Near IR Camera Market: Strategic Preview for 2026 Decision-Making

As PW Consulting’s lead industry analyst, I present a high-level but strategically rigorous preview of our new Near IR Camera Market study — a compass for executives, product leaders, and corporate development teams preparing critical decisions in 2026. This brief demonstrates the report’s analytical depth and immediate operational value while preserving the granular segment-level findings for subscribers and licensing clients.

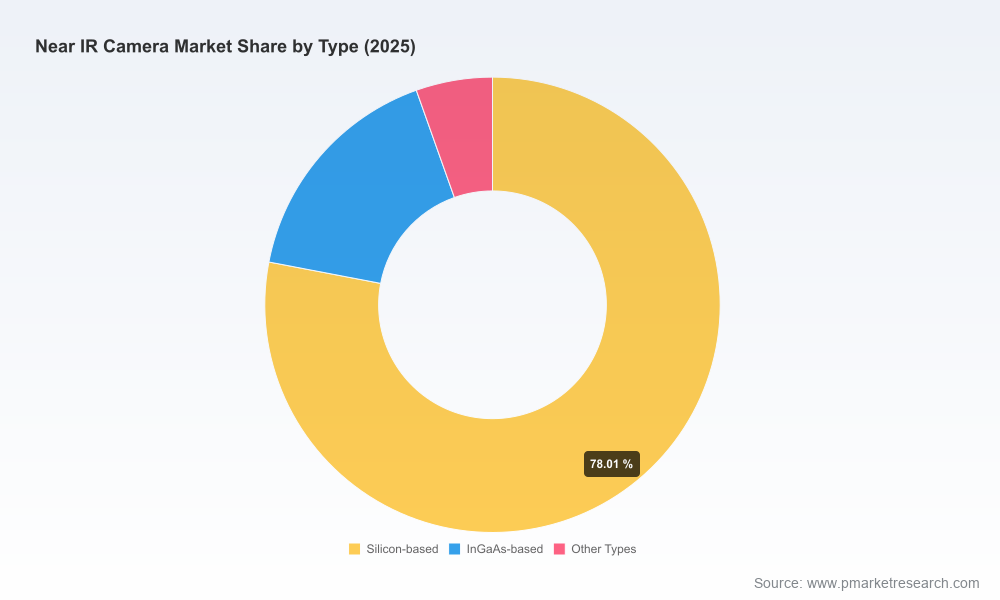

Near IR Camera Market

Market trajectory at a glance

The Near IR camera market has moved from an early-adopter phase into sustained commercial expansion. Measured in USD million, the market expanded from roughly USD 100.0 million in 2020 to USD 142.23 million in the base year 2025, reflecting accelerated adoption across medical, industrial, and defense adjacencies. Our forecast framework projects growth through the 2026–2032 horizon at a compound annual growth rate (CAGR) of 7.3%, culminating in an estimated market size of approximately USD 232.91 million by 2032.

Near IR Camera Market

These aggregate numbers capture an industry at the intersection of several secular trends: continued sensor innovation (broader SWIR band coverage and improved low-light sensitivity), expanding industrial automation use-cases, and rising demand for non-visible imaging in healthcare diagnostics and defense. They also mask significant micro-level variability — the precise mix by application, geography, and sensor type materially influences margin pools and go-to-market tactics for any participant. Our full report dissects those micro-variations with actionable models; this preview keeps the high-level context while guiding where to focus 2026 priorities.

Near IR Camera Market

Why 2026 is a pivotal planning year

- Capital allocation inflection: With the market well past early-prototype purchases, 2026 is the year companies choose between investment in differentiated optical/sensor IP versus supply-chain and volume-driven strategies. Mis-timed capital bets will either miss consolidation-driven scale benefits or lock firms into low-margin commoditization.

- Standards and safety convergence: Regulatory and standards compliance — from automotive functional safety to defense mil-spec demands — is shaping product roadmaps and procurement specifications. ISO 26262 and similar frameworks now factor into OEM selection criteria for ADAS/AV-related imaging solutions.

- Product portfolio turning points: The next 18–24 months will separate vendors that have demonstrable systems-level competence (cooling, integration, firmware, edge processing) from those selling component-level value only.

What the PW Consulting report contains (practical deliverables)

- Executive dashboards: single-page decision tools that translate market growth scenarios into revenue and margin sensitivities for different strategic options.

- Granular forecast models: bottom-up revenue models across applications, product types, and geographies (2020–2025 historicals; 2026–2032 forecasts) with drill-down capability for bespoke scenario analysis.

- Supplier scorecards: comparative assessments of technology maturity, manufacturing scale, and integration readiness, including supplier-specific SWOTs and procurement playbooks.

- Pricing and cost maps: end-to-end bill-of-material and cost-driver analysis identifying where component scarcity and specialization create asymmetric margins.

- Commercial playbooks: go-to-market strategies for OEMs, distributors, and new entrants (channel structures, bundling, service-led revenue models, and proof-of-concept templates).

- M&A and partnership thesis: prioritized acquisition targets and JV structures informed by capability gaps and market consolidation scenarios.

- Risk & resilience matrix: supply-chain stress tests, regulatory headwinds, and technology substitution pathways with mitigation actions and contingency budgets.

