EVSE Market 2026: Strategic Preview for Executive Decision‑Making

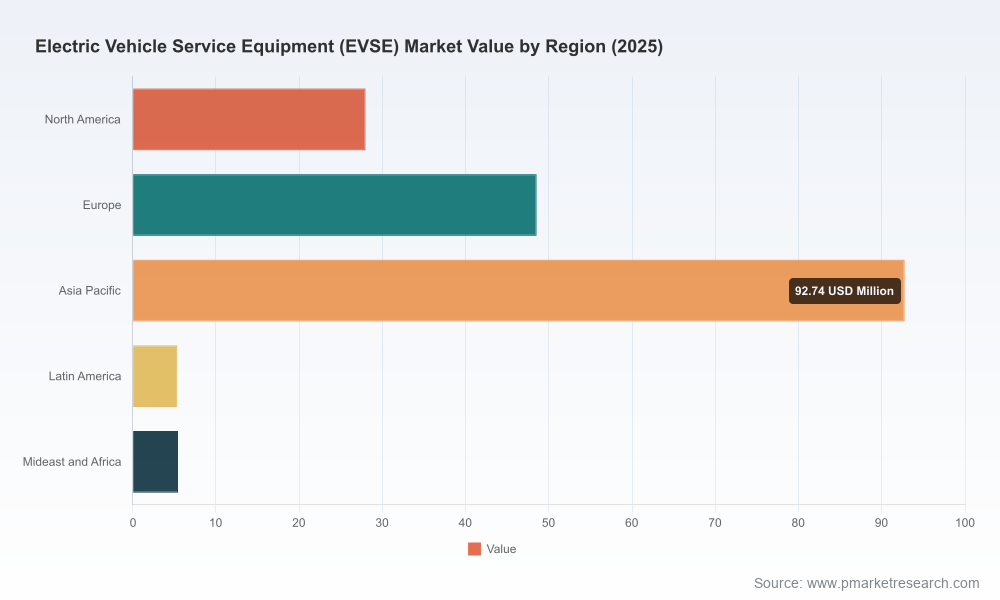

Electric Vehicle Service Equipment (EVSE) is no longer a niche capital expenditure — it is a strategic asset class that will shape fleets, utilities, urban planning and retail real estate for the next decade. Our PW Consulting market synthesis uses a 2025 base year and a 2020–2025 historical window to project the EVSE opportunity through 2032. The global market, measured in USD Million, expanded from roughly USD 80 Million in 2020 to USD 180 Million in 2025 and is forecast to continue at a compound annual growth rate (CAGR) of 29.1% through 2032, reaching an estimated USD 1,079 Million by the end of the forecast period. This trajectory — and the structural forces behind it — are the foundation for the 2026 strategic choices faced by manufacturers, operators, investors and public-sector planners.

Electric Vehicle Service Equipment (EVSE) Market

Why this report matters for 2026 decisions

- Time-to-scale urgency: At a near-30% CAGR, late market entry compounds competitive disadvantage. The analysis helps identify which segments and deployment models favor early movers versus fast followers.

- Risk-to-return clarity: With shifting regulation, rising labor costs for installation, and nascent business models around managed charging and V2G, the report quantifies downside scenarios and outlines mitigation levers.

- Procurement and partner playbooks: Tender design, specification language, and partner scorecards reduce execution risk for capital projects and public tenders.

- Capital allocation guidance: For corporate strategists and PE investors, the study maps which capability gaps (hardware scale, software stack, site operations) drive valuation premia.

What the research delivers (practical, action‑oriented components)

- Proven market-sizing methodology tied to vehicle adoption curves, policy incentives, and power availability — base year 2025, historical period 2020–2025, forecast 2026–2032.

- Scenario set (conservative, reference, accelerated) with shaded probability outcomes and sensitivity levers for energy prices, permitting lead times, and labor cost inflation.

- Competitive benchmarking and capability matrix for OEMs, system integrators and network operators — technology, product roadmap, go‑to‑market, and channel strength assessed.

- Deployment playbooks: residential rollout, commercial real‑estate programs, public fast‑charging corridors, and fleet hub strategies — each with implementation milestones, supplier selection criteria, and O&M cost outlines.

- Regulatory and standards heatmap linked to procurement checklists — includes Buy‑America considerations, metering and measurement rules, and applicable safety certifications.

- Investor appendix: capex/opex models, lifecycle TCO templates, and payback calculators prepped for board-level decisioning.

Market dynamics and near‑term catalysts

The EVSE market is maturing unevenly across technology layers. Hardware innovation (ultrafast DC charging, modular multi‑port platforms, bidirectional chargers) is converging with software stacks that enable load management, driver billing and uptime guarantees. Grid‑side constraints and the increasing value of managed charging are rapidly elevating power management as a decisive competitive moat.

Electric Vehicle Service Equipment (EVSE) Market

- Technology inflection points: 2024–2026 product introductions pushed capacity and modularity forward. Platforms enabling scalable deployments (multi‑point architecture and cloud orchestration) reduce per‑point costs and accelerate commercial rollouts.

