Cocoa Butter Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-11 10:17:43

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a condensed strategic briefing drawn from our comprehensive Atorvastatin Calcium Market study (base year 2025). This preview distills the analysis that will directly inform corporate strategy in 2026 — from commercial prioritization to sourcing, regulatory resilience, and M&A screening — while intentionally leaving proprietary segment-level breakouts to the full report.

Atorvastatin Calcium Market

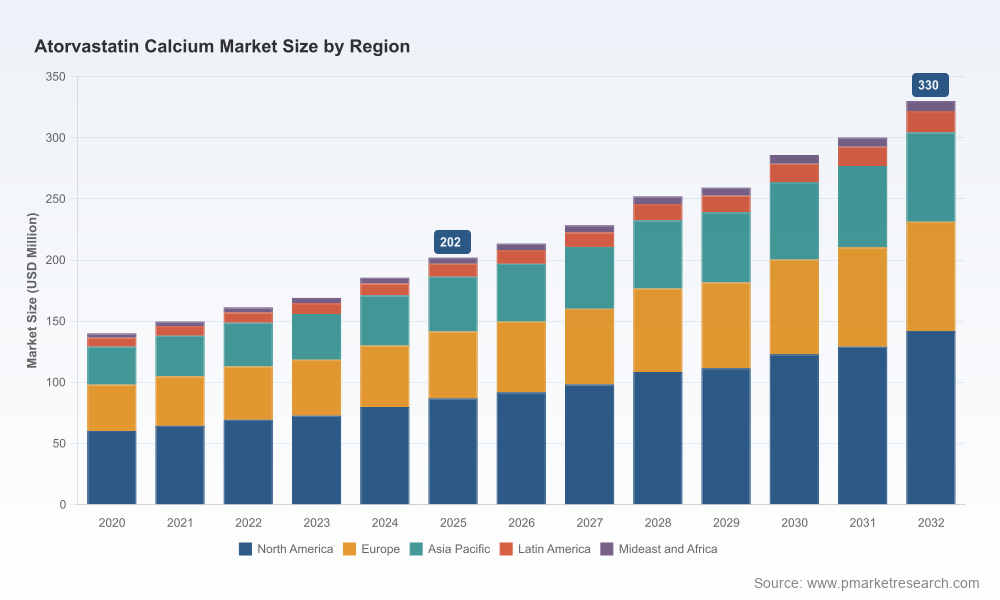

The atorvastatin calcium market has demonstrated steady expansion through the early 2020s, rising from approximately USD 140.0 Million in 2020 to USD 202.0 Million in 2025 (base year). Our forecast model projects continued growth through the 2026–2032 horizon, with the market expected to expand at a compound annual growth rate (CAGR) of 7.2% and reach roughly USD 330.0 Million by 2032. All monetary values in this briefing are shown in USD Million and reflect the aggregated market for atorvastatin calcium formulations and related API activity as defined in the study.

Atorvastatin Calcium Market

Actionable foresight for revenue planning — The combination of steady end-market growth and the structural dynamics of generic pharmaceutical supply means that near-term commercial decisions (formulation mix, contractual strategies, portfolio prioritization) will materially influence 2026 P&L outcomes.

Atorvastatin Calcium Market

Risk-adjusted sourcing and manufacturing — The production model for atorvastatin calcium remains vertically split: APIs are heavily sourced from established Indian suppliers while final formulation and distribution concentrate in other geographies. This creates both cost advantages and systemic concentration risks that must be balanced through supplier diversification and inventory strategy.

Regulatory and quality vigilance is non-negotiable — Recent quality events and recalls demonstrate how quickly market access and margins can be impacted. Companies must pair growth initiatives with robust quality and recall-response playbooks to avoid value erosion from supply interruptions.

Payer dynamics matter — Generic atorvastatin benefits from broad reimbursement frameworks (including U.S. Medicare Part D and state Medicaid programs). Optimizing route-to-payer access and contracting will be a key lever to capture volume growth without surrendering margin.

Competitive positioning — Market concentration metrics indicate a market where a handful of incumbents drive a majority of supply. This produces predictable competitive behaviors (price competition, bid-based contracting and opportunistic capacity expansion) that firms must model into their 2026 scenarios.

Integrated market model (2020–2032) with scenario toggles — base, upside and disruption scenarios (supply shock, regulatory action, accelerated generic uptake).

Segment-level analyses by region, formulation type and end-application — provided as interactive tables and downloadable financial models (note: detailed segment figures are reserved for the full report).

Supply-chain heatmap and supplier risk scoring — API source concentration, dual-sourcing opportunities, and cost-to-serve matrices for alternate suppliers.

