Oxaliplatin Market — 2026 Strategic Preview

Executive summary

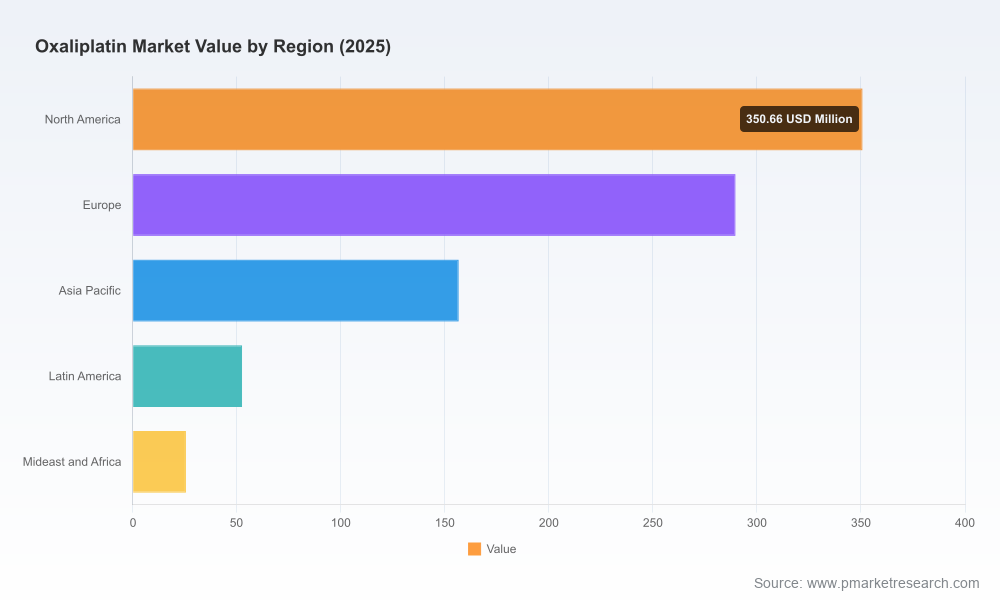

PW Consulting’s Oxaliplatin Market strategic brief synthesizes the evidence you need to make high-consequence decisions in 2026. The injectable oxaliplatin franchise has moved from a niche generics profile into a structurally growing oncology component: after rising from an estimated market base in 2020, the global oxaliplatin market reached an estimated USD 875.0 Million (base year 2025). Our forecast model projects a sustained compound annual growth rate (CAGR) of 9.6% through 2032, with the market trajectory accelerating into the second half of the decade as new clinical and commercial dynamics—ranging from regulatory designations to supply reshuffling—reconfigure access and pricing.

Oxaliplatin Market

This preview highlights the strategic implications of those dynamics without reproducing the granular subsegment figures contained in the full PW report. Think of this as the trailer: authoritative, directional and purposefully selective. The full intelligence package contains the underlying spreadsheets, SKU-level analyses, and regional split matrices that are essential for transaction due diligence, procurement strategy and launch planning.

Oxaliplatin Market

Market trajectory and scenario framing (2026–2032)

Oxaliplatin’s market evolution between 2020 and 2025 shows a clear recovery and growth inflection, driven by stable uptake in adjuvant colorectal regimens, incremental adoption in metastatic combinations, and the gradual expansion of generic supply channels. Our baseline forecast for 2026 estimates the market exceeding USD 950 Million and scopes further growth to a multi-hundred-million-dollar opportunity by 2032 under base-case assumptions.

Oxaliplatin Market

- Base case: Continued adoption in approved indications and gradual generic competitive entry, producing steady revenue growth consistent with the 9.6% CAGR embedded in the model.

- Upside case: Clinical or regulatory expansions (including new delivery/device combinations or label extensions) and resolution of current shortages could materially accelerate uptake.

- Downside case: Prolonged supply-chain constraints or a disruptive therapeutic substitution in first-line colorectal care would compress growth and shift value toward alternative pathways (e.g., oral cytotoxics or targeted agents).

Importantly, this forecast integrates supply-side shocks observed through 2026—most notably manufacturer discontinuations and current shortage listings—into stress-tested scenarios so decision-makers can calibrate inventory, contracting and M&A timelines to realistic risk horizons.

Why the 2026 decision window matters

Boardrooms and health systems will face pivotal decisions in 2026 that hinge on three interlocking timelines:

- Short-term procurement and patient-safety obligations driven by active shortage listings and manufacturer discontinuations.

- Mid-term commercial positioning to capture share as supply stabilizes or reconfigures.

- Long-term corporate strategy: portfolio diversification, capacity investments, or M&A to secure control over production and margin.

For market entrants, incumbent generics manufacturers, and private equity sponsors, 2026 is the year to convert operational responses into durable competitive advantage. Our modelling shows that firms which adapt contracting strategies, secure secondary manufacturing capacity, and align pricing to evolving reimbursement pressures will disproportionately capture upside across the forecast window.

