Sternal Closure Systems Market: Insights, Key Players, and Growth Analysis

Networking |

2026-07-01 08:17:54

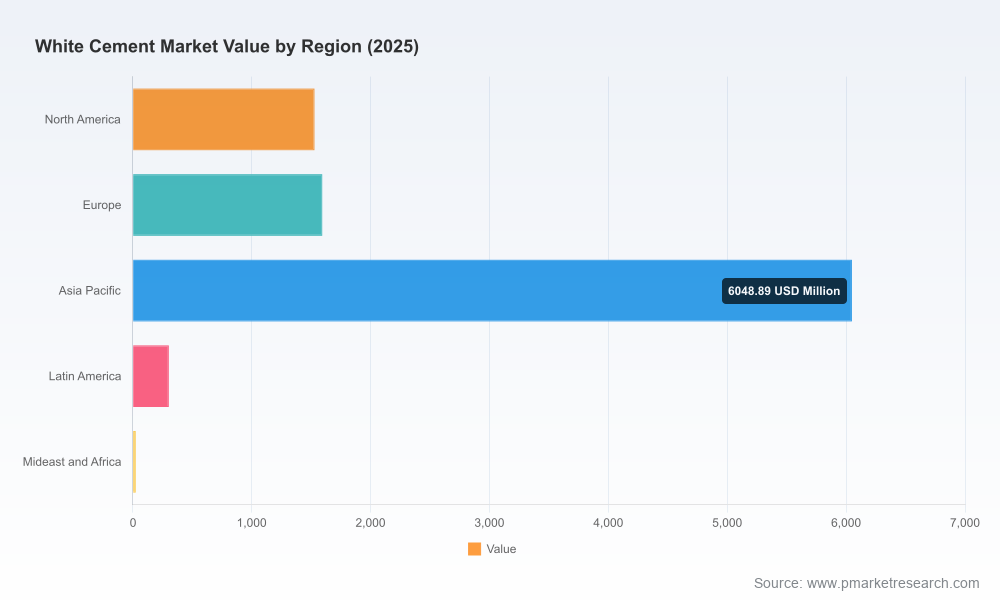

As the construction materials complex navigates post-pandemic normalization, white cement has re-emerged as a strategic niche with outsized implications for architectural finishes, premium building envelopes, and value-added downstream products such as wall putty and decorative mortars. Our PW Consulting baseline estimates place the global white cement market at approximately USD 9,500 Million in 2025; under our central scenario the market expands at a 4.55% CAGR over the 2026–2032 forecast window to reach roughly USD 12,930 Million by 2032. That trajectory reflects a steady mix of renovation-led demand in mature markets and accelerated specification-led uptake in high-growth regions.

White Cement Market

Timing: 2026 is a pivot year for decision-makers who must reconcile near-term capacity choices with medium-term sustainability and color-quality constraints. Investments approved now (grinding lines, kiln upgrades, security of low-iron feedstock) will materially shape cost curves and market access through 2030.

White Cement Market

Value capture: White cement is not a commodity-only play. Margin pools are concentrated where high-whiteness, low-defect supply, and integrated formulations (putty, primers, specialty mortars) meet specification-driven construction. Companies that align product development and channel strategies can capture premium pricing and higher lifetime customer value.

White Cement Market

Risk exposure: Raw-material concentration and color sensitivity create unique supply and operational risk. Procurement, logistics, and product engineering choices have outsized influence on both physical availability and brand reputation in premium architectural segments.

The market growth we model combines multiple, interacting drivers rather than a single demand vector. Key structural elements include urbanization and aesthetic-led specification in new commercial and high-end residential construction, renovation cycles in developed markets, and increased productization within the finishing segment (pre-blended putties, ready-mix decorative mortars, and factory-applied coatings). On the supply side, gradual capacity additions and targeted expansions—particularly in Asia and South Asia—are raising installed capability but not without constraints from feedstock availability and color-critical manufacturing limits.

Our historical series and forecasts show a clear recovery from the 2020–2024 period, with 2025 acting as a new baseline. That baseline supports a multi-year, mid-single-digit CAGR through 2032 under a central-case macro profile. Scenario analysis in the full study demonstrates sensitivity to three principal shocks: a major feedstock disruption, an accelerated shift to green building procurement, and rapid substitution by alternative aesthetic materials.

