HDI Market 2026: Strategic Preview for Corporate Decision‑Making

As PW Consulting’s lead industry analyst, I present a focused preview of our HDI Market (High‑Density Interconnect Printed Circuit Board) research—an actionable briefing designed to orient corporate leaders, strategy teams, and investors as they set priorities for 2026. This piece synthesizes the study’s high‑level trajectory, competitive implications, and decision frameworks while intentionally withholding core segmentation tables and granular splits to preserve the report’s value as a gated strategic asset.

HDI Market

Market trajectory at a glance

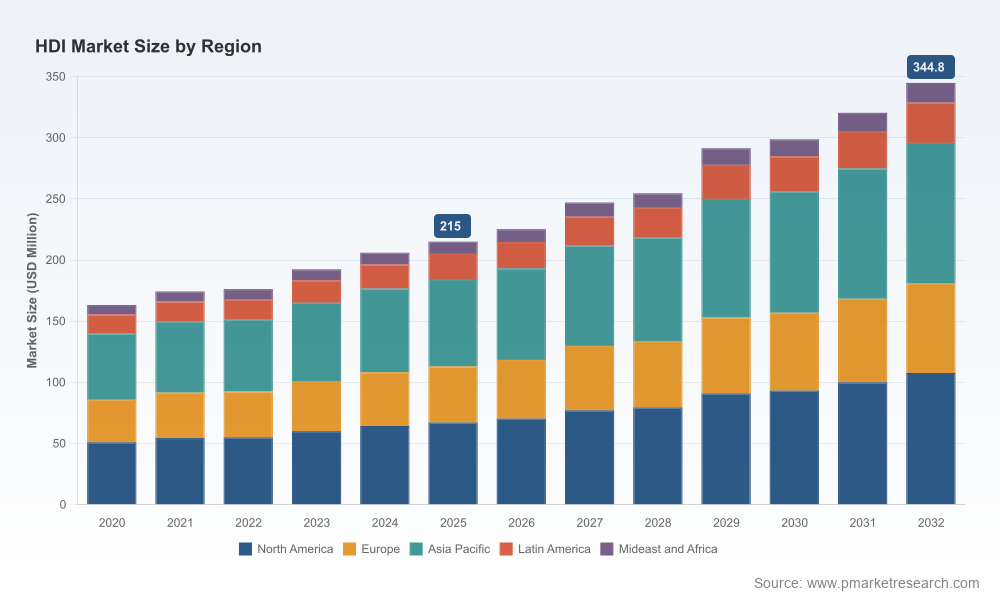

The HDI market demonstrates sustained expansion from the early 2020s into the next decade. Our base year is 2025 (USD, Million), and the historical series shows a recovery and steady growth path from 2020 through 2025, culminating in an overall market size of approximately 215.0 (USD Million) in 2025. Looking forward, the model projects expansion through the forecast window (2026–2032) to roughly 344.8 (USD Million) by 2032, implying a compound annual growth rate (CAGR) of 6.98% across the forecast period.

HDI Market

These headline dynamics reflect structural demand drivers—electrification of transport, densification of consumer and telecom electronics, and more aggressive adoption of multilayer HDI architectures in power and RF applications—that combine to extend both volume demand and value per board.

HDI Market

Why this report matters for 2026 corporate choices

- Investment timing and sizing: A mid‑single‑digit CAGR through 2032 signals durable upside but also calls for staged capital deployment. Organizations must balance capacity expansion against modular, flexible investments in advanced manufacturing equipment.

- Portfolio prioritization: HDI enables miniaturization and higher signal integrity—attributes that determine which product lines require immediate redesign investments versus those that can be deferred.

- Supply chain resilience: Ongoing commoditization in some segments contrasts with premium pricing in ultra‑high‑density and high‑frequency boards. Strategic sourcing and dual‑sourcing decisions should incorporate capacity maps, technology readiness, and regional risk profiles.

- M&A and partnership screening: Fragmented concentration metrics (modest top‑three/top‑five shares) point to opportunities for value‑creating consolidation or targeted acquisitions to secure technology or capacity.

- Regulatory and sustainability alignment: EV electrification and renewables integration create regulatory tailwinds for HDI adoption in power electronics; firms must embed compliance and sustainability KPIs into CapEx and product roadmaps.

What the full HDI Market report contains (practical deliverables)

Our HDI Market study is built for operators who need to move from insight to action. Key operational outputs include:

- Top‑down market model (2020–2032) with scenario variants that stress macroeconomic, technology adoption, and material price shocks.

- Forward‑looking demand drivers by technology class and application cluster, with elasticity estimates to inform pricing and revenue sensitivity analyses.

- Cost and margin benchmarking for incumbent and entrant manufacturers, including equipment amortization schedules and labor intensity profiles.

- Supply‑side capacity maps with lead‑time overlays and bottleneck risk ratings—useful for procurement and capacity planning.

- Competitive heatmaps and playbooks for market entry, differentiation by process capability, and integration strategies with semiconductor and module assemblers.

- Transaction pipeline: candidate M&A targets, strategic fit matrices, and integration risk checklists to accelerate diligence.

Note: This preview intentionally omits the detailed segmentation tables (regional, type, and application splits) that appear in the paid report. Those tables are essential for precise volume allocation and are accessible exclusively through the full HDI Market offering.