Competitive landscape — what matters to strategists

The oxaliplatin landscape is dominated by a small set of established generic and oncology-injectable specialists. PW’s competitive assessment synthesizes public filings, regulatory approvals and commercial-supply profiles to produce actionable competitor maps.

- Teva Pharmaceutical Industries Ltd. (Petah Tikva, Israel) — a manufacturing and commercial presence in key markets via third-party production partnerships; active US supplier dynamics make it a player to watch for tactical supply agreements.

- Fresenius Kabi USA, LLC (Lake Zurich, Illinois, USA) — leverages an oncology injectables portfolio and multiple regulatory pathways to sustain market access; strategic for institutional contracts.

- Dr. Reddy’s Laboratories Ltd. (Hyderabad, India) — an established FDA-approved generic supplier with commercial reach in oncology channels.

- Sun Pharmaceutical Industries Ltd. (Mumbai, India) — strong in emerging markets; an important channel partner for geographic expansion and cost-competitive supply.

- Accord Healthcare Ltd. (Colchester, UK) — a European-focused generics provider with multiple brand entries and distribution relationships.

- Sandoz Inc. (Princeton, New Jersey, USA) — historically an established supplier; a recent discontinuation notice (effective 2026) and related shortage signalling introduces near-term supply disruption and short-term commercial opportunity for other suppliers.

Market concentration is meaningful: a handful of players account for the majority of commercially available supply. That concentration amplifies both supply risk—when one producer exits certain presentations—and opportunity for strategic entrants able to scale manufacturing quickly.

Recent regulatory and supply dynamics that will shape 2026 actions

- Manufacturer exits and active shortage listings: Industry sources and the American Society of Health-System Pharmacists (ASHP) list oxaliplatin among drugs with ongoing shortage status through mid-2026. Institutions should plan multi-supplier sourcing and validated alternate-dose protocols now.

- Orphan drug and device combinations: In May 2026, the FDA granted Orphan Drug Designation for oxaliplatin delivered via a localized device for pancreatic cancer—this creates a new pathway for indication expansion and device-driven premiumization of an otherwise commoditized molecule.

- Clinical and regulatory guardrails: Prescribing information continues to list clear contraindications (for example, hypersensitivity to platinum agents). Payers and providers will demand clear risk-management protocols tied to supply shifts.

- Reimbursement pressures: Regional HTA and reimbursement frameworks are increasingly prescriptive; in Europe, for example, a high proportion of adjuvant colorectal cases already receive oxaliplatin-based regimens. These utilization realities will constrain price elasticity in core markets while opening negotiation channels in emerging geographies.

Practical, transaction-ready deliverables in the full PW report

PW Consulting’s full Oxaliplatin Market report is built to be operational from day one. The deliverables include:

- Financial-grade demand model (historical 2020–2025; forecast 2026–2032) with configurable scenarios and sensitivity engines.

- SKU- and channel-level commercial maps, including hospital procurement flows and wholesaler concentration analyses.

- Competitive playbooks for incumbents and new entrants—pricing strategies, contracting templates, and go-to-market sequencing by market access complexity.

- Supply-chain risk heatmap that integrates API sourcing, secondary manufacturing capacity, and regulatory approval timelines to quantify outage probability.

- M&A and JV target shortlists scored against manufacturing lead time, regulatory filings, and commercial reach; Excel-based valuation overlays provided for rapid DD.

- Regulatory watch: timelines for anticipated device/indication filings, orphan designations and label-change scenarios with likely commercial outcomes.

To preserve the strategic value of the report as a decision-making asset, this preview does not reproduce the detailed regional splits, application-by-application revenue waterfalls, or SKU-level price grids—these are included in the full deliverable and the accompanying Excel models.

Actions we recommend for C-suite and commercial leaders in 2026

- Immediate: Implement multi-supplier short-term contracts and establish clinical contingency protocols to manage active shortage risks.

- Near-term (3–9 months): Run a rapid capacity assessment to determine whether in-house scale-up or contract-manufacturer partnerships will yield faster, lower-risk supply restoration than open-market sourcing.

- Strategic (9–24 months): Evaluate M&A or minority investments in targeted manufacturers to secure margin and continuity; prioritize assets that reduce lead times for sterile injectables.

- Commercial: Reassess pricing and tender strategies under scenario stress tests—focus on preserving institutional relationships where volume is concentrated and exploring premium opportunities tied to device-enabled delivery or novel indications.

How to use this preview

This document is intended as a strategic primer to orient leadership and investment committees. If you are preparing procurement contracts, evaluating acquisition targets, or designing a commercial playbook for oxaliplatin, the granular modeling and competitor intelligence in PW Consulting’s full report are required to operationalize these recommendations.

PW Consulting can provide bespoke briefings, access to the underlying Excel models, and an accelerated due-diligence package tailored to a specific transaction or procurement cycle. Contact our Oxaliplatin Market team to schedule a demonstration and obtain the full dataset and actionable annexes.

For detailed analysis of this topic, please visit the official page:Oxaliplatin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com