Patient Infotainment Terminal Market — Strategic Briefing for 2026 Decisions

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a high-resolution, action-oriented briefing on the Patient Infotainment Terminal market. This “trailer” is designed to surface the analytic scaffolding, directional imperatives, and investment-grade implications you will need to make decisive moves in 2026 — while preserving the granular tables and proprietary segment detail for our full report.

Patient Infotainment Terminal Market

Why this market matters in 2026

Patient infotainment terminals have moved from a hospitality adjunct to a core node in the digitalized care experience. Between 2020 and 2025 the market expanded from approximately USD 197.3 Million to USD 271.7 Million (base year 2025). Our forecast through 2032 projects a sustained expansion (forecast period 2026–2032) to around USD 479.4 Million, reflecting a compound annual growth rate of approximately 8.5%. That trajectory signals durable, investment-worthy demand driven by clinical integration, patient engagement initiatives, and incremental service revenue opportunities for healthcare providers and vendors alike.

Patient Infotainment Terminal Market

What this growth means for corporate decision-makers

- Portfolio Prioritization: An 8–9% CAGR across the forecast window justifies prioritized investment in modular, certifiable products that reduce integration friction with Electronic Health Records (EHRs) and clinical workflows.

- Scaling Services vs. Hardware: Growth is not purely hardware-driven — meaningful upside comes from managed services, software licensing, content partnerships, and lifecycle support. Providers should evaluate margin profiles across hardware, software, and services when sizing go-to-market plays.

- Competitive Positioning: Market concentration metrics indicate that a relatively small group of incumbents capture the majority of value. This raises acquisition and partnership opportunities for mid-sized vendors looking to scale distribution quickly or to access certification pipelines.

What the full PW Consulting report delivers (practical, operational intelligence)

Our full study is structured to move leaders from insight to execution. Highlights include:

Patient Infotainment Terminal Market

- Market sizing and scenario-based forecasts (2026–2032) rooted in demand drivers, procurement cycles, and hospital replacement cadences.

- Competitive scorecards and vendor capability matrices that assess certifications, clinical integrations, security posture, manufacturing scale, and service ecosystems.

- Commercial playbooks: go-to-market segmentation, pricing archetypes, channel models, and contracting templates tailored for health systems, long-term care operators, and ambulatory networks.

- Procurement and implementation toolkits: total cost of ownership (TCO) models, integration checklists for EHR and telemedicine stacks, cybersecurity & privacy compliance maps, and on-premises vs. cloud deployment decision trees.

- Regulatory and reimbursement intelligence: mapping of certification requirements, validation timelines, and payer attitudes that influence uptake and purchase cadence.

- M&A and partnership analysis: target screens, synergy estimates, and valuation heuristics for strategic acquirers and financial sponsors.

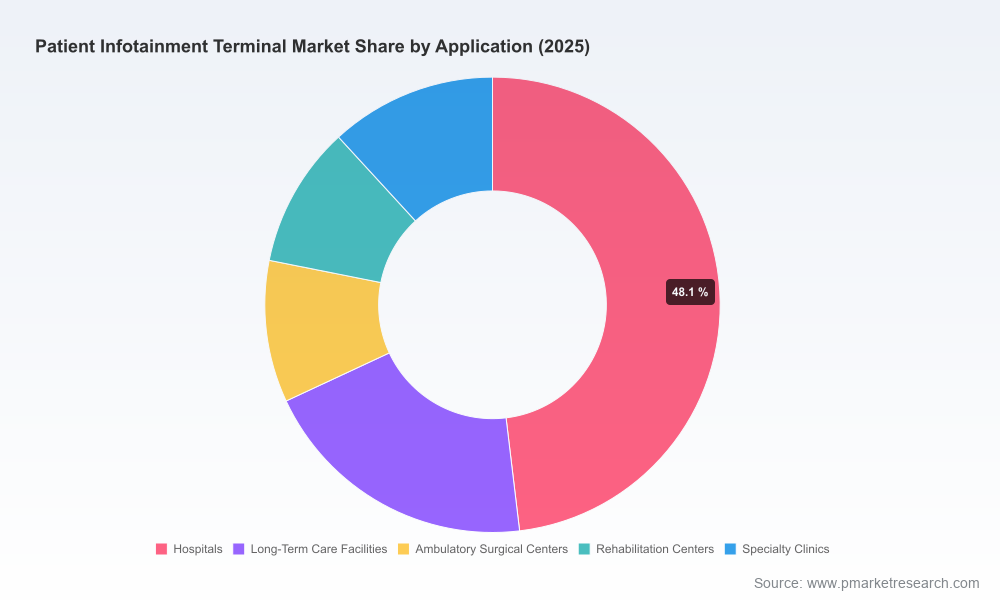

Note: this briefing intentionally omits the granular regional, product and application breakout tables that drive many tactical decisions; those are available in the full report.

Competitive landscape — who to watch and why

The market is concentrated among a set of firms with established healthcare channel access, regulatory certifications, and integration footprints. Top-tier vendors combine medical-grade hardware design, robust service models, and clinical integration capabilities.

- BEWATEC (Germany) — Known for the VITOS 5000 bedside series and ConnectedCare ecosystem. Strength: integrated scheduling, medication and treatment-plan workflows embedded into bedside endpoints. Strategic implication: strong candidate for partnerships focused on clinical workflow embedding and device-as-a-service models.

