Global Electron Beam Lithography Equipment Market Growing at 10.0% CAGR Through 2034

Other |

2026-06-22 11:02:04

As PW Consulting’s lead industry analyst, I present a condensed strategic preview of our comprehensive Silicon Nitride (Si3N4, CAS 12033-89-5) market study, timed for planning cycles that peak in 2026. The global market for silicon nitride is on a clear growth trajectory: valued at approximately USD 113.0 Million in our 2025 base year and projected to approach USD 183.4 Million by 2032, with a compounded annual growth rate (CAGR) of roughly 7.1% across the 2026–2032 forecast window. Those headline metrics encapsulate a technology-led materials market that is transitioning from niche high-performance applications toward broader industrial and medical adoption.

Silicon Nitride (CAS 12033-89-5) Market

Timing and capital allocation: 2026 is the inflection point when steady demand and regulatory milestones convert R&D investments in Si3N4 into scalable commercial returns. Firms making capacity, JV, or M&A choices in 2026 will either secure feedstock advantage and end-market access or face higher costs and longer time-to-market.

Silicon Nitride (CAS 12033-89-5) Market

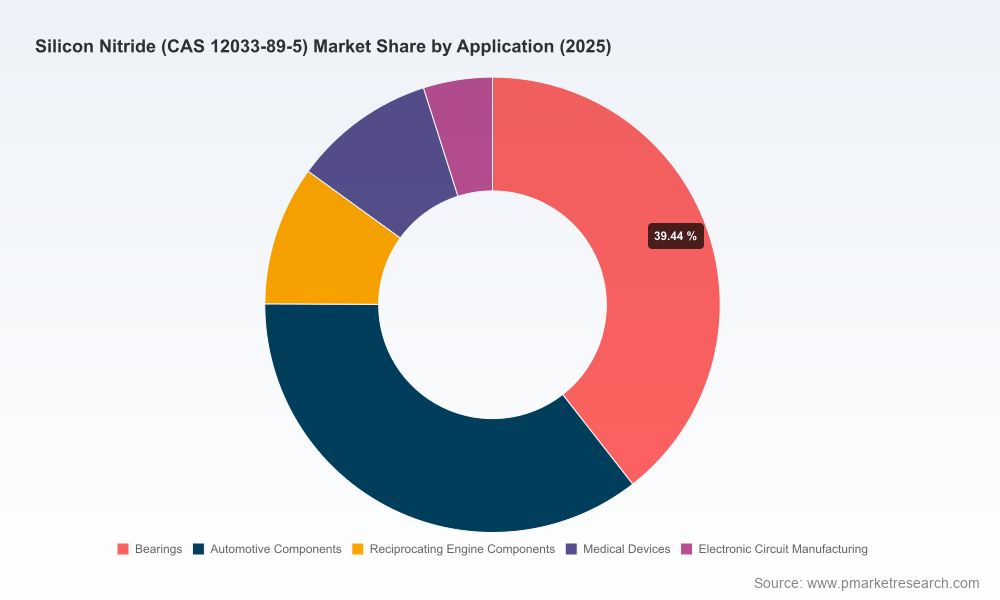

Product roadmaps: Si3N4’s combination of mechanical, thermal, and bioactive properties makes it a candidate for cross-industry product extensions (from bearings and cutting tools to medical implants). Strategic product development choices made in 2026 will determine whether companies capture the “premium” layer of future growth.

Silicon Nitride (CAS 12033-89-5) Market

Supply resilience and vertical strategy: With a supply base that exhibits regional technical specialization, 2026 decisions about supplier contracts, qualification timelines, and potential backward integration will materially affect cost curves and time-to-revenue over the forecast horizon.

Three structural drivers underpin the forecasted ~7.1% CAGR. First, technology diffusion: silicon nitride’s performance envelope—wear resistance, thermal shock tolerance, and in some grades favorable biocompatibility—is enabling penetration into higher-volume industrial subsystems and certain medical implants. Second, regulatory validation: recent medical-device clearances have shifted silicon nitride from a laboratory curiosity to a commercially addressable biomaterial class. Third, supply-side maturation: improvements in production routes and powder chemistry have increased consistency and reduced qualification friction for downstream manufacturers.

These forces combine to make 2026 an operational hinge year. Firms that accelerate qualification cycles and secure tiered supply commitments in 2026 stand to capture disproportionate share growth through 2032. Conversely, late movers will face a higher bar on supplier evaluation and potentially longer certification timelines, particularly in regulated medical and semiconductor adjacent markets.

A notable recent development underlining this transition is the regulatory progress of an industry participant that pursued and achieved US FDA 510(k) clearance for a Si3N4 orthopaedic implant system in 2025. That clearance—preceded by a 510(k) submission earlier that year—represents the first commercial availability of a silicon nitride implant in that specific clinical segment. In practical terms: device OEMs, implant component suppliers, and investors should treat 2026 as the start of the commercial phase for Si3N4 in select medical niches, with implications for reimbursement strategy, clinical evidence generation, and scaled manufacturing.

