matrix to map highest-return programmes and allocate test-facility capacity accordingly; avoid broad, unfocused campaigns that burn cash and calendar.

Explore bolt-on M&A in specialty chemistries. Niche formulators with PFAS-free and hybrid-thickener IP are acquisition candidates that can de-risk your product pipeline within 12–18 months.

Introduce a sustainability premium tier. Clearly document PFAS-free status, lithium content and recyclability of packaging to capture OEMs’ increasing procurement premiums for documented compliance.

De-risk aftermarket channels. Strengthen distributor partnerships with stock-point guarantees and co-branded service offerings — aftermarket resilience is a powerful hedge against OEM cycle volatility.

The automotive grease market is a classic industrial market in transition: reliable aggregate growth (4.5% CAGR to 2032) but an evolving set of functional requirements and regulatory constraints that will re-order value pools. Firms that treat 2026 as a year for disciplined capital allocation — prioritising reformulation, securing upstream supply and selectively investing in OEM approvals or M&A — will convert the market’s predictable topline growth into durable competitive advantage.

PW Consulting’s full study gives procurement, R&D and corporate development teams the granular intelligence and executable playbooks necessary to turn 2026 uncertainty into strategic optionality. For the complete subsegment breakouts, interactive models and supplier maps referenced above, please consult the full report and dashboards on our website or contact our Automotive Lubricants practice for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Automotive Grease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com