Micro Turbine Market 2026: Strategic Preview for Corporate Decision‑Makers

Executive preview

As energy transition priorities, distributed generation mandates, and cost‑performance improvements converge, the micro turbine market is entering a phase of sustained commercial maturation. Our PW Consulting market model—anchored on a 2025 base year—estimates a global market of approximately USD 215 Million in 2025, rising at a compound annual growth rate (CAGR) of roughly 9.44% through the forecast horizon. By 2026 the market crosses the mid‑hundreds mark and the trajectory points to a near‑doubling of scale by the early 2030s. This brief distils the strategic implications for corporate leaders who must make investment, product, and go‑to‑market choices in 2026.

Micro Turbine Market

Why this study matters for 2026 decisions

- Timing: 2026 will be the first full planning year after several major policy clarifications and incentive resets that materially affect project economics for distributed generation assets.

- Scale inflection: Our forecast shows that the market is not only growing but shifting in buyer composition and use cases — creating windows for early movers to capture premium margins.

- Competitive posture: With market concentration relatively low (CR3 ~24.6%, CR5 ~26.2%), the sector remains fragmented — an advantageous environment for targeted consolidation, partnerships, and differentiated service models.

Data‑driven market trajectory (what the numbers tell you)

Historical performance underscores recoveries and step‑changes: the market expanded steadily from the early 2020s up to the 2025 base. Our forecast assumes continued demand for onsite generation and CHP solutions supported by decarbonization incentives, fuel flexibility advances (notably hydrogen blends and biogas), and cost declines through manufacturing learning curves and longer component life. The model projects year‑on‑year expansion from the 2025 baseline consistent with the cited CAGR, producing meaningful addressable‑market increases by the end of the decade.

Micro Turbine Market

Key market dynamics shaping 2026 strategy

- Policy and incentives: Tax credits and investment incentives are a primary driver of near‑term procurement economics. Examples include per‑capacity credits for fuel cell and micro‑generation technologies and provisions in major acts that enable a 30% Investment Tax Credit for qualifying systems under 1 MW—subject to prevailing wage and other eligibility rules. Several jurisdictions have also restructured eligibility criteria and phase‑out timetables, which will change project return profiles depending on construction start dates.

- CapEx and project economics: Installed capital costs for microturbine CHP systems vary by scale and configuration; recent benchmarking places typical installed costs in a band that materially affects payback trajectories for commercial and industrial buyers. Engineering for heat recovery, fuel procurement, and system integration now dominates the incremental value equation.

- Fuel and decarbonization pathways: The technology’s ability to operate on diverse fuel streams—natural gas, biogas, RNG, landfill gas, and hydrogen‑blends—creates differentiated value propositions across use cases (CHP, standby, waste‑heat recovery). This fuel flexibility is a near‑term competitive differentiator as hydrogen blending and biogas feedstock availability expand.

- Use‑case evolution: From telecom backup and remote/off‑grid power to industrial CHP and municipal projects, adoption patterns are broadening. Customers increasingly demand turnkey solutions that combine equipment, controls, and long‑term service contracts.

Competitive landscape — what incumbents are doing (and why it matters)

The market is characterized by a mix of specialist OEMs, system integrators, and niche technology providers. Key commercial archetypes include: agile small‑unit OEMs targeting telecom and bad‑grid power; mid‑range suppliers focused on CHP packages for commercial and industrial customers; and diversified turbomachinery groups offering higher‑power modules and hydrogen‑tolerant systems.

Micro Turbine Market

- Ansaldo Energia S.p.A. (Genoa, Italy) is positioning with mid‑range microturbines engineered for CHP/CCHP and multi‑fuel operation including high hydrogen blends. Their product focus and efficiency claims make them a contender for institutional and industrial CHP bids where fuel flexibility is a requirement.

- Capstone Green Energy Corporation (Van Nuys, California) has been the most visible commercial performer in recent months, securing multiple orders across food manufacturing and institutional CHP applications. Repeat orders and multi‑MW projects demonstrate a strong service and ref‑sell dynamic — a commercial model worth emulating for scale players.

- Bladon Micro Turbine (Warwick, UK) is concentrated on smaller gensets optimized for telecom and extreme reliability use cases, leveraging fuel options like diesel, kerosene and HVO to serve off‑grid and “bad grid” customers.

- FlexEnergy Solutions (Centennial, Colorado) and similar suppliers are addressing larger off‑grid and grid‑parallel applications with natural gas microturbines, while others like Turtle Turbines (India) and Advanced Microturbines Srl (Italy) focus on waste‑heat recovery and decompression energy recovery respectively — signaling niche opportunities in industrial process sectors.

- pyropower GmbH (Germany) exemplifies the convergence of microturbines with thermal processing (e.g., pyrolysis CHP), highlighting alternative feedstock pathways for decentralized energy projects.

Strategically, these profiles show two actionable trends: incumbents with strong service and project execution capabilities capture disproportionate lifetime value; and technology differentiation (hydrogen tolerance, air‑bearing systems, low‑maintenance architectures) remains a defensible barrier against low‑cost incumbents.

Regulatory and financing landscape — practical implications

- Incentive timing matters: Several credit lines and phase‑outs have precise cutoffs tied to construction start or commissioning dates. Corporate procurement officers must align capex schedules to maximize ITC/PTC capture where applicable.

