Emerging Applications Accelerating the Global Pharmaceutical Filtration Market Growth Trajectory

Health |

2026-07-03 11:56:37

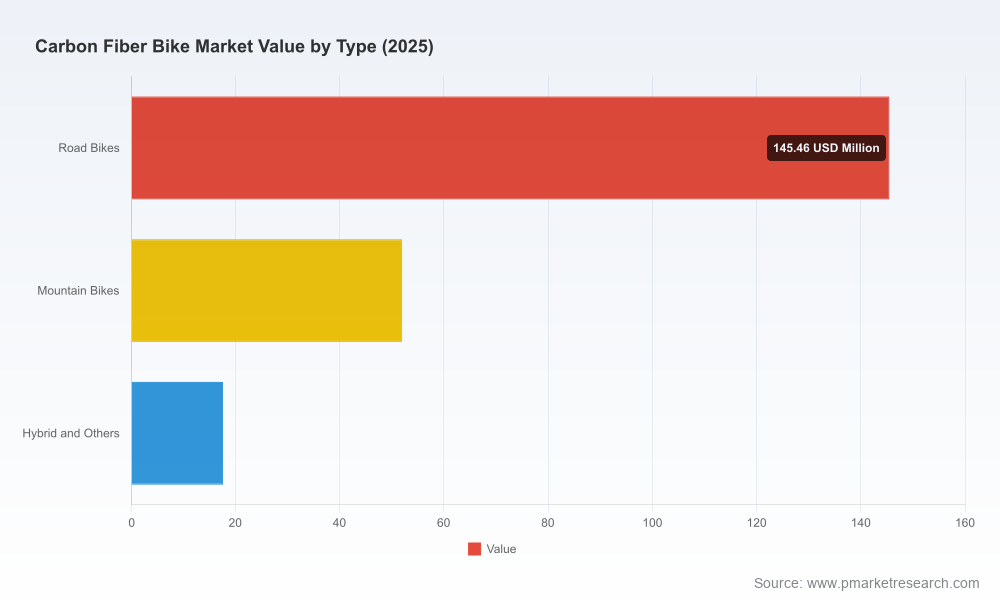

As PW Consulting’s senior strategy team and lead industry analyst, we present a focused synopsis of our Carbon Fiber Bike Market study designed to influence boardroom decisions in 2026. Grounded in a base year of 2025 and extending a detailed forecast through 2032, the research captures a market that has expanded steadily since 2020 and is expected to continue growing at a compound annual growth rate of approximately 6.98% for the forecast horizon. To illustrate scale and trajectory without exposing proprietary segment-level breakdowns, note the market moved from an aggregated industry revenue base in the low hundreds of USD Million in 2020 to a larger market in 2025, with our single‑line forecast projecting continued expansion into 2032—evidence that the category is matureing into a structurally larger premium niche within global cycling.

Carbon Fiber Bike Market

Capital allocation precision: the forecast and scenario models enable finance teams to size investments in tooling, composite production capacity and R&D with defensible revenue and margin pathways.

Carbon Fiber Bike Market

Product and portfolio roadmaps: engineering and marketing can align product launches (entry, mid and premium tiers) to demand inflection points identified in the report.

Carbon Fiber Bike Market

Supply‑chain and procurement playbooks: the combination of raw‑material price intelligence and supplier risk heatmaps is actionable for procurement to reduce exposure to carbon precursor swings.

M&A and partnership prioritization: the competitive map and capability matrices identify attractive targets for bolt‑ons, equity partnerships or JVs across geographies and value chain layers.

Regulatory and safety compliance planning: the study decodes testing expectations and quality thresholds so product and legal teams can align testing programs and warranty strategies.

Bottom‑up market sizing and a transparent forecast methodology (2026–2032) with sensitivity cases for ±200bps demand shocks and material cost volatility.

Demand driver diagnostics: premiumization, e‑bike cross‑over effects, urban commuting trends and professional racing technology transfer into consumer segments.

Cost‑of‑goods sold (COGS) models and bill‑of‑materials (BOM) templates that link raw material prices, layup complexity and manufacturing yields to gross margin implications.

Supplier capability scorecards covering layup proficiency, tooling capacity, lead‑time reliability and quality certification mapping.

Regulatory and testing matrix: ISO 4210 implications plus comparative testing regimes (e.g., industry bodies with higher thresholds) and their commercial impacts on warranty, liability and brand perception.

Commercial playbooks: pricing ladders, channel mix scenarios (direct‑to‑consumer vs wholesale), and aftersales & spare‑parts strategies to protect lifetime value.

M&A and partnership models: valuation heuristics, integration risk checklists and example deal structures tailored to composite manufacturers and bike OEMs.

