Dominique Rogeau A Name That Reflects Individual Identity and Curiosity

Health |

2026-01-05 06:33:47

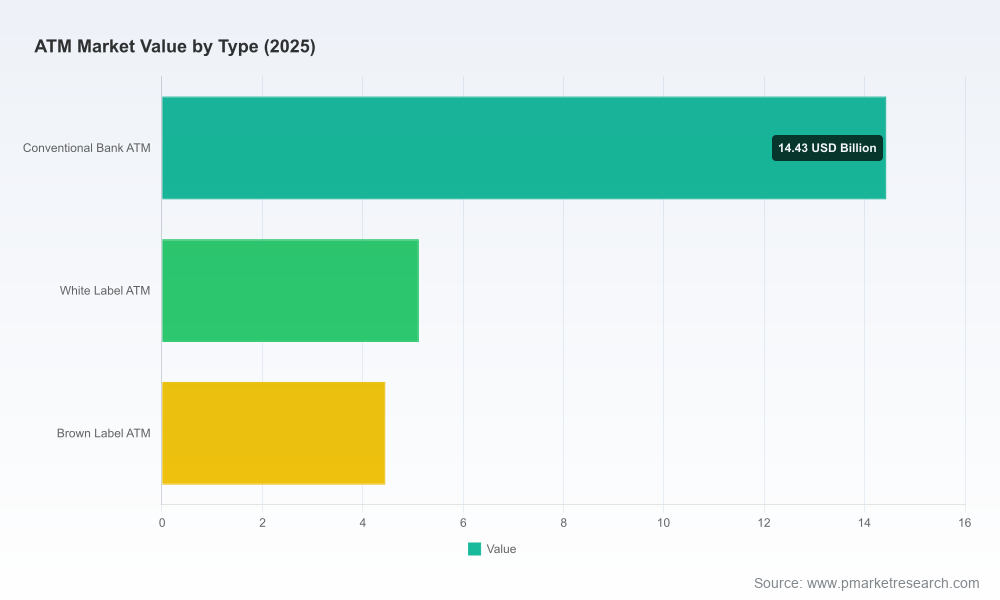

The global ATM market sits at a pivotal inflection point. After a measured recovery through the early 2020s, the installed base and service ecosystem are entering a period of steady modernization. Our analysis establishes the ATM market at approximately USD 24.0 Billion in the base year (2025) and models a compound annual growth rate (CAGR) of 4.9% across the 2026–2032 forecast window, driving the market toward roughly USD 34.4 Billion by 2032. Behind that headline growth are concentrated upgrade cycles, regulatory-driven ripples, and technology-led redefinitions of value — from “cash dispensers” to multifunctional, AI-enabled service points.

ATM Market

Capital allocation and timing: With material investment required to meet recent regulatory mandates and to deploy cash-recycling and deposit-enabled “Super ATMs,” firms must prioritize which estate segments to upgrade in 2026 to avoid stranded assets or compliance exposure.

ATM Market

Vendor strategy and procurement: The market shows meaningful concentration among leading suppliers (CR3 ≈ 55%; CR5 ≈ 68%), making vendor selection and leverage critical. Our research identifies which OEM and software partners are best positioned for deep integrations versus transactional supply.

ATM Market

Security and compliance roadmaps: PCI DSS v4.0, TR‑31/TR‑34 key management mandates, and TLS requirements have converted what were once optional upgrades into mandatory projects. Our scenario work quantifies the likely upgrade demand and sequencing that will consume a significant portion of 2026–2027 implementation budgets.

Operational economics of new capabilities: Cash-recycling and advanced cash-management systems materially change operating cost profiles — recent industry work highlights recycling’s potential to represent a meaningful share of branch ATM operating costs. Banks and deployers need to understand total cost of ownership (TCO) implications before committing to widescale refreshes.

Service design and customer experience: Super ATMs with biometric authentication, integrated bill pay, and real-time service diagnostics are altering customer journeys. Early movers can monetize improved uptime and reduced branch load, while laggards face eroding retention.

Our full study blends quantitative forecasting with executable playbooks. The core deliverables are designed for CFOs, heads of retail banking, operations leads, CIOs, and procurement teams preparing 2026 roadmaps:

The ATM vendor ecosystem is evolving from a hardware-centric market into an integrated hardware‑software‑services contest. A handful of global players lead product innovation and distribution, with adjacent incumbents and regional specialists filling niche roles. Below are strategic summaries of the most consequential firms for 2026 planning.

