Scaling Revenue Growth with Pipeline Intelligence

Other |

2026-06-11 17:59:09

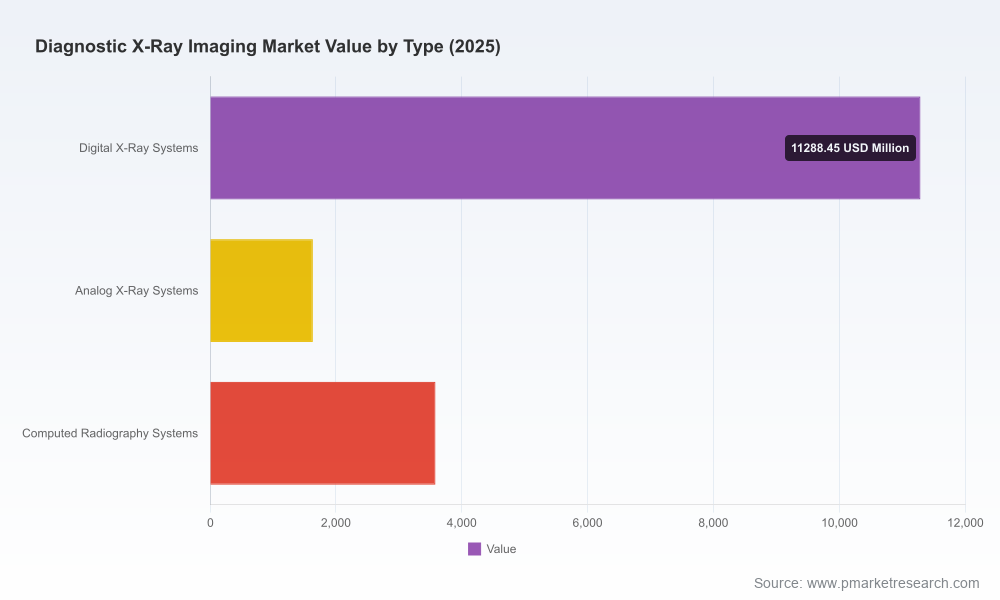

As healthcare systems, device OEMs, and capital investors set priorities for 2026, the diagnostic X‑ray imaging market presents a mix of steady growth, structural transformation and concentrated competition. PW Consulting’s Diagnostic X‑Ray Imaging Market study (base year 2025) synthesizes historical performance (2020–2025) and a detailed forecast (2026–2032) to frame practical choices for product roadmaps, commercial investment and M&A. The global market reached USD 16,500 Million in 2025 and, under a central case, is projected to expand at a 5.6% CAGR through 2032 — crossing the USD 24,000 Million threshold by the end of the forecast window. This briefing highlights how those macro trajectories translate into actionable priorities for 2026 while deliberately omitting granular sub‑segment numerical tables; the full report contains the detailed splits and models.

Diagnostic X-Ray Imaging Market

Timing and runway: 2026 is the pivotal year in which near‑term product launches, regulatory cycles and reimbursement updates will either accelerate adoption or introduce new barriers. The forecast horizon (2026–2032) gives decision‑makers a clear view of medium‑term payback windows for CAPEX and R&D.

Diagnostic X-Ray Imaging Market

Capital allocation: With the market growing at a mid‑single digit CAGR, distinguishing between stable, defensive investments (service, replacements, detector refresh) and higher‑growth adjacencies (AI, multi‑modal integration, portable/mobile fleets) is essential to optimize ROI.

Diagnostic X-Ray Imaging Market

Competitive posture: The market exhibits meaningful concentration among large incumbents alongside strategic component suppliers. Understanding where scale, vertical integration, or specialist differentiation matter will determine successful routes to market in 2026.

Validated market sizing and 7‑year forecasts (2026–2032) with scenario stress‑tests tied to reimbursement and regulatory inflection points.

Competitive landscape mapping, including vendor scorecards, product positioning matrices and go‑to‑market playbooks tailored for hospitals, imaging chains, outpatient clinics and dental/orthopedic specialties.

Technology and product deep dives: digital flat‑panel detectors, mobile X‑ray platforms, computed radiography legacy displacement curves, and the economics of detector replacement vs system refresh.

Regulatory and reimbursement impact analysis, including compliance pathways (assembler reporting and national/region‑specific controls) and payer dynamics that influence adoption cycles.

Supply chain and sourcing risk register, from X‑ray tube availability to detector glass and electronics, with mitigation playbooks (dual sourcing, strategic inventory, co‑development).

M&A and partnership frameworks: target prioritization, valuation sensitivities, integration checklists and examples of value creation through component control or software monetization.

Operational benchmarks and pricing guidance — not as raw list prices, but as actionable margins, service revenue opportunities and upgrade pathways mapped to buyer personas.

Technology substitution and refresh cycles: The shift toward digital radiography and improved detector performance continues to drive replacement demand and create opportunities for retrofit kits and detector leasing models.

AI and workflow automation: Incremental image post‑processing, AI‑assisted collimation and triage are moving from pilot to productization. Vendors that bundle clinical decision support with clear regulatory compliance pathways will win faster hospital trials and scaling agreements.