Implementation templates: a six‑quarter launch calendar for new carbon models, a supplier audit checklist, and an engineering hiring plan to scale composite competencies.

The long‑term picture is well defined: steady volume and value growth driven by premiumization, technical trickle‑down from racing to consumer products, and increased adoption of carbon across multiple bike categories. Our base‑to‑forecast path shows the market growing materially from 2020 through 2025 and continuing on to 2032, an affirmation that investments made now will have multi‑year payoff windows under the central case.

Raw material dynamics: standard modulus carbon fiber pricing in 2026 was observed in the mid‑teens USD per kilogram range—an important input for COGS scenarios and margin stress testing.

Retail and positioning: by 2025, entry‑level carbon road bikes from major brands had established retail price bands that set a new floor for premium entry offers—directly influencing go‑to‑market strategies for challengers and incumbents.

Regulation and testing: ISO 4210 remains the baseline safety standard for bicycle frames and forks; however, certain testing authorities employ more stringent protocols—our report shows how meeting higher test thresholds affects warranty exposure and brand positioning.

Market structure: the category is moderately fragmented — leading brands have visible advantages in brand equity and engineering, but no single group dominates the entire landscape; this opens opportunities for consolidation, technology partnerships and niche premium plays.

Our competitive analysis profiles global OEM leaders, high‑end artisans, D2C disruptors and vertically integrated Chinese manufacturers. Below are high‑level strategic positioning insights on the principal players covered in the full study (company profiles, product portfolios and URLs are available in the appendix of the complete report).

Global OEM powerhouses (e.g., established multinational OEMs): scale advantages in procurement, broad distribution networks and multi‑tier product ladders. Strategy: leverage scale to lock favorable resin and fiber contracts; invest in modular frame platforms to compress development cycles.

High‑end European artisans (racing pedigree brands): superior composite know‑how and strong brand premium. Strategy: protect IP and service premium through limited‑series launches, bespoke options and race‑team affiliations.

Direct‑to‑consumer specialists and lean European innovators: able to optimize margins by controlling channel and customer experience. Strategy: blend D2C efficiencies with experiential retail pop‑ups to scale brand loyalty while keeping unit economics attractive.

Chinese OEMs and component specialists: aggressive cost structures, rapid product cycles and increasingly sophisticated layup technologies. Strategy: consider strategic supply partnerships or minority stakes to secure flexible capacity and access to rapid prototyping.

Recent industry activity underscores these dynamics: manufacturers showcased new carbon frames and wheelsets at major trade events and launched ultra‑light production frames and compact full‑suspension models — signals that product innovation and manufacturing sophistication are accelerating across both established and emerging players.

Short‑term (0–12 months): prioritize supplier audits and establish multi‑sourcing for resin and fiber; launch a BOM rationalization to improve gross margins by targeting simple layup optimizations.

Medium‑term (12–36 months): invest in composite engineering capability (in‑house or via strategic JV), pilot integrated cockpit systems and aero optimizations that create defensible feature differentials.

Long‑term (36+ months): evaluate M&A for regional manufacturing footprint consolidation and capability acquisition; create aftermarket and service models to capture recurring revenue as frames become higher‑value assets.

Defensive plays: set price elasticity triggers and SKU rationalization rules to respond quickly to entry‑level price pressure; ensure product testing programs exceed minimal safety standards to reduce warranty risk.

This article demonstrates the kind of insight and practical orientation contained in the full PW Consulting study while preserving the commercial sensitivity of detailed segment numbers. The full report includes:

Comprehensive regional and application splits with downloadable tables and interactive charts for board presentation (kept out of this summary to protect strategic value).

Granular company profiles and capability maps, including primary web references and recommended engagement approaches per firm.

Actionable templates — supplier scorecards, COGS modeling spreadsheets, regulatory compliance checklist, and a six‑quarter product launch calendar ready for executive adoption.

Scenario simulators allowing you to stress test investment decisions under alternate material price and demand growth scenarios.

For executives making 2026 decisions, the carbon fiber bike category presents clear opportunities and definite operational risks. The market’s structural growth—reflected in our post‑2025 forecast and 6.98% CAGR central case—creates a window to capture premium value through disciplined supply‑chain management, targeted innovation investments and strategic partnerships. If your team needs the full dataset, segment‑level analytics, supplier rankings and executable templates to move from strategy to implementation, the complete PW Consulting report provides the necessary toolkit and the step‑by‑step playbooks to execute with confidence.

Access the full study to retrieve the proprietary segment breakdowns, detailed competitor scorecards and plug‑and‑play operational templates that will convert 2026 strategic intent into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Carbon Fiber Bike Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com