Diebold Nixdorf (United States) — Strengths: a broad portfolio that spans lobbies and in‑wall machines, advanced cash-recycling, biometric and NFC enablement, and the Vynamic software suite for AI-driven fraud and estate management. Strategic implication: Diebold is positioned as a one-stop partner for full-estate modernization; institutions seeking single-vendor estate consolidation should model integration and switching costs against long-term software lock‑in.

NCR Atleos (United States) — Strengths: established SelfServ hardware family, network play via surcharge-free partnerships, and recent recognition for AI-assisted service resolution. Strategic implication: NCR’s emphasis on service intelligence reduces operational disruption risk. Deployers focused on uptime and predictive maintenance should prioritize pilots with NCR’s service analytics to quantify savings.

Hyosung TNS / Hyosung Americas (South Korea / United States) — Strengths: retail-facing ATMs, Secure Cash Transfer automation, biometric authentication, and an integrated software suite. Strategic implication: Hyosung is attractive for retail and omnichannel strategies; commercial partnerships (e.g., with logistics and retail networks) can unlock off-balance-sheet deployment models.

GRG Banking (China) — Strengths: versatile hardware with bill-pay and video-teller integration. Strategic implication: GRG competes on cost and feature breadth in growth markets; multinational deployers should weigh total lifecycle support when considering entry into price-sensitive regions.

Hitachi Channel Solutions (Japan) — Strengths: advanced recycling units with anti-skimming and counterfeit serial-number detection. Strategic implication: Hitachi’s security-first hardware is a fit for institutions in markets with acute fraud risk; pairing with strong key-management practices will be essential.

OKI Electric Industry (Japan) — Strengths: high-capacity recycler modules and robust note-handling throughput. Strategic implication: OKI is optimal for high-transaction environments where throughput and cash capacity matter most; integration cost into existing estate should be modeled carefully.

KAL ATM Software GmbH (Germany) — Strengths: hypervisor-based ATM software with AI fault detection and estate analytics. Strategic implication: Software vendors like KAL lower the barrier to cross-vendor estate standardization; banks can use hypervisors to extend hardware life and centralize security updates.

Market momentum toward Super ATMs was reinforced at the ATMIA US Conference 2026, where deposit-enabled, recycling, and AI solutions dominated exhibitor roadmaps — signaling strong OEM commitment to multifunction devices.

Product launches and awards in early 2026 (e.g., Hyosung’s AI-powered ATMs and NCR’s industry award for AI-assisted service resolution) indicate a shift from feature parity to service and software differentiation.

Regulatory changes effective from 2025 (PCI DSS v4.0, TR‑31/TR‑34, TLS requirements and FDIC guidance) have crystallized a near-term upgrade wave that will define procurement timelines and capital needs.

Immediate estate audit: segment your ATM estate by upgrade urgency (compliance, customer impact, cost-to-serve) and capture five-year refresh windows in your 2026 budget cycle.

Compliance-first upgrades: sequence TR‑31/TR‑34 and PCI DSS v4.0 workstreams to capture synergies with TLS and key-management projects to minimize redundant device downtime.

Service-intelligence pilots: run focused pilots on AI-driven service resolution and fraud detection with partners that offer both hardware and analytics; measure MTTR and operational savings over a 6–12 month horizon.

Cash logistics optimization: quantify the trade-offs between cash-recycling adoption and branch cash handling costs, including the working capital and operational implications.

Vendor negotiation playbook: use concentration benchmarks to drive competitive tension in RFPs; consider split-sourcing hardware and software to avoid supplier lock-in where appropriate.

Partnerships and ecosystems: explore partnerships with retail networks, logistics providers, and fintechs to monetize new ATM services and share deployment economics.

Our report translates market-scale forecasts and regulatory overlays into executable roadmaps. We combine vendor-level intelligence, practical procurement tools, and financial models you can plug directly into 2026 capital-planning cycles. This preview surfaces the strategic framing — the full report provides the granular, auditable tables and segment-by-segment forecasts that CFOs and procurement teams need to finalize FY26 budgets.

Note: This article intentionally omits the detailed regional and application-level numeric splits included in the full dataset. To access the complete model, vendor scorecards, and downloadable forecast tables, please visit our report page or contact PW Consulting for a tailored briefing and dataset delivery.

For detailed analysis of this topic, please visit the official page:ATM Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com