Rhinoplasty Planning: How Anatomy Guides the Operation

Health |

2026-06-20 09:31:45

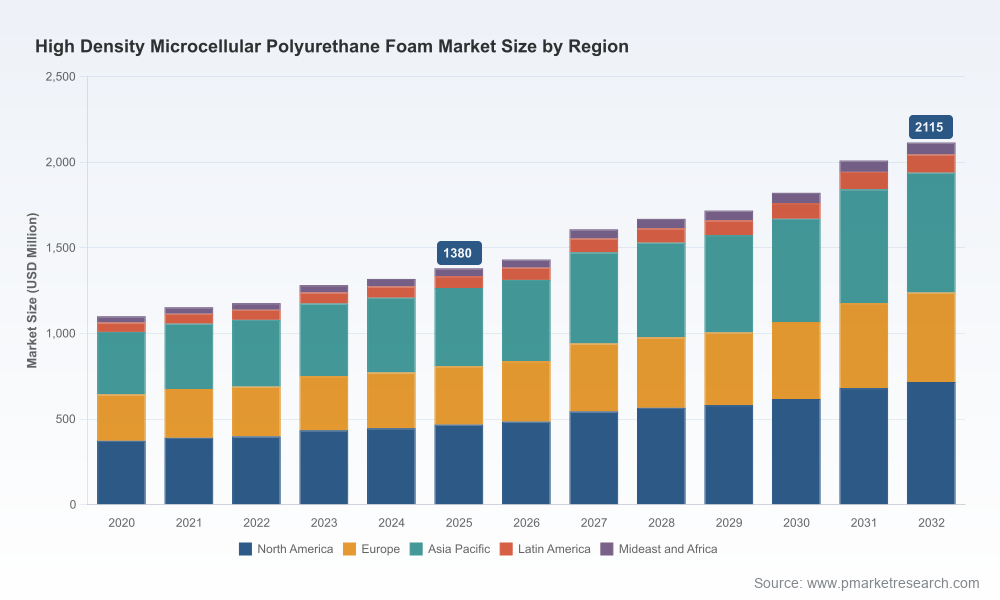

As companies prepare to make capital, sourcing, and product decisions in 2026, a clear-eyed understanding of the High Density Microcellular Polyurethane Foam market is no longer optional. This material class sits at the nexus of advanced cushioning, precision engineering, and industrial sealing, and it is being reshaped by macro supply pressures, regulatory tightening, and accelerated demand from electrification and aerospace quality chains. PW Consulting’s market study (base year 2025; historical coverage 2020–2025; forecast 2026–2032) synthesizes these forces into actionable strategy options. This executive introduction explains the study’s strategic value, highlights the practical outputs you can expect, and sketches the key implications for executives who must act in 2026.

High Density Microcellular Polyurethane Foam Market

The High Density Microcellular Polyurethane Foam market has demonstrated steady expansion through the historical period and enters the 2026–2032 forecast window with a projected compound annual growth rate (CAGR) of 6.5%. From the base year (2025), the market shows a robust upward trajectory into the early 2030s under our central scenario. This growth reflects a mix of rising demand from technical applications (automotive structures, battery systems, aerospace components) and heightened performance requirements in electronics and medical devices.

High Density Microcellular Polyurethane Foam Market

For strategic planners, two numbers matter most: the market size at the 2025 baseline (our study’s calibrated starting point) and the 6.5% CAGR that frames the forecasting envelope to 2032. Together these provide the top-line runway for capacity planning, product roadmaps, and M&A sizing exercises without relying on granular subsegment disclosure in this teaser.

High Density Microcellular Polyurethane Foam Market

Upstream feedstock volatility — In early 2026, our field monitoring captured regional spikes in polyurethane feedstock pricing: European polyurethane prices reached approximately USD 3.48/kg in March 2026 with a modest upward move from December, while South American benchmark prices were around USD 3.43/kg and saw sharper short‑term increases driven by constrained import cargo availability. These moves translate into non-trivial cost pressure for foam producers and frequently trigger short‑lead time repricing across contracts.

Transport and logistics friction — Freight disruptions and rerouting raised landed costs in several higher-growth markets during early 2026; India and other importing hubs saw increased landed costs driven by container shortages and rerouting. For manufacturers and OEMs this creates an increased incentive to localize supply or to redesign inbound inventories and contractual terms.

Environmental and regulatory tightening — Regulatory bodies are sharpening rules related to the environmental footprint of raw materials and production emissions. Compliance costs and documentation burdens are rising; manufacturers with advanced LCA (life‑cycle assessment) capabilities and lower-carbon feedstock roadmaps are positioned to convert regulatory obligation into go-to-market advantage.

Concentration and competitive dynamics — The market displays a moderate concentration profile: the top three players capture a meaningful portion of industry revenue, and the top five increase that share materially. This structure leaves space for specialist players with technical depth, and it favors consolidation strategies that can achieve scale in procurement and R&D amortization.

Reprice and renegotiate with visibility — Given feedstock and freight volatility, procurement leaders must adopt dynamic pricing clauses and scenario-based hedging for MDI, polyol and transport. Contracts that contain short-term pass-throughs without bilateral trigger thresholds will be a liability in 2026.

