Laser Skincare Treatments Create Luminous Beauty Joy

Health |

2026-06-12 06:44:29

As PW Consulting’s Lead Industry Analyst, I present a concise, decision-oriented primer on the global pet food packaging market designed to inform strategic choices in 2026. Built on a base year of 2025 and a historical view covering 2020–2025, our analysis projects the market through the 2026–2032 forecast window. At the macro level the market grew from approximately USD 8.5 billion in 2020 to roughly USD 12.3 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.7% through the forecast period, reaching an estimated USD 18.0 billion by 2032. Market concentration is moderate: the top three players account for roughly 37% of value, with the top five near 47%—a structure that favors both scale players and well-capitalized challengers pursuing premium or niche plays.

Pet Food Packaging Market

Regulatory inflection points: Major legislative shifts—most notably the EU’s Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025 and becomes generally applicable from 12 August 2026—introduce eco-modulated Extended Producer Responsibility (EPR) frameworks and recyclability mandates that materially change total cost of ownership for packaging choices.

Pet Food Packaging Market

Market momentum and scale: After steady expansion through 2025, the market is entering a phase where incremental growth will be powered by premiumization, e-commerce adoption, and reformulation of packaging systems to meet sustainability constraints without sacrificing barrier performance.

Pet Food Packaging Market

Value migration opportunities: Shifts in raw material economics (paper, paperboard, metal, and plastic resins) and downstream recycling capacity create windows for cost-effective material substitution, circular-design pilots, and differential EPR fee optimization for brands that act quickly.

Decisions made in 2026 will determine competitive positioning for the rest of the decade. Leadership teams should prioritize three near-term workstreams that our full report operationalizes in depth:

Product portfolio and packaging architecture rationalization—Identify which SKUs to migrate to mono-material, recyclable, or compostable formats and which to retain on high-barrier multi-layer structures (with a plan for targeted circularity pilots where recycling infrastructure lags).

Regulatory cost modelling and EPR mitigation—Map the P&L impact of regional EPR regimes (including the EU’s PPWR timeline and the growing patchwork of U.S. state EPR laws) and quantify the trade-offs between lower EPR fees for recyclable formats versus any up-front tooling or material costs.

Supply chain & sourcing resilience—Stress-test supplier networks for resin and recycled-content supply, and build tiered sourcing strategies to isolate margin exposure in the event of raw material inflation or export restrictions.

EU PPWR (effective 12 August 2026): The new regulation raises the bar on recyclability requirements and links EPR fees to performance. Brands that pre-emptively redesign packaging to meet eco-modulation criteria will enjoy lower lifecycle fees and faster time-to-market for compliant SKUs.

U.S. EPR patchwork: As of late 2025/early 2026, seven U.S. states have enacted comprehensive packaging EPR laws and more are considering bills. This creates a mosaic of compliance obligations that favors companies capable of harmonizing packaging specifications across multiple jurisdictions or localizing volumes strategically.

Raw material dynamics: Paper, paperboard, metal, and plastic resin prices remain primary cost drivers. Shifts toward mono-materials and recycled-content targets will reshape supplier negotiations and capital allocation for conversion equipment and recycling partnerships.

The sector is anchored by global converters and materials groups that combine scale with innovation pipelines. Key strategic profiles we track include:

Amcor plc (Zurich) — A leader in recycle-ready flexible formats with product families tailored for wet and dry pet food needs. Their emphasis on heat-sealable, barrier-capable solutions provides a useful yardstick for balancing recyclability with performance.

Huhtamaki Oyj (Espoo) — Focused on mono-material and alu-free designs, Huhtamaki’s blueloop portfolio demonstrates how cinema-grade sustainability claims can be operationalized for mass-market pet food segments.

UFlex Limited (New Delhi) — An example of scale-oriented, cost-competitive manufacturing that is actively showcasing recyclable formats across global trade platforms. Their product breadth highlights the commercial viability of recyclable and refill formats for emerging markets.

Mondi plc (Vienna) — Notable for recent mono-material launches with brand partners, demonstrating that replacement of non-recyclable multi-material bags for dry pet food is technically feasible while retaining barrier performance.

Silgan Holdings Inc. (Norwalk) — A significant provider of metal cans and dispensing closures tailored to pet food, underscoring the continued relevance of metal formats in certain wet food and premium dispensing use cases.

Recent market moves—such as Mondi’s mono-material launch with a dry-pet-food brand in mid‑2025 and UFlex’s product showcases at industry events in 2026—underline a dual pathway strategy among incumbents: sustain premium barrier solutions for wet and high-moisture products while accelerating recyclable, mono-material solutions for dry and snack formats.

Recyclability-first reformulation: Brands that prioritize mono-material conversion for high-volume SKUs will benefit from lower EPR exposure in regulated markets and better alignment with retailer sustainability criteria.

