Anti-Ageing Products Market Trends, Competitive Landscape & Growth Forecast

Health |

2026-05-04 15:29:49

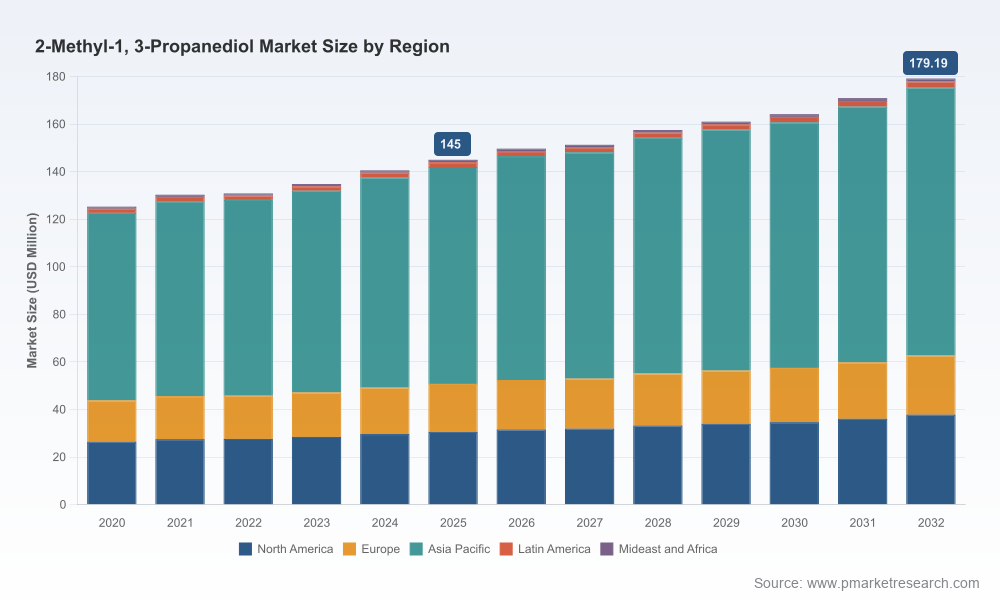

The global market for 2‑Methyl‑1,3‑propanediol (commonly referred to as MPDiol) is entering 2026 from a position of steady, structurally supported growth. Using 2025 as the base year, our analysis places the market at approximately USD 145.0 Million (revenue unit: Million) with a compounded annual growth rate (CAGR) of roughly 3.0% over the 2026‑2032 forecast horizon. Under the baseline projection, the market expands progressively to a projected value in the high USD hundreds of millions by 2032, reflecting steady demand reinforcement from polymer, coatings and specialty chemical end markets.

2-Methyl-1, 3-Propanediol Market

Two features define the current landscape for strategic planners: a high degree of market concentration among a few integrated suppliers, and a demand profile that remains anchored in industrial polyester and related resin systems while gradually diversifying into higher‑value and sustainability‑oriented applications. These characteristics create discrete opportunities — and asymmetric risks — for incumbents, suppliers, buyers and potential new entrants.

2-Methyl-1, 3-Propanediol Market

From a production standpoint, the commercial route for MPDiol relies on the hydroformylation pathway using allyl alcohol as a key precursor. This implies that feedstock availability, price volatility in propylene derivatives, and the integrity of integrated manufacturing chains materially affect both cost curves and reliability of supply. Several large chemical companies operate integrated chains and proprietary purification technologies, which create structural differentiation in product quality, yield and logistics cost.

2-Methyl-1, 3-Propanediol Market

The market’s high concentration amplifies supplier influence on pricing and service levels. For strategic planners, this translates into two imperatives: (1) secure term supply where possible and (2) build contingency plans that include validated secondary sources or tolling arrangements. Vertical integration and co‑location of monomer and downstream resin facilities continue to be key defensive strategies for incumbents.

Regulatory signals are also relevant to supply dynamics. Notably, a US EPA decision in mid‑2024 established an exemption for certain polymerized systems containing MPDiol as inert ingredients in pesticide formulations. While that ruling is narrowly framed, it illustrates how regulatory clarification can open incremental demand pathways or simplify formulatory workstreams — an important consideration for suppliers and specialty end‑users evaluating the economics of lower‑volume, high‑value applications.

Historically, the bulk of MPDiol demand has been tied to polyester resins used in composite materials and coatings, with supplementary volumes absorbed by polyurethanes, plasticizers and specialty chemical formulations. Over the coming planning cycle, demand growth is being driven by a mix of conventional industrial recovery patterns, incremental substitution away from legacy glycols in select high‑performance resins, and the emergence of sustainability‑driven product specifications.

Two demand vectors stand out for 2026 strategic planning: (1) the ongoing uptake of MPDiol in unsaturated polyester resin systems for composites and coatings — driven by performance advantages such as improved mechanical and thermal properties — and (2) growth in smaller but higher‑margin applications that require high‑purity, specialty grades (including certain personal care and formulated specialty polymers). For buyers and producers alike, aligning product portfolios and quality controls to these vectors will yield differentiated returns.

The sector is effectively dominated by a handful of well‑capitalized chemical corporations with integrated asset bases and branded product lines. The strategic postures we observe among the leading players shape market access, technology trajectories, and the range of viable commercial strategies.

Collectively, these suppliers’ behaviors — investments in purification, selective capacity additions, and product differentiation — underscore barriers to rapid commoditization and suggest sustained supplier pricing power unless demand accelerates materially or new low‑cost entrants scale quickly.

We frame three realistic scenarios to support decision‑making in 2026, with associated tactical responses:

Our complete 2‑Methyl‑1,3‑Propanediol market study is designed expressly as a decision‑grade tool for 2026 planning cycles. Key deliverables include:

For executives making strategic calls in 2026, MPDiol is a mature yet evolving intermediate: growth is steady, supplier concentration is high, and profitable upside is attainable through targeted product differentiation, secured supply lines, and nimble regulatory engagement. The right mix of contracting discipline, selective capital deployment and forward‑looking sustainability initiatives will determine which players capture value over the next planning cycle.

To access the granular forecasts, regional and application breakdowns, and the full set of supplier profiles and scenario models — information we intentionally summarize here to preserve competitive integrity — please consult the full PW Consulting 2‑Methyl‑1,3‑Propanediol Market report and datasets on our report page. The detailed segmentation tables and downloadable spreadsheets provide the actionable figures needed to convert these strategic insights into investment‑grade decisions.

For detailed analysis of this topic, please visit the official page:2-Methyl-1, 3-Propanediol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com