Hydraulic Dock Leveler Market — Strategic Briefing for 2026 Decision-Makers

As PW Consulting’s lead industry analyst, I present a directional briefing that frames the strategic choices facing manufacturers, logistics operators, private equity, and infrastructure investors focused on hydraulic dock levelers. This article synthesizes our market model through the 2026 planning horizon, highlights competitive and regulatory inflection points, and sketches the practical use-cases in which our full study will materially change capital-allocation and go-to-market decisions.

Hydraulic Dock Leveler Market

Why this study matters for 2026 strategy

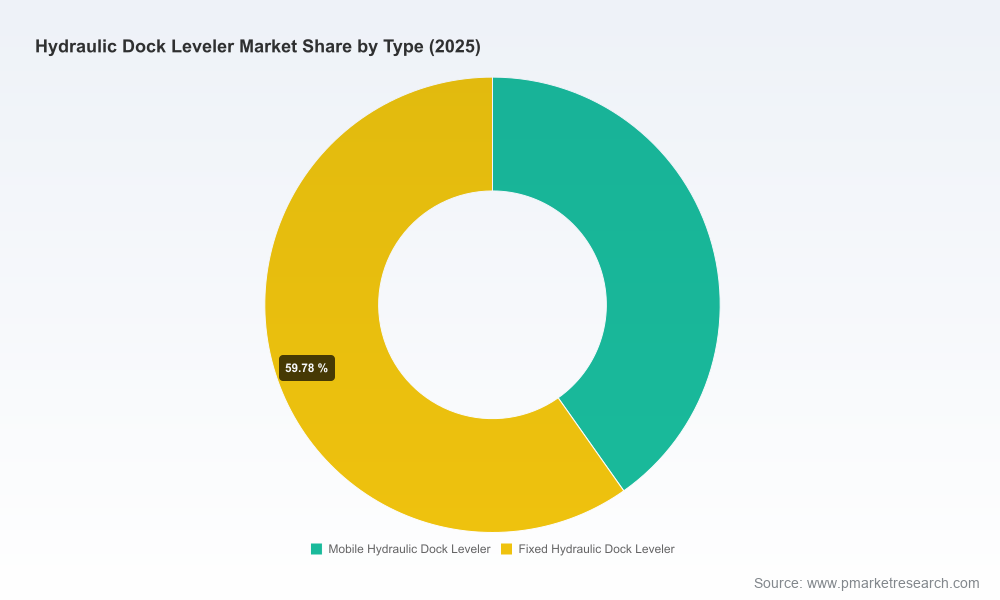

The hydraulic dock leveler market has demonstrated steady, investment-grade growth through the last five years and continues on a predictable expansion path. Our base-year assessment (2025) values the global market at roughly USD 1.75 billion (USD Million basis) and our scenario-led forecast shows continuation of this trajectory into the long term — reaching roughly USD 2.71 billion by 2032 on a compound annual growth rate of 6.5%. The near-term projection for 2026 also anticipates a measurable uplift as industrial automation, safety-driven retrofit programs, and e-commerce logistics capacity investments maintain momentum.

Hydraulic Dock Leveler Market

For 2026 planning cycles, three strategic imperatives emerge: (1) prioritize compliance-led product roadmaps to leverage new normative requirements, (2) make retrofit vs. replace decisions using supplier-specific TCO and downtime models, and (3) position for aftermarket and service revenue capture as installation volumes and installed-base replacement windows widen. The PW Consulting study supplies the decision-grade inputs required to operationalize each imperative.

Hydraulic Dock Leveler Market

Market dynamics shaping competitive advantage

- Regulatory and standards pressure: Recent and emergent standards (notably ANSI MH30.1-2022 and related guidance on built-in and portable levelers) are moving from recommendations to procurement filters among enterprise buyers. Certification — and the ability to demonstrate compliance with testing protocols — is already a buying criterion for large distribution centers and public-sector contracts. Vendors that certify models are experiencing shortened evaluation cycles and face higher expectations around warranty and documentation.

- Product differentiation is technical, not just price-based: Hydraulic control architectures, vertical storing versus pit-mounted form factors, NEMA-rated control stations for corrosive environments, and lifecycle maintenance features (e.g., reduced-pin wear designs, easier access for seal replacement) are the real battlegrounds. Those design choices materially influence maintenance windows and cost of ownership metrics used in CapEx decision trees.

- Aftermarket service economics: As install bases grow, service, parts, and maintenance contracts become the higher-margin lever. Our models show that operational savings from reduced downtime and longer service intervals often justify premium purchase prices — if those savings can be credibly quantified and contracted.

- Supply-chain and raw-material risk: Steel and hydraulic components remain drivers of bill-of-materials volatility. Strategic procurement teams are increasingly requiring supplier-level BOM transparency, multi-sourcing options for critical components, and pass-through clauses in long-term contracts to mitigate margin erosion in the presence of commodity swings.

Competitive landscape — what we see and why it matters

The sector displays moderate market concentration: the top three suppliers account for roughly a quarter of market revenues (CR3 ≈ 26.5%), and the top five account for approximately two-fifths (CR5 ≈ 41.2%). That structure creates differentiated strategic pathways: scale players can pursue integrated service platforms and global distribution, while regional and niche innovators can win on specialized features, quicker iterations, and local service networks.