Feedstock scarcity and concentration: White cement requires ultra-low-iron limestone or TiO2-based color adjustments. High-quality deposits are geographically concentrated, and our field interviews confirm that procurement competition for these deposits—and the logistics to transport them—are primary sources of margin pressure.

Thermal and color constraints limit fuel flexibility: Unlike gray cement kilns that can pivot readily to alternative fuels and higher substitution rates of SCMs, white cement kilns face stricter color and temperature windows. That reduces options for decarbonization unless specialized, incremental investments are made in process control and colour-preserving fuel blends.

Regulatory and green-building drivers: Updated Environmental Product Declarations (EPDs) and green certification requirements are becoming a de-facto procurement filter for institutional clients. Producers that can validate lifecycle performance and low-carbon pathways will access specification-led projects and premium tenders.

The sector is moderately concentrated: our market concentration metrics indicate that the top three producers account for roughly a third of market value, and the top five approach mid-forties percentages. That market structure supports both regional champions and a set of highly specialized local players focused on architectural markets and export niches.

Illustrative corporate moves and commitments in the last 18–24 months underscore two strategic themes—vertical integration toward value-added products, and targeted sustainability investments. Examples we track include:

Strategic acquisitions and capacity scaling to integrate wall-putty and downstream formulations into a single go-to-market package—moves that shorten the route to specification and boost customer lock-in.

Certification and lifecycle transparency: producers releasing updated EPDs to meet green procurement specifications and to position premium white cements for sustainable construction projects.

Operational expansion in core producing regions through grinding lines and plant debottlenecking, improving local availability while lowering transport exposure for heavy low-iron feedstock.

Company-level positioning matters more than ever. Regional champions with integrated putty and wall-finishing portfolios are competing directly with international suppliers that rely on logistics scale and EPD-backed products. In this environment, three tactics tend to separate winners from the pack: breadth of formulation and product services, secure low-iron feedstock access, and credible sustainability credentials.

For executive teams and investment committees, the 2026 decision horizon should emphasize three pragmatic lines of action:

Secure upstream inputs through diversified sourcing and selective stake-building in low-iron limestone assets. Where direct ownership is infeasible, negotiate long-term offtakes with supply-linked price collars to mitigate raw-material volatility.

Invest selectively in color-stable process control and high-precision grinding to expand the usable feedstock envelope and enable higher substitution of alternative materials without compromising whiteness or performance.

Differentiate through product ecosystems: couple white cement to pre-blended putties, certified EPDs, and specification support for architects and contractors. This is a route to packaging premium margins and building durable specification pathways.

Feedstock availability curves and landed cost per tonne of low-iron limestone.

Color quality yield rates (e.g., batches meeting whiteness thresholds) and scrap/rollback ratios at the grinding and blending stages.

EPD and certification pipeline status across key sales markets—monitor changes in procurement policies among major contractors and institutional buyers.

M&A and capacity additions in core geographies—track announced projects and commissioning schedules, which can alter regional supply balances within 12–24 months.

Our full White Cement Market study is designed to be a decision-focused playbook, not just a descriptive review. Highlights include:

Scenario-based demand models and sensitivity matrices that link macro assumptions to regional and application outcomes (interactive dashboards included).

Plant- and asset-level mapping of capacity, with commissioning timelines and estimated utilization thresholds to inform capacity-allocation and greenfield vs. brownfield choices.

Supplier scorecards and benchmarking templates for procurement teams to evaluate feedstock contracts, logistics partners, and tolling arrangements.

Sustainability compliance playbook: steps to secure EPDs, roadmap to incremental decarbonization within color constraints, and buyer-facing documentation templates.

M&A and partnership playbooks — valuation ranges, integration risks, and typical synergies for bolt-on white cement assets and downstream wall-putty businesses.

White cement will remain a specialized but strategically critical sub-sector of the broader cement market. The path to higher returns is not purely volume-driven; it is built on specification control, upstream feedstock security, and the ability to translate product performance into ecosystem solutions for finishing and façade applications. For investors and corporate strategists, 2026 is the year to make choices that lock in color-quality advantages, EPD-driven market access, and downstream monetization—choices that will determine competitive positioning across the next market cycle.

Our public preview highlights the contours of these opportunities and risks. For the granular regional splits, segment-level forecasts, plant-by-plant capacity maps, and the full set of actionable toolkits that support procurement, M&A, and product-development decisions, please consult the complete PW Consulting White Cement Market report and its interactive annexes.

For detailed analysis of this topic, please visit the official page:White Cement Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com