Premium barrier plays: For wet pet food and long-shelf-life products, high-barrier flexible or metal formats will retain a role—opportunities exist to optimize these formats for recyclability (e.g., recyclable liners, easy-separate components) rather than abandon them altogether.

Refill and portion-pack innovation: Urbanization and e-commerce trends favor reclosable pouches, spouted formats, and multi-serve portioning, enabling higher per-unit revenues if paired with a sustainability narrative.

Localized circular partnerships: Commercial pilots that secure feedstock for recycled-content claims (PCR) close the loop and reduce exposure to resin volatility; such partnerships are becoming a differentiator for brand owners in markets with stringent EPR regimes.

M&A and strategic sourcing: Given moderate market concentration, targeted bolt-on acquisitions in regional converting, recycling, or specialty barrier technologies can deliver rapid capability gains and margin expansion.

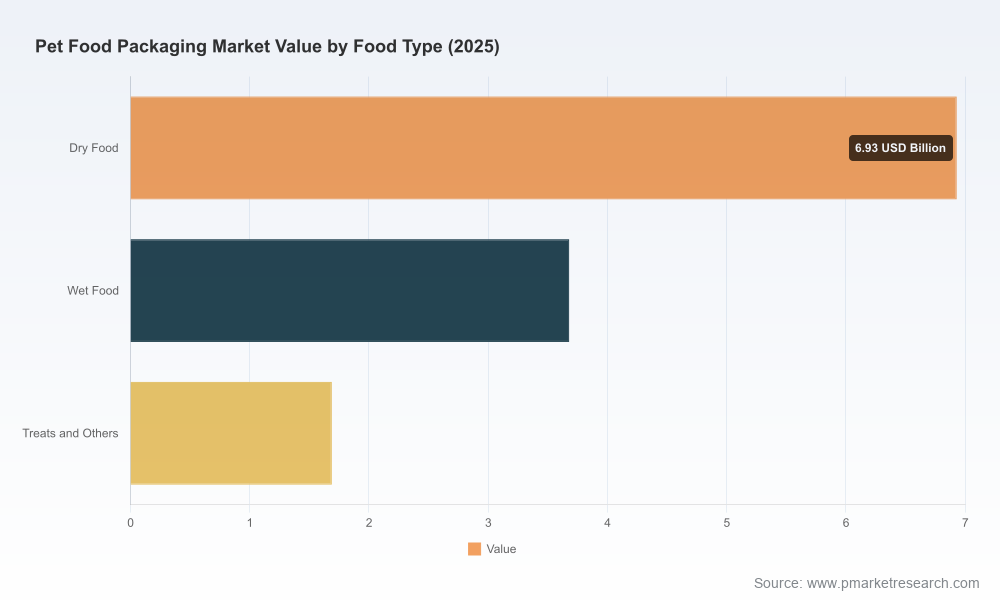

Granular demand-models by packaging format, material, and food type (note: the executive primer intentionally omits the granular splits; these are available in the full dataset).

Scenario-run P&L templates that quantify the impact of packaging redesign on COGS, EPR fees and shelf-availability under alternative regulatory timelines.

Supplier scorecards and due-diligence frameworks for selecting converters and recyclers by capability, geography, and transition-readiness.

Playbooks for piloting mono-material transitions, including supplier engagement scripts, packaging validation matrices, and retailer acceptance criteria.

An M&A target shortlist methodology calibrated to CR3/CR5 dynamics, capex needs, and integration risk profiles.

Start by prioritizing decisions that lock in advantage while remaining reversible. Examples:

Implement a two-track packaging strategy: certify a group of high-volume SKUs for recyclable mono-material formats within 12–18 months while maintaining premium barrier platforms for wet/long-dated products with a parallel R&D track for recyclable alternatives.

Run EPR sensitivity analyses for the markets where you have the largest exposure and negotiate supplier contracts that include shared responsibility mechanisms for recycled content availability and price volatility.

Design a measurable circularity pilot with a recycler or converter partner that includes PCR commitments and a path to scale if economics prove out.

2026 is less a year of gradual change than a turning point: regulatory deadlines, evolving consumer expectations, and supplier innovation are converging to rewrite the economics of pet food packaging. PW Consulting’s research synthesizes market-scale projections (historical and forecast), competitive diagnostics, regulatory impact modelling, and plug‑and‑play commercial tools that expedite decision-making. We deliberately frame this primer to demonstrate the analytical depth you will need while reserving the underlying granular segmentation and financial templates for the full report—where the real operational levers live.

If your team needs a short briefing tailored to your portfolio (20–60 minutes), we can map the report’s scenarios to your SKU architecture and produce an implementation roadmap with estimated capex and timing.

Contact PW Consulting to request the complete dataset, including the detailed segmentation splits, supplier scorecards, and the P&L templates required to execute the 2026 playbooks.

For detailed analysis of this topic, please visit the official page:Pet Food Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com