United States Ready-to-use Laboratory Test Kits Market Size and Projections 2034

Health |

2026-06-24 10:26:01

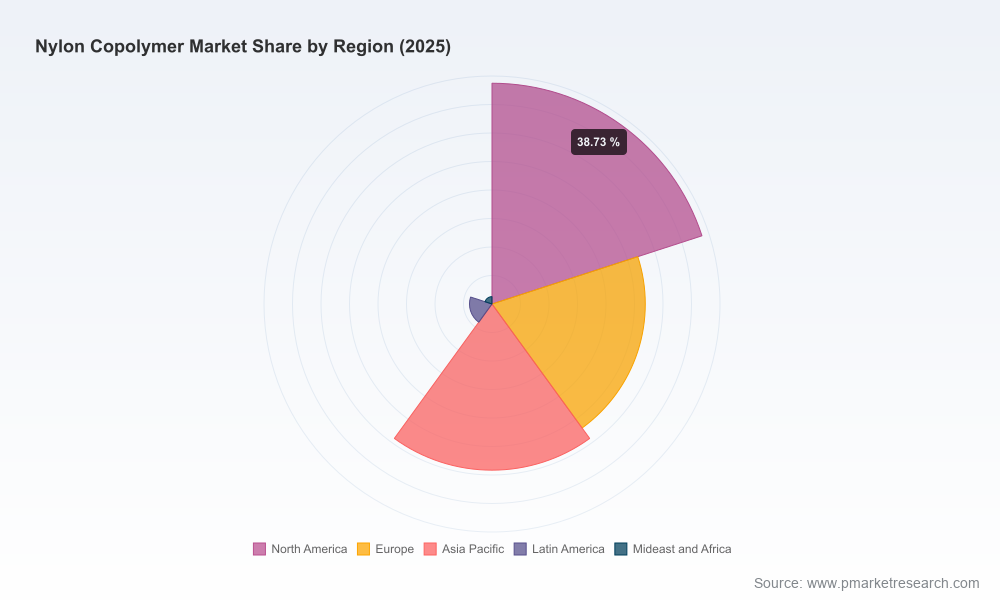

As 2026 becomes the operational horizon for many capital and procurement decisions, the global nylon copolymer market is transitioning from a recovery phase into a period defined by constrained upstream supply, selective capacity additions and targeted pricing actions. PW Consulting’s market model (base year 2025) shows the market measured in USD Million rising from roughly 287 in 2020 to about 309 in 2025, and our forward outlook projects a modest but resilient expansion to approximately 340 by 2032, implying a compound annual growth rate of 1.44% across the 2026–2032 forecast window. This steady, low-single-digit growth environment favors disciplined execution: firms that align product portfolio moves, sourcing strategies and CapEx to these structural dynamics will materially outperform peers.

Nylon Copolymer Market

Investment timing: With limited top-line growth but pronounced volatility in upstream feedstocks and selective capacity ramps, the difference between an accretive and dilutive investment in 2026 often hinges on granular timing and feedstock exposure. Our study identifies where demand is stable, where technical differentiation delivers margin, and where new capacity is likely to pressure realized prices.

Nylon Copolymer Market

Sourcing and contract strategy: Adipic acid and other nylon 66 feedstocks have re-emerged as primary cost levers. Procurement teams that adopt multi-scenario hedging, long-term offtake and regional diversification will reduce margin erosion from sudden feedstock shocks.

Nylon Copolymer Market

Product and go-to-market prioritization: Technical grades (high-temperature nylons, long-chain copolymers and flame-retardant HTN variants) command strategic value where metal replacement, weight reduction and thermal stability are non-negotiable. The report maps near-term white spaces where application-specific innovation yields the quickest ROI.

The headline—a global market of roughly 309 USD Million in 2025 and growing at a 1.44% CAGR thereafter—masks a market with differentiated pockets of strength and softness. Overall demand growth is modest, but not uniform: application-specific performance and raw-material cycles create opportunities for selective premiumization. Importantly, concentration metrics show that the top three players control about 60% of market share, and the top five around 65%, indicating a market where scale, technical portfolios and integrated value chains materially affect competitive dynamics.

Upstream feedstock pressure: Adipic acid pricing has become a systemic risk driver in 2026. Regional benchmarks recorded substantial upward moves in early 2026, driven by inflation in cyclohexane and nitric acid, and a renewed restocking cycle for nylon 66. Producers such as LANXESS signaled price adjustments to reflect these cost realities. For manufacturers and converters, the pass-through cadence for these moves will be a core margin management challenge in 2026.

Capacity additions are selective and strategic, not pervasive: New upstream projects that came online in early 2026 (for example, large adiponitrile capacity) are meaningful for feedstock security and cost structure for integrated producers, but downstream polymer capacity remains disciplined. Where expansions occur—often in specialty long-chain nylons—the commercial focus is on premium applications rather than volume displacement.