- Onyx Healthcare Inc. (Taiwan) — Emphasizes medical-grade compliance (UL/ANSI/IEC 60601-1 suite) and mobile nursing/telemedicine integration. Strength: certification-first engineering that lowers adoption friction in regulated hospitals. Strategic implication: critical partner for customers prioritizing compliance and certified manufacturing.

- PDi Communication Systems (USA) — Deep compatibility with major EHR ecosystems (e.g., Epic MyChart Bedside). Strength: software and content integration expertise. Strategic implication: attractive for health systems seeking turnkey integration with existing digital front-ends.

- ClinicAll (Canada) — Focused on integrated hospital platforms delivering entertainment, communication, and education. Strength: platform-centric approach facilitating bundled services. Strategic implication: platform play attractive for service-led monetization.

- Teguar (USA) — Offers ruggedized, MIL-STD qualified medical computers with capacitive touch capability. Strength: durability and industrial design for high-utilization environments. Strategic implication: suitable for high-acuity, high-turnover settings.

- Advantech (Taiwan) — Medical-grade units with antimicrobial housings; recent Android Enterprise Recommended certification on AIM-68H. Strength: strong device management and security posture. Strategic implication: enterprise IT-friendly vendor for large-scale rollouts.

- Barco NV (Belgium) — Differentiates via advanced visualization (glasses-free 3D) and clinical-grade displays. Strength: unique visualization IP that can extend into specialty clinical uses. Strategic implication: horizontal expansion into clinical imaging and patient education.

- Lincor Solutions (Canada) — Integrated EHR connectivity and patient engagement platforms. Strength: established software stack for patient services. Strategic implication: attractive for system-level digital transformation initiatives.

- Saintwaytech & Hitekon (China) — Offer competitively priced, medical-grade bedside terminals with antimicrobial touchscreens and Android/Linux stacks. Strength: cost-efficient hardware and rapid customization. Strategic implication: supply chain/contract manufacturing partners for cost-sensitive deployments.

Recent vendor developments underscore two themes: certification-led differentiation (e.g., Advantech’s Android Enterprise Recommended) and consolidation/extensions of product portfolios (e.g., BEWATEC’s expanded VITOS deployments following corporate acquisition activity). These moves compress time-to-deployment risk for buyers but intensify competitive pressure for independent vendors.

Regulatory, reimbursement, and cost dynamics — the growth restraints and accelerants

- Regulatory burden: Compliance with medical-device standards (UL, ANSI/AAMI, IEC 60601-1) and, where applicable, FDA manufacturing expectations increase development time and validation expense. This raises the bar for new entrants but creates differentiation opportunities for certified incumbents.

- Data privacy & security: Hospitals now require device-level security, centralized patching, and device management. Vendors that can demonstrate enterprise-grade update lifecycles and privacy controls will enjoy procurement preference.

- Reimbursement gap: Limited reimbursement pathways for non-clinical digital tools slow adoption in publicly reimbursed systems; value propositions that tie infotainment to clinical outcomes or revenue (e.g., telemedicine billable visits, throughput gains) will accelerate procurement.

- Material & implementation cost pressure: Rising hardware, licensing, and integration expenses mean buyers prioritize modularity and lifecycle economics. Vendors that offer flexible financing, managed services, or SaaS bundles can capture more share.

Strategic imperatives for 2026

- Prioritize certification and lifecycle management. Certification investments improve win rates in regulated health systems and can shorten sales cycles.

- Design for clinical integration, not just entertainment. Roadmaps that emphasize EHR hooks, medication/treatment-plan displays, and telemedicine-native features unlock procurement budgets tied to clinical improvement initiatives.

- Shift to service-led economics. Hardware margins are compressing; wrap managed services, content distribution, and analytics into bundled offerings to improve lifetime value.

- Mitigate reimbursement risk through value quantification. Build ROI case studies showing reduced length-of-stay, improved patient satisfaction scores (HCAHPS/NPS equivalents), or revenue capture from telehealth to influence purchasers and payers.

- Accelerate channel and alliance strategies. For vendors without global footprints, partnerships with certified manufacturers or established integrators can accelerate market entry while controlling CAPEX.

- Explore consolidation where scale matters. Given industry concentration, M&A can be the most efficient route to access global channels, regulatory certifications, and enterprise IT relationships.

How PW Consulting helps

Our full report operationalizes these imperatives with vendor scorecards, integration playbooks, buyer procurement templates, and three modeled go-to-market strategies calibrated for OEMs, integrators, and health systems. It also includes a curated M&A target list and a scenario engine for stress-testing adoption under alternative reimbursement and regulatory trajectories.

This briefing intentionally omits the granular regional, product and application splits — the precise sub-segment tables, pricing ladders, and customer-level adoption curves are available in the full PW Consulting Patient Infotainment Terminal Market report. That detailed intelligence is where tactical planning, RFP construction, and M&A valuation work should begin.

Next steps

- Request the full report to access the proprietary sub-segmentation matrices, vendor benchmarking sheets, and the TCO calculator necessary for RFP development and capital planning for 2026.

- Schedule a strategy session with PW Consulting to translate market scenarios into a 12–24 month product and commercial plan tailored to your role — OEM, integrator, payer, or provider.

In a market expanding at roughly 8.5% annually and approaching half a billion dollars by 2032, early 2026 is a decision point: invest in certification and integration capabilities now, or expect to buy them later at a premium. PW Consulting’s full study provides the granular maps and executable playbooks to ensure you choose deliberately.

For detailed analysis of this topic, please visit the official page:Patient Infotainment Terminal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com