Localize critical nodes selectively — Not all localization is equal. Our scenario modeling shows that targeted nearshoring of cut-and‑finish operations, or critical technical compounding labs, delivers better cash conversion and reduced landed cost risk than full vertical duplication.

Invest in low-carbon product variants — Regulatory risk is increasingly a commercial opportunity. Companies that validate lower carbon-intensity feedstocks and can document LCA benefits for aerospace, medical, and EV-related buyers will unlock premium procurement lists and lengthened contract tenures.

Differentiate with technical services — As margins compress, firms that bundle engineering validation, custom compounding, and certification support for customers (e.g., automotive OEMs and aerospace suppliers) secure stickier relationships and higher total lifetime value.

Prepare M&A and alliance playbooks — Moderate market concentration combined with geographic cost dispersion makes 2026 a window for bolt-on acquisitions that accelerate market access or technical capability. Our deal simulation workstream shows where chemical knowledge and manufacturing footprints create asymmetric value.

The full study is constructed as a practitioner’s toolkit rather than a pure academic exercise. Key deliverables include:

Forecasting models (2026–2032) with scenario toggles — base, upside, and stress cases for feedstock prices, transport disruption frequency, and regulatory tightening.

Cost-to-serve and landed-cost calculator — a downloadable workbook that maps raw material, energy, labor, and freight inputs to per-unit economics across manufacturing footprints.

Supply‑chain playbook — actionable supplier segmentation and mitigation strategies, including recommended contracting language templates for price escalators and service-level commitments.

Commercial go-to-market modules — differentiated value propositions for automotive EV components, aerospace cushions and seals, medical-grade foams, and precision electronics packing.

M&A scorecard and integration checklist — a readiness framework to prioritize targets and de‑risk post‑deal integration across technology, quality systems, and customer retention.

The market’s mid‑to-high density niche is shaped by a mix of specialized manufacturers and vertically integrated suppliers. A few representative profiles illustrate the competitive logic you’ll find in the report’s detailed benchmark:

Rubberlite Inc. (Huntington, WV; https://www.rubberlite.com/) — Known for technical HyPUR-cel® families, Rubberlite competes on seal/gasket performance and industrial-grade customization. Their strength lies in application-specific compound expertise and long-standing OEM relationships.

XYFoams (Hubei Xiangyuan New Material Technology Inc., Xiaogan, China; https://www.xyfoams.com/) — A producer with a broad density range, XYFoams targets high-demand industrial segments including EV battery support and precision equipment. Their scale in Asia and cost structure provide aggressive commercial options in regional supply chains.

General Plastics Manufacturing Co. (Tacoma, WA; https://www.generalplastics.com/) — A specialist in LAST-A-FOAM® high-density microcellular products, they are positioned toward aerospace and precision engineering applications where specification compliance and certification traceability are decisive.

Urethane Technologies International (Monroe, WA; https://www.utech-polyurethane.com/) — Focuses on high-quality production and technical variants for industrial uses; their differentiation lies in process control and product consistency for demanding customers.

Our benchmarking framework evaluates these and other participants across eight dimensions — technology depth, scale, geographic footprint, supply-chain resilience, regulatory readiness, channel access, R&D pipeline, and commercial agility — and provides a succinct competitor scorecard in the full report.

We model three policy-relevant scenarios through 2032: (1) steady-state (central), (2) sustained cost inflation with periodic freight disruptions (stress), and (3) accelerated green-material adoption driven by new regulation and buyer mandates (policy-driven). Each scenario produces distinct margin, capacity utilization, and capital allocation outcomes. Tactical responses we advise for 2026 include:

Short-term: renegotiate supplier contracts with bilateral price triggers, tighten working capital buffers, and implement contingency freight lanes.

Medium-term: allocate capex to modular finishing lines that can be scaled regionally, and create product variants that command premium pricing due to verified environmental credentials.

Long-term: pursue partnerships or minority stakes in upstream feedstock innovators and engage in standard-setting initiatives to shape regulatory trajectories.

Beyond the market study, PW Consulting offers an implementation suite that combines the report’s quantitative models with hands-on execution capabilities: supplier negotiations, LCA verification support, joint product development facilitation, and M&A advisory. Our cross-functional teams pair former industry procurement leaders with polymer engineers to translate scenario outputs into executable project plans within 90 to 180 days.

2026 is a pivotal year for firms participating in high density microcellular polyurethane foam: cost volatility, regulatory tightening, and selective demand acceleration create both risk and optionality. The right combination of dynamic procurement, targeted localization, product differentiation, and proactive regulatory positioning will determine winners and laggards. PW Consulting’s 2025-calibrated study (covering 2020–2025 history and forecasting through 2032 at a 6.5% CAGR) is designed to be the decision-support backbone for executives who intend to act decisively in 2026.

This briefing intentionally highlights strategic findings while reserving the granular subsegment and regional breakdowns for report subscribers. To access the full dataset, scenario models, competitor scorecards, and implementation toolkits, please visit the report landing page or contact PW Consulting’s lead industry analyst team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:High Density Microcellular Polyurethane Foam Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com