- Overhead Door Corporation: The company’s recent H68R and H78R releases — ANSI MH30.1-2022 certified, with top-side adjustable leveling bolts and expanded warranty options — are illustrative of a certification-first product strategy. This approach reduces buying friction in regulated tenders and public-sector procurement, and the investment in a cleaner X-frame pit design targets lower lifetime maintenance costs.

- Poweramp & DLM (Divisions of Systems, LLC): Both brands continue to emphasize operational ergonomics (push-button activation, vertical storing designs) and variation in capacity ranges. Their product breadth supports channel partners that prioritize one-stop procurement and simplified spares management.

- Rite-Hite: Focused on engineered systems, Rite-Hite’s vertical storing models and platforms such as the Smooth Transition Dok System® underscore a strategy of selling integrated material-handling outcomes (safety + throughput) rather than compartmentalized hardware.

- Pentalift, Nordock, McGuire, Blue Giant: These players highlight differentiated propositions — from heavy-capacity offerings and interlock compatibility to low-downtime push-button series and corrosion-resistant NEMA4X control stations. Each presents a defensible niche in which aftermarket and retrofit services can be monetized.

These strategic positions imply specific procurement and partnership actions. For vendors, investing in certification and service networks delivers premium capture. For buyers, supplier selection should be based on validated TCO models and scenario-tested uptime guarantees rather than headline unit pricing.

Practical intelligence the report delivers (high-level)

Our full PW Consulting study is purpose-built to convert market insight into executable choices for 2026. Key operational deliverables include:

- Scenario-driven demand models covering 2026–2032 with segmented base-case, upside, and downside forecasts tied to warehouse automation spend and retrofit cycles.

- Supplier benchmarking matrices that align product features, certification status, warranty terms, typical lead-times, and channel footprints to buyer use-cases.

- TCO and ROI calculators calibrated for vertical-storing vs. pit-mounted vs. edge-of-dock deployments — with modular inputs for labor rates, downtime costs, and parts-replacement schedules.

- Regulatory compliance checklists and procurement language templates that procurement teams can plug into RFPs to enforce ANSI-conformant specifications and enforceable performance SLAs.

- Aftermarket and service expansion playbooks: upsell pathways, spare-parts assortments, field-service economics, and subscription pricing models that increase customer lifetime value.

- Supply-chain risk register and mitigation roadmaps including alternative-sourcing recommendations for hydraulic pumps, seals, and electrical control components.

- M&A and partnership radar: target profiles, valuation multiples, and integration risk factors for private equity and industrial acquirers looking to consolidate regional service networks.

Note: In keeping with our “trailer” approach, this briefing intentionally omits confidential level segmentation tables, regional and application-specific share percentages, and supplier-level pricing schedules. Those details are available through the full report and are essential for transaction- or bid-level work.

Decision frameworks — how to use the research in 2026 plans

- Capital budgeting: Use our TCO outputs to define replacement thresholds (e.g., at what diminishing uptime or rising maintenance cost you trigger a capex replacement instead of incremental repairs).

- Procurement: Build RFP requirements around certification and maintainability metrics, demand clear lead-time commitments, and evaluate vendors on total lifecycle cost rather than unit price.

- Product roadmap prioritization (for OEMs): Invest in certification, modular control systems (for easier field upgrades), and corrosion-resistant options where industrial or maritime applications dominate.

- Service expansion: Treat service contracts as a strategic growth engine — structure them with performance SLAs, predictive-maintenance analytics, and parts-bundling that improve margins over time.

- M&A and partnerships: Seek regional service-platforms and control-electronics specialists to accelerate aftermarket capability and reduce field-service risk.

What to expect next — actions for 90/180/360 days

- 90 days: Align procurement and engineering teams on the new ANSI expectations and begin updating RFP templates to reflect warranty and certification conditions as mandatory pass/fail criteria.

- 180 days: Run pilot ROI projects on retrofit vs. replacement at two representative sites to validate model assumptions about downtime savings and parts-life improvements.

- 360 days: Execute a supplier rationalization that favors partners delivering certified models and demonstrable service economics; concurrently launch a bundled aftermarket offering for a selected region.

Conclusion and next steps

The hydraulic dock leveler market is not a low-margin commodity space — it is a technical, rules-driven equipment category where standards compliance, service economics, and design-for-maintainability drive differentiated outcomes. With an expanding market base (historical resilience to 2025 and a forecast CAGR of about 6.5% into 2032), 2026 is a pivotal year for firms to convert product and service capabilities into durable commercial advantage.

Our full PW Consulting Hydraulic Dock Leveler Market study contains the proprietary segment-level tables, supplier scorecards, scenario models, and executable playbooks referenced above. For client teams preparing 2026 budgets, procurement strategies, or M&A screens — those granular deliverables are the operational intelligence you will need. Contact our research desk or visit the PW Consulting market page to access the complete dataset and schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Hydraulic Dock Leveler Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com