Regulatory tightening: Recent guidance around assembler reporting and equipment safety frameworks means procurement teams and manufacturers must allocate programmatic resources to compliance and traceability during installations.

Reimbursement sensitivity: Adoption is materially influenced by the reimbursement environment. Shifts in public payer coding or private contract pricing can compress or expand addressable volumes, especially in outpatient settings.

Component concentration and verticalization: Key components — tubes and flat panels — remain strategic inputs. OEMs pursuing in‑house production or long‑term supply contracts with independent suppliers are reshaping cost structures and aftermarket margins.

The competitive field is characterized by a small group of global system OEMs, specialist component suppliers, and nimble regional players. PW Consulting’s analysis profiles each major player and synthesizes their strategic posture for 2026:

GE HealthCare Technologies Inc. — A market leader for advanced digital radiography systems and mobile units. Strengths: broad installed base, integrated workflows, and a product pipeline oriented toward image quality and operational efficiency. For 2026, GE’s focus on modularized offerings and service network optimization will make it a preferred partner for large health systems.

Siemens Healthineers AG — Competitive in digital radiography platforms with a strong emphasis on clinical integrations and AI. Recent product introductions underline a strategy of combining hardware with software to lock in clinical workflows across hospital networks. Expect Siemens to push advanced functionality into mainstream products in 2026.

Koninklijke Philips N.V. — Positions its DR series around automation and workflow efficiency, leveraging AI‑assisted features. Philips’ strength lies in cross‑modality enterprise relationships that can bundle X‑ray with complementary solutions for enterprise deals.

Canon Medical Systems Corporation — Focused on image quality and specialized detector designs. Canon’s incremental innovations appeal to facilities prioritizing diagnostic fidelity; in 2026, targeted partnerships with imaging networks will be a growth lever.

Fujifilm Healthcare Solutions — Offers detector innovation and DR systems optimized for high throughput. Fujifilm’s strategy emphasizes detector technology as an entry point to drive system upgrades and service contracts.

Varex Imaging Corporation — As a leading independent supplier of X‑ray tubes and flat‑panel detectors, Varex sits at the center of OEM supply economics. Their position influences component pricing, availability and the feasibility of OEM verticalization strategies.

Carestream Health, Inc. — A specialist in mobile X‑ray and HD detectors with recent regulatory approvals that expand its addressable markets. Carestream’s agility in certification and targeted product innovation makes it a viable partner for European and North American imaging chains.

Recent company movements — product launches and regulatory approvals in 2025 — demonstrate acceleration in both innovation and market access. Notable examples include major OEMs introducing next‑generation DR platforms and specialist vendors achieving certification milestones that broaden market reach. These actions create near‑term opportunities for partnerships, pilots and procurement cycles in 2026.

Regulatory tightening scenario: Faster adoption of new assembler and safety reporting rules increases installation lead times and impacts time‑to‑revenue for new systems. Mitigation: standardize installation SOPs and allocate compliance specialists to large deals.

Supply shock scenario: Disruption to detector glass or tube production causes OEM lead‑time extensions. Mitigation: secure multi‑year supply contracts, invest in buffer inventory or evaluate detector refurbishment partnerships.

Reimbursement compression scenario: Payer rate pressure slows elective imaging volumes. Mitigation: pivot toward value‑based bundles, outcome‑linked service contracts and higher‑utilization settings (emergency, trauma).

Q1 — Portfolio triage: Use the PW Consulting decision matrix to rank product SKUs by margin resilience, replacement cycle and clinical stickiness. Decommission low‑yield SKUs and reallocate R&D to high‑impact detector and AI modules.

Q2 — Secure upstream inputs: Negotiate strategic supply agreements for detectors and tubes or evaluate minority investments in component suppliers to lock pricing and capacity.

Q3 — Commercial pilots: Launch joint pilots with key health systems integrating AI workflow features and service‑bundle economics; use pilot metrics to build the case for scaled rollouts in 2027.

Q4 — Market expansion & M&A screening: Target tuck‑ins that fill distribution gaps (e.g., mobile X‑ray specialists) or software assets that enable recurring revenue via subscriptions and analytics.

How exposed is our product roadmap to component shortages and regulatory delays in 2026?

Which clinical workflows will be defined by AI in the next 12–18 months, and can we be first‑mover in those pockets?

Do our commercial contracts capture service and upgrade economics that will offset hardware commoditization?

Are there strategic suppliers or regional partners whose control would materially change our margin and delivery profile?

This briefing is designed to orient executive priorities for 2026 and to highlight the kinds of strategic choices supported by our full Diagnostic X‑Ray Imaging Market study. The comprehensive report contains the granular regional and application splits, vendor share tables, detailed financial models (in USD Million), and a prioritized opportunity map that supports transaction diligence and operating plans. For full access to the sub‑segment data, scenario spreadsheets and vendor scorecards, please consult the PW Consulting source page and the complete study.

Pushing beyond the high‑level trajectory (USD 16,500 Million in 2025 to an estimated USD 24,029 Million by 2032 at a 5.6% CAGR) requires translating market growth into operational and strategic moves: secure supplies, accelerate software monetization, and align product innovation with payer and regulatory realities. Those who do will convert steady market growth into sustainable share gains in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Diagnostic X-Ray Imaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com