Quality & regulatory playbook — escalation protocols, recall preparedness, and CAPA prioritization tied to potential revenue at risk.

Commercial playbooks — tendering templates, payer negotiation heuristics for Medicare Part D and Medicaid channels, and pricing recommendation bands aligned with margin objectives.

M&A and partnership screening toolkit — valuation sensitivities, integration risks and a prioritized target shortlist based on strategic fit and synergies.

Go-to-market impact analysis for manufacturing investments — ROI, payback timelines and scenario-based utilization forecasts for capacity expansion.

The competitive field for atorvastatin calcium mixes originator legacy players and global generic manufacturers, with specialization across API supply, formulation manufacturing and distribution. Key strategic positions are summarized below.

Originator presence: The originator continues to anchor brand awareness and pricing references in certain markets. Brand heritage affects contract benchmarks and clinician/payer perceptions despite generic prevalence.

Global generics and API suppliers: Large, vertically integrated generics firms control meaningful manufacturing and distribution scale. Select Indian API manufacturers are particularly influential in the upstream supply chain, serving as both internal suppliers and third-party vendors.

Distribution and contract-focused players: Certain regional distributors and specialty marketers play a pivotal role in channel execution, frequently procuring from overseas manufacturers to meet local demand.

Representative company roles captured in our study include originator commercialization, large-scale generic manufacturing, API supply specialization and distribution/marketing intermediaries. The full report profiles each material competitor with HQ, operational footprint, ANDA status, API capabilities and strategic posture to help prioritize partnerships or targets for acquisition.

Quality event: In September 2025, a voluntary nationwide recall was initiated for multiple lots of atorvastatin calcium tablets due to failed dissolution specifications (approximately 142,000 bottles). The recall underscores the speed at which localized quality control issues can ripple into supply volatility, contractual penalties and reputational loss.

Regulatory approvals: New ANDA approvals in late 2025 expanded the pool of approved manufacturers, altering competitive capacity and pricing dynamics in the U.S. market.

Supply chain reality: API supply remains concentrated among established Indian manufacturers; this structural characteristic creates both cost competitiveness and single-source risk for many buyers.

Reimbursement framework: Generic atorvastatin continues to benefit from established U.S. payer channels, including Medicare Part D and state Medicaid programs — a stable demand anchor for contract negotiation.

Quantitatively, the market exhibits a concentrated structure where the top three and five suppliers command a significant share of supply and commercial influence. For decision-makers, this concentration translates into:

High likelihood of disciplined price competition among top suppliers — expect periodic price compression tied to capacity expansions or tender cycles.

Opportunities for differentiated positioning — quality, supply assurance, and integrated API capabilities can be monetized as premium service propositions when base product commoditization intensifies.

Targeted M&A potential — acquiring upstream API capability or downstream commercial reach offers strategic shortcuts to capture margin and control risk.

Immediate (0–6 months): Conduct a supplier stress test and create a dual-sourcing plan for strategic API volumes; implement tightened batch-release testing and third-party audits for critical suppliers. Update commercial contracts with recall and quality breach clauses to protect margins and limit liability.

Near-term (6–18 months): Negotiate payer access strategies focusing on Medicare Part D formularies and state program placements; deploy competitive tender response teams with playbooks tuned to handle cyclical price pressure. Consider strategic inventory buffers calibrated to cost-of-carry and tender risk.

Medium-term (18–36 months): Evaluate targeted M&A to acquire API capability or to vertically integrate high-risk supply nodes — run scenario-based valuations reflecting possible quality events and price cycles. Invest in quality systems and digital traceability to materially lower recall risk and improve bid outcomes.

Our full-service offering turns the analysis summarized here into executed outcomes: integrated market models delivered as interactive workbooks, supplier due-diligence templates, tender and contracting playbooks, and hands-on M&A screening. We combine quantitative forecasting with operational readiness tools so leadership teams can move from insight to action within 90 days.

This preview surfaces the strategic contours your team needs to prioritize 2026 decisions. The full PW Consulting Atorvastatin Calcium Market report contains the granular segment-level breakouts, supplier-by-supplier profiles, downloadable financial models and executable commercial playbooks necessary to operationalize these recommendations. We have intentionally withheld detailed segmentation tables and proprietary scenario outputs in this public preview to preserve the value of the full deliverable.

To access the complete analysis — including region/type/application splits, interactive scenario models, and a prioritized target list for acquisition or partnership — contact PW Consulting or visit our report portal for the full report and executive workshop options.

For detailed analysis of this topic, please visit the official page:Atorvastatin Calcium Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com