Multi-crystalline Ingot Furnace Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a synthesized, decision-focused preview of our new Multi-crystalline Ingot Furnace Market study. This briefing distills the structural trends, supplier dynamics, and near-term tactical imperatives that will matter most to executives planning capital allocation, procurement cycles, and technology roadmaps in 2026. It deliberately demonstrates analytical depth while reserving the granular segment tables and proprietary supplier scoring for the full report.

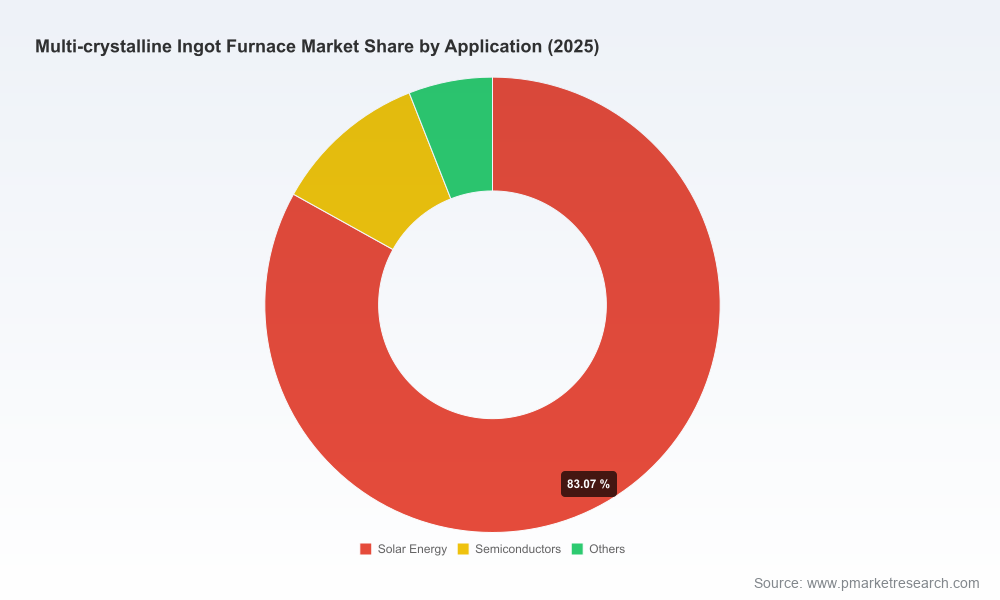

Multi-crystalline Ingot Furnace Market

Why this study matters for 2026

The multi-crystalline ingot furnace market is at an inflection point between steady demand growth and intensified operational pressures. Our macro model shows the market expanding from a mid‑hundred million USD base in the early 2020s to a substantially larger market by the end of the next decade — driven by solar deployment, semiconductor niche demand, and equipment refresh cycles. The forecast period (2026–2032) is modeled at a compound annual growth rate (CAGR) of 5.9%, underscoring predictable expansion but also signaling a market that rewards timing, supplier selection, and process optimization.

Multi-crystalline Ingot Furnace Market

For executives, the 2026 planning cycle is the last practical window to align CAPEX with tightening regulatory efficiency requirements, raw-material inflation pressures, and automation imperatives. Decisions made this year will determine installed base economics, service exposure, and product competitiveness into the 2030s.

Multi-crystalline Ingot Furnace Market

What this briefing covers — and what’s deliberately held back

- High-level growth trajectory and the demand drivers shaping furnace uptake through 2032, backed by a rigorous market model that reconciles historical 2020–2025 performance with scenario-based projections for 2026–2032.

- Operational levers that materially affect total cost of ownership (TCO): energy efficiency, thermal cycle control, automation integration, and supply-chain resilience.

- A competitive assessment of the core global suppliers, highlighting strategic strengths, capability clustering, and partnership levers.

- Actionable guidance for procurement, R&D prioritization, and M&A signal scanning tailored to 2026 budgets and risk tolerances.

What we do not disclose in this preview: the granular regional and application splits, price-by-configuration tables, and the proprietary supplier scorecards. Those segmented data and company-level metrics are accessible in the full PW Consulting report and are the key assets to execute procurement RFPs and competitive intelligence programs.

Market structure and concentration: implications for strategy

The market exhibits a fragmented competitive structure: measured concentration among the top three and top five players is modest, indicating that no single incumbent dominates the arena. This fragmentation creates upside for equipment differentiation, aftermarket service models, and selective consolidation. For strategic buyers, it means negotiation leverage varies by furnace class and by supplier specialization — a one-size procurement approach will produce suboptimal TCO outcomes.

Fragmentation also signals an opportunity for technology-led entrants and regional OEMs to capture share via performance, localized support, or cost-effectiveness. Conversely, suppliers with vertically integrated capabilities or established aftermarket networks can command premium margins and longer customer lifecycles.

Competitive landscape — who to watch and why

- GT Advanced Technologies (Merrimack, NH, USA): Strength lies in directional solidification (DSS) furnace platforms tailored for solar wafer casting. Their engineering pedigree and existing customer base position them well for buyers prioritizing throughput predictability and known process windows.