Competitive landscape — who matters and why

The Near IR and SWIR camera supplier ecosystem remains fragmented: the top-three firms account for roughly one-fifth of market revenue, while the top-five approach the mid-20s percentage range. This distribution signals a market with specialized niche leaders and significant opportunity for consolidation or strategic partnerships.

- Hamamatsu Photonics K.K. (Japan): Known for InGaAs camera offerings across scientific and machine-vision use-cases. Their strength is sensor-level expertise and trusted optics integration important for high-precision laboratory and medical customers.

- Xenics / Exosens (Belgium): Specialist in SWIR InGaAs detectors and cores targeting machine vision and inspection. Their modular detector approach supports OEM integration and tailored industrial solutions.

- Teledyne FLIR OEM (United States): Focused on SWIR/InGaAs modules for OEMs with an emphasis on reliability and automotive compliance. Their product strategy targets high-volume systems where functional-safety standards are critical.

- Raptor Photonics (UK/US): A focused developer of VIS-SWIR cameras with recent investments in extended SWIR technology and production scaling, indicating a push toward broader spectral coverage and higher throughput.

- Sensors Unlimited / Collins Aerospace (United States): Defense- and aerospace-oriented provider, notable for cameras optimized for operation through obscurants and harsh environments.

- Photonic Science (UK) and New Imaging Technologies (NIT / LYNRED, France): Both bring high-performance cooled and uncooled variants tailored to scientific imaging and high-speed industrial inspection respectively — strong options for customers prioritizing dynamic range and frame-rate.

Our competitive assessment evaluates each supplier on five dimensions: sensor technology roadmap, thermal management/cooling capability, software and edge-processing, manufacturing scale, and standards/regulatory readiness. The detailed vendor matrices in the full report provide procurement teams with score-weighted comparisons to fast-track vendor selection in 2026 RFPs.

Recent industry movements that change tactical plays

- Product introductions and platform extensions: Several vendors have launched extended SWIR offerings and updated models with Stirling cooling to enable broader wavelength sensitivity and lower dark current — a material performance uplift for long-range surveillance and certain industrial inspection tasks.

- Capacity and team expansions: At least one specialist supplier publicly expanded production capabilities in early 2026 to meet growing demand — a signal that industrial customers are shifting from trials to fleet deployments.

- Regulatory and standards alignment: OEM-focused modules now emphasize compliance with automotive functional-safety standards (e.g., ISO 26262) and MilSpec ratings for defense customers — influencing qualifying criteria in procurement processes.

- Price dispersion and cost drivers: SWIR InGaAs systems exhibit wide price variability driven primarily by sensor choice, cooling solutions, and integration complexity; buyers should expect a range from tens of thousands to multiple hundreds of thousands of USD for extended SWIR systems.

Commercial implications for 2026—what you should consider

- Buyers (OEMs & System Integrators): Re-evaluate RFP specifications to balance sensor performance against total cost of ownership. Prioritize vendors demonstrating systems-level integration (hardware + firmware + calibration) and lifecycle support.

- Component suppliers: Invest selectively in sensor IP or thermal management partnerships; commoditization risk is real where sensor differentiation is lacking.

- Investors & M&A teams: Target niche specialists with validated application wins or platform technologies that bridge multiple use-cases (medical, industrial, defense). Our report ranks acquisition targets by strategic fit and anticipated integration lift.

- New entrants: Focus on bundled solutions (imaging + analytics) or captive niches where domain knowledge (e.g., medical diagnostics protocols) establishes durable barriers to entry.

Decision framework — a three-step playbook for 2026

- 1. Rapid audit: Map your current product and procurement exposure to the report’s risk matrix. Identify two “must-fix” gaps that threaten near-term projects (e.g., lack of ISO 26262 compliance, insufficient thermal control for target wavelengths).

- 2. Option testing: Use the report’s vendor scorecards and cost maps to assemble a 12–18 month supplier test slate (1 incumbent, 1 challenger, 1 specialist). Budget for field trials that measure the full stack — optics, firmware, and processing latency.

- 3. Scale or niche bet: Decide whether to invest in scale (supply-chain, volume contracts, and manufacturing) or double-down on a niche with higher ASPs and customization (e.g., medical diagnostic imaging workflows). Our scenario models quantify the ROI breakpoints for each approach.

Closing — why PW Consulting’s report is timely

The Near IR camera market is moving from experimentation to industrialization. Aggregate statistics show attractive growth — roughly USD 142.23 million in 2025 growing to about USD 232.91 million by 2032 at a 7.3% CAGR — but the real value for executives lies in understanding where pockets of superior margin and strategic defensibility will form. This study synthesizes market sizing, supplier intelligence, regulatory dynamics, and tactical playbooks into deliverables you can act on immediately.

For organizations preparing 2026 budgets, procurement cycles, or strategic investments, the full PW Consulting Near IR Camera Market report provides the segmented forecasts, supplier financials, and downloadable models you need to convert insight into action. Contact our market research team to license the complete dataset and vendor matrices that underpin these strategic recommendations.

For detailed analysis of this topic, please visit the official page:Near IR Camera Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com