Кованые диски в широком каталоге от известного изготовителя

Other |

2026-03-27 14:53:25

As executive teams and investors prepare their 2026 agendas, the aesthetic lasers and energy devices market presents a classic strategic inflection: accelerating technological innovation, shifting payer and regulatory signals, and structural consolidation are converging to reshape commercial opportunity. Our upcoming PW Consulting report — with a base year of 2025 and a forecast window covering 2026–2032 — synthesizes five years of historical performance (2020–2025) and projects the market forward at a compound annual growth rate (CAGR) of 7.88%. This preview highlights the report’s practical value for decision-makers while preserving the detailed segmentation and proprietary figures that underpin our models; access to the full deliverable is required for the granular data that drive transaction-level decisions.

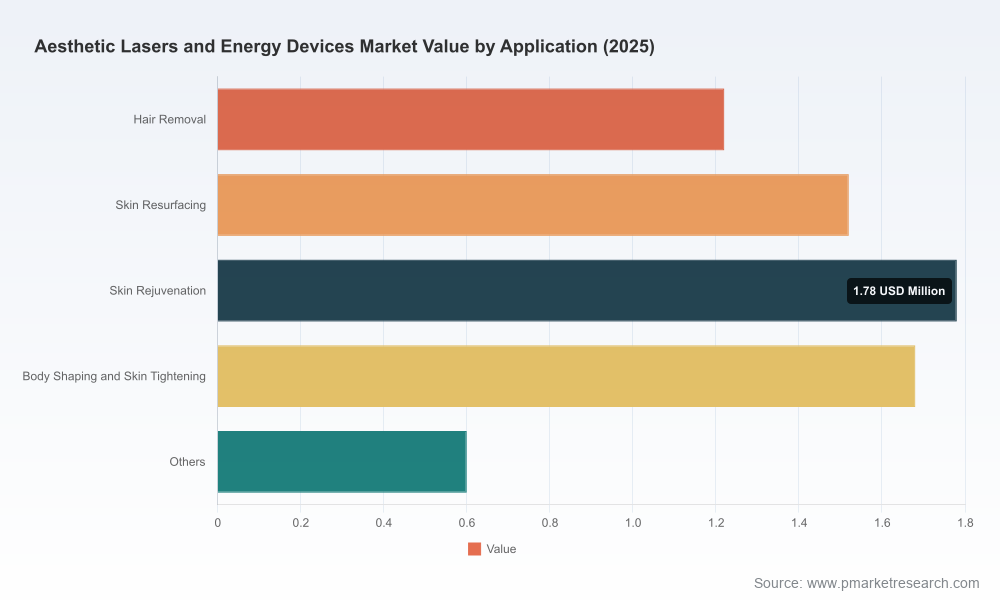

Aesthetic Lasers and Energy Devices Market

Two dynamics make 2026 uniquely consequential. First, the market completed a cyclical correction through 2025 and is positioned to resume durable growth across the forecast period; our modelling shows a clear recovery trajectory underpinned by renewed capital spending in clinics and medspas and by refreshed product launches. Second, a wave of regulatory clearances and certifications over 2024–2026 has lowered technical and market-entry barriers for certain technologies, changing the calculus for partnership, distribution, and competitive positioning. For strategy teams, this combination means 2026 is the year to move from “watch” to “win”: deciding whether to double down on organic R&D, accelerate inorganic consolidation, or refine a channel-first commercial model will determine competitive standing through 2032.

Aesthetic Lasers and Energy Devices Market

Growth posture: With the report’s 2026–2032 CAGR at 7.88%, the market is expected to generate consistent, above-market returns for companies that can capture share through differentiated technology, strong clinical evidence, and efficient sales channels. This pace supports mid-sized M&A where scale unlocks disproportionate margin upside via supply-chain and service-infrastructure leverage.

Aesthetic Lasers and Energy Devices Market

Volatility to opportunity: The historical window shows variability as clinics reset capital allocation and reimbursement dynamics evolved. That volatility compresses risk-adjusted valuations for some assets, creating attractive acquisition targets for strategic buyers and private-equity sponsors in 2026.

Market concentration: The market exhibits moderate concentration, with the top three firms accounting for a meaningful minority share and the top five increasing that proportion. For incumbents this means defensive product roadmaps and after-sales platforms (service, consumables, training) will be the primary levers for margin protection; for challengers it frames the opportunity for targeted disruption in narrow clinical use-cases or price-sensitive channels.