Competition and positioning—what leading players reveal

The competitive landscape is composed of a mix of specialized HDI leaders and diversified electronics manufacturers. Market concentration is relatively low: collective shares of the top three and top five firms are modest, indicating room for strategic moves by ambitious midsize players. Below are interpretive profiles of representative companies and the strategic inferences we draw for 2026.

- Zhen Ding Technology Corporation (Taiwan): Strengths in high‑layer‑count HDI for automotive and industrial applications position Zhen Ding as a go‑to partner for OEMs transitioning to complex battery management and vehicle control systems. For competitors, Zhen Ding’s playbook underscores the importance of process depth and automotive qualification pipelines.

- Unimicron Technology Corp (Taiwan): Its focus on telecommunications and computing HDI highlights the premium associated with high‑frequency and high‑I/O boards. Firms aiming to penetrate telecom OEMs should prioritize RF characterization labs and co‑development agreements tied to 5G/6G roadmaps.

- AT&S (Austria): AT&S’s consumer and automotive exposure shows a hybrid strategy of scale plus engineering differentiation. Their approach illustrates the value of geographic proximity to European OEMs and joint‑engineering contracts to shorten development cycles.

- Ibiden Co., Ltd. (Japan): Deep capabilities in high‑frequency and power HDI make Ibiden a benchmark for firms targeting power electronics and industrial RF. Their investments in material science and controlled impedance processes provide a template for product‑level differentiation.

- TTM Technologies, Inc. (U.S.): U.S. industrial and automotive focus suggests a strategic advantage for companies that can combine domestic supply with defense and industrial compliance—an important consideration given shifting onshore sourcing policies.

- Meiko Electronics Co., Ltd. (Japan): Specialist orientation toward automotive and EV applications demonstrates the commercial payoff of aligning roadmaps with electrification trends—especially for suppliers that can meet supplier quality and longevity demands.

- Samsung Electro‑Mechanics (South Korea): Their pursuit of ultra‑high‑density interconnects for consumer electronics indicates where volume and technology trajectories converge. Consumer OEMs continue to value vertically integrated suppliers that can manage tight BOM and timing constraints.

These snapshots are complemented in the full report by competitive positioning maps, capability matrices, and supplier scorecards that quantify technology depth, certification status, and capital intensity.

Dynamics shaping 2026 outcomes

- Electrification and automotive demand: With global EV production surpassing 19 million units in 2025, multilayer HDI adoption in battery management and power conversion is a material growth vector. OEMs and Tier‑1s will increasingly penalize partners who cannot meet automotive qualification and traceability requirements.

- Telecom densification: Rapid 5G rollout stimulated a roughly 21% increase in procurement of high‑frequency HDI boards in 2025—an acceleration that supports continued capex in RF‑optimized lines and laminate innovation.

- Material and labor cost dynamics: HDI designs reduce material footprint in many compact devices but require higher‑precision materials and specialized equipment, raising per‑unit labor and capital intensity. Margin management will be driven by yield improvements and automation in microvia formation and laser drilling.

- Capacity moves and greenfield additions: Recent capacity additions—such as a new multilayer HDI facility announced in 2025—underscore ongoing private sector responses to demand. Buyers must calibrate supplier selection not only on nameplate capacity but on ramp feasibility and process qualification timelines.

- Renewables and power efficiency: HDI boards that support power electronics contribute to efficiency gains in renewable energy systems, creating cross‑sector demand pull and potential for co‑development programs with inverters and BMS suppliers.

A pragmatic decision framework for 2026

Leaders should operationalize the report’s insights through a concise decision framework:

- Scenario planning: Build three internal demand scenarios (base, upside tied to EV/5G acceleration, downside tied to macro slowdown) and stress test capital allocation across them.

- Capability gap analysis: Audit internal design and manufacturing capabilities against the technical requirements for high‑frequency and high‑layer HDI. Prioritize investments that shorten time‑to‑market for high‑value boards.

- Supplier segmentation: Classify suppliers by risk and strategic value—tiering them for critical long‑lead components, qualification pathways, and co‑innovation potential.

- Operational resilience: Invest in process automation and yield analytics to offset rising labor intensity; secure alternate laminate and plating sources to mitigate material disruptions.

- M&A and partnership playbook: Target bolt‑on acquisitions that accelerate access to specific process capabilities (e.g., microvia formation, high‑TG laminates) rather than trying to build every capability in‑house.

- Regulatory and sustainability alignment: Integrate compliance timelines (automotive, telecom) and sustainability metrics into procurement contracts and supplier scorecards to avoid downstream rework and market access delays.

Final note: why access to the full dataset matters

This preview surfaces the strategic contours and decision levers that will define successful positioning in 2026. However, the granular segmentation—regional flows, application shares, and precise type‑level volumes—are intentionally withheld here. Those splits are essential for precise capacity planning, regional exposure assessment, and deal valuations, and they form the core deliverable of the full HDI Market report.

If your 2026 strategy depends on optimizing CapEx, selecting supply partners, or executing M&A in the HDI space, the complete dataset and accompanying scenario models are indispensable. The full report includes downloadable models, supplier scorecards, and a transaction shortlist that directly support board‑level and investment committee decisions.

To access the full HDI Market report and our proprietary datasets, please visit the HDI Market page on the PW Consulting portal. Our team is available to run custom workshops that translate these insights into a 90‑day action plan tailored to your business priorities.

For detailed analysis of this topic, please visit the official page:HDI Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com