- Policy and standards: 2026 saw meaningful regulatory activity that directly affects procurement and localization decisions. For example, a notice proposing adjustments to the Buy America waiver for EV chargers (FHWA, Feb 2026) raises the likelihood of supply‑chain localization requirements for publicly funded projects. Parallel activity in Europe — amendments to measurement directives introducing EVSE‑specific annexes — tightens metering and revenue‑grade requirements for public charging providers.

- Safety and interoperability: An emphasis on accredited safety standards (e.g., UL 2252 for adapters and chargers) and public guidance from industry bodies increases compliance costs for non‑certified offerings but also creates switching opportunities for certified incumbents.

- Demand push from fleets and public incentives: State and utility rebate programs and targeted funds for medium/heavy‑duty hubs are seeding concentrated demand. These programs address total cost of ownership challenges for fleet operators and, when aligned with deployment incentives, shift the economic case toward faster commercial adoption.

Competitive landscape — high‑level positioning and recent moves

The market remains moderately fragmented: the top three firms account for roughly one‑third of market share (CR3 ~33%), and the top five around 35% (CR5 ~35%), indicating room for consolidation but also substantial opportunity for differentiated players.

Electric Vehicle Service Equipment (EVSE) Market

- ChargePoint (California, US) — Strengths: broad product range from home to commercial and DC fast chargers, with a clear push into software services and driver management solutions. Recent launch: Flex Plus home charger with an integrated Driver Management Solution (July 2025) which signals an ambition to monetize employer‑based reimbursement and managed charging flows.

- Eaton (Dublin, Ireland) — Strengths: power electronics and systems integration for utilities and commercial customers. Strategic collaboration with ChargePoint on ultrafast DC V2G chargers (announced Aug 2025) highlights a combined hardware‑software approach for grid‑friendly, high‑duty deployments.

- Tritium Technologies (Irvine, US) — Strengths: focus on DC fast chargers and scalable platforms for commercial/fleet deployments, exemplified by the TRI‑FLEX platform (May 2025) that supports high density distributed deployments.

- ABB (Zurich, Switzerland) — Strengths: megawatt‑scale systems and proven deployments in high‑duty corridors. ABB’s portfolio positions it to capture utility and large‑fleet tenders that require hardened hardware and established service networks.

- Siemens (Munich, Germany) — Strengths: integrated metering, connectivity and industrial execution experience; suited to complex commercial and municipal rollouts that require end‑to‑end systems delivery.

- EVgo (United States) — Strengths: operator heritage in public fast charging and an aggressive connector strategy aligned with NACS expansion; well positioned for retail and highway charging footprints.

- EPRI (United States) — Role: not a commercial vendor but a critical standards and vetting authority through tools like the Vetted Product List, which materially influences utility procurement decisions.

These players illustrate two strategic archetypes that buyers must weigh: scale‑oriented system integrators that bundle power and services, and focused hardware innovators that compete on product economics and deployment velocity. Strategic partnerships (e.g., Eaton + ChargePoint) show the market favoring combined value propositions that address both grid integration and customer experience.

Strategic choices for 2026 — what leaders should prioritize

- Lock in standards compliance early. Certification (safety, metering, interoperability) is increasingly a gating factor for public and utility procurement. Non‑compliance risks delayed commissioning and higher retrofit costs.

- Design procurement for optionality. Include upgrade paths for software, modular power scaling, and tariff‑based load management. Avoid single‑vendor lock‑in on elements that will evolve quickly (e.g., protocol stacks, payment integrations).

- Hedge supply‑chain localization risk. With shifts in Buy America and similar rules elsewhere, buyers with public funding exposure should build alternative sourcing strategies or pre‑qualify local assembly options to preserve eligibility for incentives.

- Prioritize operational performance metrics. For operators, uptime and throughput per site drive revenue. Contract structures and SLAs should reflect expected utilization curves and include clear terms for maintenance and parts replacement.

- Invest in integrated energy management. The margin waterfall increasingly sits in power optimization and managed charging services rather than hardware alone. Bundled offers that reduce demand charges and enable V2G capture will win in commercial and fleet contexts.

- Use pilot projects to de‑risk scale. Structured pilots with explicit KPIs (installation time, mean time to repair, customer uptake) create playbooks that reduce execution risk when moving to rollouts.

How to use the full PW Consulting report

This article is a strategic preview. The full report contains the granular modeling and operational assets needed to act in 2026: disaggregated demand scenarios by deployment archetype, vendor scorecards with weighting methodologies, downloadable capex/opex templates, procurement RFP language, and a regulation‑by‑market heatmap. It also provides a short list of prioritized vendors for different buyer archetypes and a recommended 18‑month implementation timetable for public agencies and large corporate fleets. For teams preparing budgets or tender pipelines in 2026, these deliverables convert insight into actionable decisions.

EVSE is now a systems problem as much as a product problem. The winners will be those that integrate hardware economics, software intelligence, grid partnerships and disciplined execution. Our 2026 advisory focus is to reduce uncertainty at each decision point — from supplier selection to site design, regulatory compliance and financing — so leaders can convert high‑growth opportunity into durable, profitable scale.

For detailed analysis of this topic, please visit the official page:Electric Vehicle Service Equipment (EVSE) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com