Regulatory and payer shifts are not only compliance items — they are demand multipliers. Recent regulatory milestones illustrate how clearance and reimbursement clarity can unlock new indications and expand the eligible patient pool. Notable signals include device CE approvals under updated MDR frameworks and multiple 510(k) clearances that justify expanded surgical and dermatological use. Parallel to device approvals, payer policies — for example, the recognition of fractional ablative fenestration procedures as medically necessary under specific functional-impairment criteria — create pathways for outpatient and hospital adoption beyond purely cosmetic queues.

For commercial leaders, this means a dual investment thesis: invest in evidence-generation (prospective registries, payer dossiers) to convert procedural reimbursement into recurring demand, while aligning regulatory strategy with product life-cycle planning to avoid commercial disruptions from evolving standards.

The competitive topology combines global incumbents with regionally strong specialists. Several firms have reinforced their positions through product innovation, distribution partnerships, and regulatory wins:

Established platform leaders have extended multi-modality roadmaps (laser + IPL + RF + microneedling) to maintain breadth across clinic use-cases, leaning on installed-base service and consumables to monetise lifetime value.

Recent product introductions and regulatory milestones (spanning late 2024 through early 2026) — including next-generation fractional CO2 systems, non-ablative fractional platforms receiving CE approvals, and multiple 510(k) clearances for platforms used in plastic surgery and dermatology — are reshaping competitive parity. These moves lower the barrier for clinic adoption of higher-value resurfacing and surgical-adjacent procedures.

Distribution strategy is a differentiator. Multi-country distribution agreements executed in recent cycles show how vendors are prioritizing access over direct investment in certain geographies, enabling rapid scale without heavy fixed-cost footprints.

Our full report profiles the incumbent and challenger sets in operational terms — go-to-market models, installed-base economics, consumables and service revenue shares, clinical evidence pipelines, and M&A readiness scores — to support tactical decisions such as category entry, bolt-on acquisition sizing, or divestiture timing.

This study is structured for immediate use by senior leaders and corporate development teams. Key deliverables include:

Market-sizing and scenario forecasts for 2026–2032, with base and stress scenarios that isolate technology substitution and reimbursement shocks.

Segment-level demand drivers by product architecture, technology families, clinical application clusters, and end-user channels — modelled to inform portfolio prioritisation.

Commercial playbooks: pricing, reimbursement pathways, training and adoption levers, and channel economics tailored to the medspa, dermatology clinic, ambulatory surgery center, and hospital segments.

Competitive due diligence packs: detailed company profiles, capability matrices, recent strategic moves, valuations yardsticks, and synergy estimates for M&A scenarios.

Regulatory and payer intelligence: timelines, policy impacts, and an evidence-generation roadmap aligned to high-return indications.

Risk matrix and mitigation guide: technology, regulatory, supply-chain, and market-adoption risks with prioritized action lists.

Crucially, the full dataset and appendices contain the granular region- and application-level splits, price-point elasticity tables, and the underlying forecast workbooks that power our recommendations. This preview omits those line-item details to preserve the strategic advantage that comes with the full subscription.

Companies that use 2026 to reconfigure their competitive stance should evaluate three core options, each demanding a different operational playbook:

Scale-through-consolidation: For businesses with product portfolios that overlap top-tier incumbents, targeted M&A to capture service networks and consumable streams is the fastest path to margin expansion. Integration plays should prioritise cross-selling to installed bases and harmonising service logistics.

Specialty depth: For technology-focused firms, double down on a narrow set of clinical indications where clinical differentiation and reimbursement lift allow premium pricing. Invest in randomized trials and payer dossiers to turn clinical evidence into market access.

Channel expansion with asset-light models: For companies seeking rapid geographic reach, distribution partnerships and hybrid direct-channel models reduce upfront costs and accelerate revenue while preserving capital for R&D and evidence generation.

Treat this preview as a strategic checklist and an operational thermometer. Use it to:

Validate whether current 2026 budgets align with a market growing at roughly an 8% CAGR over the forecast horizon.

Prioritise regulatory and evidence milestones — clearances and payer recognition visible today materially change total addressable opportunity.

Run a rapid portfolio triage using our outlined options to determine whether to invest organically, partner, or pursue M&A in 2026.

The aesthetic lasers and energy devices market is moving from a phase of platform competition to one of clinical and commercial leverage. Technology cycles, regulatory approvals, and payer determinations that have unfolded through 2024–2026 create differentiated pathways to growth for incumbents and newcomers alike. PW Consulting’s full report equips leaders with the quantitative scenarios, competitive dossiers, and execution playbooks needed to make confident 2026 decisions — whether that is to acquire, to scale, or to specialize.

To access the full analytical models, region- and application-level forecasts, and the detailed company profiles that underpin these strategic recommendations, please consult our full market study on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Aesthetic Lasers and Energy Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com