- ALD Vacuum Technologies (Hanau, Germany): ALD’s Silicon Crystallization Unit series demonstrates strengths in precision thermal control and modularity, appealing to manufacturers seeking tight crystallographic properties and energy efficiency. Their European base also provides advantages where regulatory energy targets are strict.

- Ferrotec Corporation (Tokyo, Japan): Ferrotec brings integrated thermal systems and materials know‑how, beneficial for buyers that value co‑optimization of crucible, hot‑zone components, and furnace controls.

- Zhejiang Jingsheng Mechanical & Electrical Co., Ltd. (Hangzhou, China): A strong regional OEM with competitive semi-melting, high‑efficiency offerings targeted at volume PV producers. Their proximity to supply chains and pricing position makes them a frequent choice in high-throughput lines.

- Tanlong Photoelectric & Zhejiang Jinggong Technology (China): These companies represent focused domestic suppliers with product portfolios optimized for photovoltaic applications and localized service models — important alternatives for Asian manufacturers reducing logistical and tariff risk.

Each supplier profile in the full study includes capabilities mapping (thermal architecture, control systems, automation compatibility), lifecycle cost models, and strategic posture (R&D focus, partnership tendencies). That granular intelligence is essential when selecting an OEM for multi‑year production roadmaps.

Key market dynamics shaping 2026 choices

- Energy efficiency mandates: Regulatory and corporate decarbonization targets are raising the bar. New furnace deployments are required to deliver material energy reductions versus legacy units — PW modeling points to required performance improvements in the 35–40% range to meet anticipated mandates. For CAPEX planners, this raises the effective replacement threshold: retrofitting older lines may no longer be cost‑effective without major upgrades.

- Automation and predictive maintenance: Modern furnaces that integrate automation reduce labor dependency by roughly 30% while enabling predictive maintenance regimes that push process yield above 98%. Such capabilities change the economics of aftermarket service contracts and should be central in supplier evaluation criteria.

- Raw‑material pressure: Graphite hot‑zones and crucibles — a small share of equipment BOM by value — have outsized schedule and cost impact. These subcomponents face lead‑time constraints and annual inflation pressures often in the high single‑digits to mid‑teens percent, meaning procurement contracts and inventory strategy must explicitly cover critical spares and price escalation risk.

- Fragmentation and service economics: Because the market’s top players do not dominate, aftermarket services and spare parts are fertile areas for margin expansion. Buyers should model spare part availability and the supplier’s service footprint as core inputs to lifetime equipment cost, not as afterthoughts.

Practical frameworks and tools in the full report

The full PW Consulting study provides decision-ready tools designed for 2026 planning cycles, including:

- Dynamic TCO calculator that captures purchase price, energy consumption, spare‑parts inflation, downtime cost, and projected yield impacts from automation.

- Procurement playbook with negotiation levers: warranty structures, spare‑part consignment, performance‑tied payments, and trade‑in options aligned to CAPEX amortization schedules.

- Supplier short‑listing matrix combining technical fit, regional support capability, financial health indicators, and strategic alignment to circularity/efficiency goals.

- Scenario-based CAPEX phasing guide that aligns furnace upgrades with regulatory milestones and expected product-cycle changes in the PV and semiconductor markets.

- M&A and partnership scanner that identifies likely consolidation targets and technologies that could disrupt current incumbents.

Recommended actions for 2026 — prioritized

- Prioritize energy‑efficient furnace models for any new investments. The coming regulatory and corporate energy targets will raise operating cost differentials between modern and legacy units.

- Lock critical graphite and crucible supply via multi‑year contracts or strategic inventory buffers to immunize your production schedule against lead‑time spikes and inflation.

- Make automation a non‑optional specification. Automation yields labor cost reductions, higher uptime, and enables predictive maintenance — all of which materially improve ROI trajectories.

- Use the PW TCO calculator during RFP evaluation to quantify lifecycle cost differences across vendors rather than relying on headline equipment prices.

- Negotiate performance‑based contracts (e.g., energy consumption thresholds, acceptable defect/yield bands) to shift risk and incentive toward suppliers with proven reliability.

- Consider partnering with suppliers who offer strong aftermarket networks if your resilience objective emphasizes uptime over minimal initial spend.

- Run a 36‑month CAPEX phasing exercise that aligns equipment purchases with forecasted module/wafer demand to avoid overcapacity in intermediate years.

Closing — the strategic value of the full PW study

For executives making binding commitments in 2026, timing and supplier choice will determine operating cost curves for a decade. Our study converts market trajectory, supplier capabilities, component‑level risks (notably graphite and crucibles), and regulatory imperatives into actionable procurement and R&D roadmaps. It is designed as a working tool for procurement leads, factory operations heads, and corporate strategy teams who must reconcile capital discipline with competitive performance gains.

If you are evaluating furnace replacements, new production lines, or M&A options in 2026, PW Consulting’s full report provides the segmented demand matrices, supplier scorecards, and scenario models required to execute with confidence. Access to those granular insights is intentionally gated to ensure decision-makers receive the tailored, validated intelligence necessary to close contracts and prioritize investments.

Contact PW Consulting to request the full Multi-crystalline Ingot Furnace Market report and the accompanying TCO toolkit — we will provide the detailed splits, vendor benchmarking, and customizable models you need to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Multi-crystalline Ingot Furnace Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com