- Prevailing wage and domestic content: Qualification for higher credit rates often depends on labor and content rules. Project developers should integrate compliance pathways into early procurement and contracting documents to avoid retroactive ineligibility.

- Project structure: Given the modest absolute ticket size of many microturbine projects, creative financing (pooled portfolios, performance contracts, ESAs) can unlock deals that would otherwise be capital‑constrained.

What our report contains — practical, operational, buy‑side intelligence

The full PW Consulting report goes beyond market topline growth. Highlights include:

- Actionable buyer personas and procurement decision maps for commercial, industrial, municipal, and telecom customers.

- Investment due diligence checklists tailored to microturbine projects (technical, fuel‑supply, regulatory, O&M, and decommissioning risks).

- Segment economics and payback sensitivity models that incorporate current capex bands, fuel price scenarios, and incentive structures.

- Competitive benchmarking across performance, fuel flexibility, service networks, and total cost of ownership—presented in an anonymized comparator matrix to preserve commercial confidentiality while enabling side‑by‑side evaluation.

- A transaction playbook for corporate strategy teams: bolt‑on M&A targets, JV structures for distributed energy service providers, and go‑to‑market models for rapid deployment.

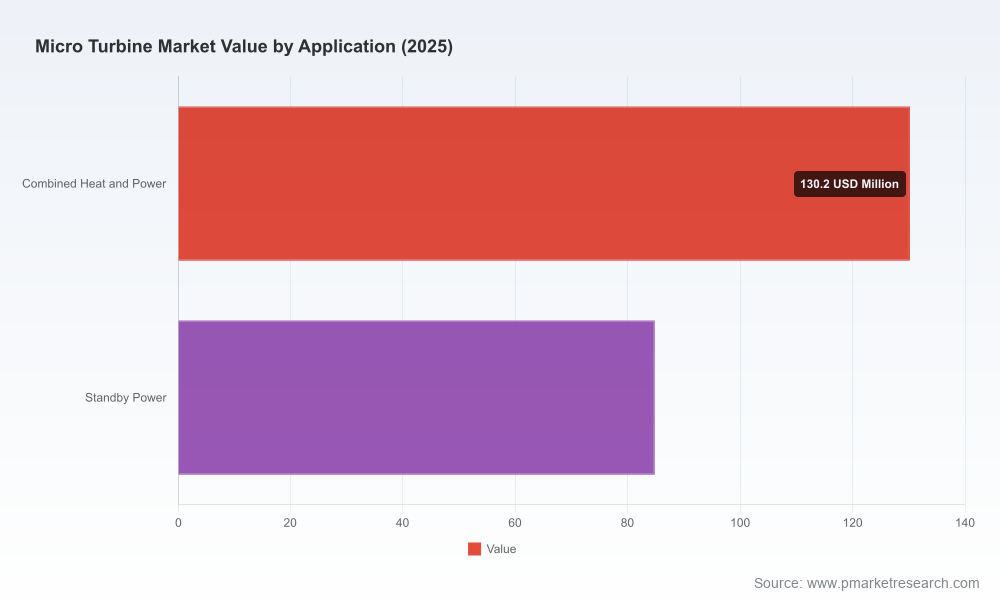

Note: this public preview intentionally omits detailed segment numbers and geography‑level splits. The full report includes granular segmentation, revenue models, and downloadable financial templates for buyers and suppliers.

2026 strategic recommendations — immediate actions for senior leaders

- Audit near‑term projects for incentive eligibility: align procurement and construction start dates to maximize available ITC/PTC benefits and avoid phase‑out traps.

- Prioritize fuel‑flexible architectures: product roadmaps and procurement specifications should require hydrogen‑blend capability and biogas compatibility where practical.

- Bundle hardware and service: design contracts that monetize long‑tail service revenue—warranties, remote monitoring, and parts consignment materially improve lifetime margins.

- Evaluate financing pools: aggregate smaller projects into portfolio finance vehicles to lower capital costs and accelerate deployment.

- Pursue selective partnerships: target waste‑heat recovery integrators, CHP contractors, and telco infrastructure providers to access non‑traditional adoption channels.

- Monitor competitor orderbooks: recent multi‑MW orders by leading OEMs signal where channel momentum is building—use those signals to prioritize sales coverage and inventory planning.

Why PW Consulting’s microturbine study is strategically different

Our analysis blends macro market modelling with transaction‑level playbooks. We combine proprietary demand models, incentive rule‑sets, and a vendor capability assessment to produce not just forecasts, but executable strategies for procurement, product development, and corporate development teams planning for 2026 and beyond. We explicitly model regulatory sensitivities and provide customizable Excel models so executives can simulate their portfolio outcomes under alternative policy and fuel‑price scenarios.

Next steps

If you are building a procurement pipeline, defining a product roadmap, or evaluating M&A targets in distributed energy for 2026, the window for strategic advantage is open but narrowing. Our public preview above highlights the major directional forces; the full PW Consulting Micro Turbine Market report contains the granular segmentation, company scorecards, and downloadable financial templates required to translate insight into action. Contact our research team or visit our report page to access the complete dataset, scenario workbooks, and the executive briefing tailored to your organization’s risk and growth profile.

For detailed analysis of this topic, please visit the official page:Micro Turbine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com