Regulatory changes: Recent European measures aimed at upstream material production and authorization create a dual effect—short-term implementation uncertainty and medium-term incentives for reshoring or verified local supply. Companies with regulatory-readiness programs will preserve speed-to-market advantages for modified grades and recycled-content offerings.

The market is shaped by a concentrated set of global players with differentiated technical arsenals. Firms that marry advanced polymer technology, global logistics and application engineering hold outsized influence over pricing and specification trends.

Celanese Corporation — Leader in engineered materials with a focused portfolio of high-temperature, flame-retardant HTN grades. Their emphasis on performance nylons for demanding thermal and safety applications makes them a natural supplier to OEMs pursuing weight and performance trade-offs. Recent price moves underscore how integrated players manage cost inflation across value chains.

DuPont de Nemours — A longstanding producer of broad PA6/66 families with deep penetration in automotive and electrical markets. Their mix of amorphous and crystalline grades offers customers specification breadth and scale; such breadth is an advantage when customers seek single-supplier simplification and validated qualifications.

BASF SE — Positioned as both a materials innovator and large-scale supplier, their mid- to high-performance Ultramid offerings are optimized for injection molding and extrusion. BASF’s depth in application engineering becomes a differentiator where replacement of metal parts or integration of multi-material assemblies is required.

EMS-GRIVORY — A premium specialist with a clear play on metal replacement and high-performance alloying. Their portfolio is well-suited to customers willing to pay for mechanical performance and thermal endurance, particularly in automotive and medical niches where specification cycles are longer but margins are higher.

Nylon Corporation of America (NYCOA) — A specialist in long-chain copolymers and amorphous high-performance nylons. Recent capacity additions at their Manchester facility signal an intent to scale specialty, long-chain grades—an important development for customers targeting reduced moisture uptake and enhanced dimensional stability.

Feedstock price volatility and supplier price notices have increased commercial friction in the value chain; several manufacturers announced price adjustments in response to supply chain and raw material inflation.

Targeted capacity expansions—particularly in long-chain nylon copolymers and upstream adiponitrile—are improving feedstock availability for vertically integrated producers, while leaving conversion capacity tight for standard commodity grades.

Regulatory shifts in Europe and evolving upstream production authorizations are influencing regional sourcing strategies and accelerating qualification of alternative feedstocks and recycled content.

Re-evaluate contracting models: Move from purely spot-led purchases to a hybrid of hedged, indexed, and fixed-price contracts aligned to product margins. Include clauses that address feedstock pass-throughs and force majeure to reduce downside in volatile months.

Prioritize product segmentation and value capture: Identify where technical copolymers (HTN, long-chain nylons) can be premiumized for higher margin pockets—this typically delivers better returns than volume plays in a slow-growth market.

Consider selective vertical integration or strategic partnerships for feedstock access: Recent adiponitrile project starts illustrate the advantage enjoyed by players with secured upstream supply, whether through ownership, long-term offtakes or joint ventures.

Accelerate regulatory and sustainability readiness: Build capability to validate recycled content, substitute restricted chemistries and meet evolving regional compliance. Early movers will capture the preferred supplier slots for OEMs under stricter ESG and regulatory regimes.

Invest in application engineering and qualification pipelines: Because the market is concentrated, winning long-term business often means investing where customers evaluate material changes—automotive and electronics OEMs will pay for proven, low-risk transitions.

Independent market sizing and a transparent model covering historical performance (2020–2025) and a scenario-driven forecast for 2026–2032, including sensitivity to feedstock price swings and demand shocks.

A practical playbook for procurement, supply planning and product strategy that aligns to four commercial archetypes: integrated producers, specialty players, large converters and regional independents.

Comprehensive competitive profiles and an M&A watchlist with risk-adjusted valuation guidance for assets that unlock feedstock security or technical differentiation.

Raw-material mapping and price-impact scenarios—including case studies that quantify margin erosion at different adipic acid and adiponitrile price points—and a timeline to stress-test your contracts and inventory policies.

A regulation-and-sustainability annex that translates emerging rules into compliance Checklists and product roadmaps to preserve market access.

The nylon copolymer market in 2026 is not a market of dramatic expansion; it is a market of careful choices. The headline growth rate belies a battleground of feedstock cost management, selective capacity deployment, and product differentiation. For leadership teams that must allocate CapEx, negotiate multi-year supply agreements, or choose acquisition targets, the value lies in executional clarity: marry technical product strategy with supply security and regulatory foresight.

PW Consulting’s full report provides the quantitative segment matrices, interactive models and supplier scorecards required to turn these strategic priorities into executable plans. For organizations preparing 2026 budgets and three- to five-year roadmaps, this research functions as both a risk map and an action checklist—helping leaders convert modest market growth into outsized commercial returns. Visit our report page or contact PW Consulting to request the complete dataset and tailored advisory options.

For detailed analysis of this topic, please visit the official page:Nylon Copolymer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com