The market is neither a pure commodity nor a closed oligopoly. Aggregate concentration metrics point to a market where the top three and top five suppliers hold material but not dominant shares, creating room for challengers with technical or regulatory differentiation. Key company archetypes and strategic positions emerging from our analysis include:

Japanese specialty producers — Exemplified by established chemical manufacturers: these firms are widely recognized for high-purity Si3N4 powders produced by advanced synthetic routes. Their strengths are tight impurity control, consistent powder morphology, and longstanding customer relationships in precision applications such as semiconductors and bearings.

European high-performance ceramic houses — Companies focused on component manufacturing and hot-pressing routes bring capabilities in complex sintered parts for aerospace, automotive, and industrial tooling. Their advantage lies in application engineering, scale in component processing, and global aftermarket channels.

Medical-materials innovators — A US-based company with an FDA-registered Si3N4 manufacturing facility has moved medical-grade powders and implants into clinical reality; its regulatory moat provides a first-mover edge in implantable devices and creates an ecosystem advantage for partners seeking qualified biomaterials.

Emerging suppliers from China and other regions — These players offer cost-competitive powders and are consolidating capabilities in amorphous and near-amorphous grades for non-critical structural applications. Their growth path will depend on closing quality gaps and achieving broader certifications.

For executive teams, the competitive takeaway is straightforward: suppliers cluster by technical offering (powder chemistry and purity), component fabrication capability, and regulatory footprint. Sourcing and partnership strategies should therefore prioritize two vectors—material qualification depth for high-value applications, and supply redundancy for volume segments.

Raw-material variability is a constant strategic risk. High-purity powder grades—produced predominantly by advanced-process manufacturers—differ materially from standard grades in terms of impurity levels and oxygen content, which affects sintering behavior and part performance. Buyers targeting performance-critical segments must plan multi-stage qualification programs and should expect premium pricing and longer lead times during the next 12–24 months.

From a procurement perspective, firms should evaluate three levers in 2026: (1) technical co-development agreements with powder suppliers to tailor chemistries; (2) conditional-capacity reservations or toll-manufacturing arrangements to secure throughput; and (3) backward-integration feasibility studies where scale justifies investment. These levers will be especially relevant for OEMs entering medical, semiconductor, and high-speed rotating-equipment markets.

Defensive incumbent — Prioritize locking long-term supply contracts for high-purity grades, invest in qualification labs, and accelerate incremental product upgrades for existing Si3N4 applications.

Aggressive entrant — Target niche medical or semiconductor adjacencies where regulatory or technical barriers create opportunity windows; consider partnerships with material innovators and M&A of specialist component makers to shortcut go-to-market.

Cost-leadership play — Work with lower-cost powder producers to develop value-optimized grades for high-volume, lower-spec applications; focus on process robustness and downstream automation to lower total delivered cost.

PW Consulting’s full Silicon Nitride market study is built for decision-makers who need executable intelligence, not just charts. Highlights include:

An integrated demand model (2020–2032) with scenario variants designed for capital planning and product launch timing.

Supplier dossiers and a technical supplier matrix that map powder chemistries to downstream manufacturing routes and qualification complexity.

Regulatory pathway maps and clinical evidence templates for medical device firms seeking to use Si3N4 in implants, including recommended trial designs and regulatory milestones.

A commercial due-diligence playbook for M&A and JV activity, including benchmark valuation drivers and a short list of target profiles.

Manufacturing economics: cost-per-part sensitivity analyses across powder grades, forming methods, and sintering technologies to support capex decisions.

Go-to-market options and partner archetypes for getting from prototype to commercial production within 12–36 months.

Note: while this preview summarises the strategic intelligence, detailed subsegment tables (regional breakdowns, application-by-application demand curves, and supplier share matrices) are intentionally withheld from this overview to preserve the investigative value of the full report.

Initiate supplier qualification pilots now: budget and begin cross-functional qualification in H1 2026 to compress the typical 12–24 month timeframe.

Set conditional capacity commitments: negotiate volume options or take-or-pay windows with technical suppliers to manage ramp risk without overcommitting capital.

Prioritize regulatory strategy for medical aspirations: leverage alliances with firms that have existing approved manufacturing infrastructure where possible.

Run a targeted M&A scan: prioritize assets that bring either a certified medical facility, proprietary powder chemistries, or scalable component manufacturing in regions critical to your revenue mix.

Si3N4 is moving from a performance-material specialty into a market with clear mid-term commercial trajectories across industrial and select medical applications. The USD 113.0 Million market base in 2025, expanding at a projected 7.1% CAGR through 2032, creates a window in 2026 where strategic moves—capacity reservations, regulatory positioning, or focused M&A—translate into disproportionate share gains. The full PW Consulting report supplies the operational granularity required to translate these strategic choices into executable plans. For organizations that need to decide on capital allocation, supplier strategy, or market entry in 2026, treating Si3N4 with priority in the planning cycle is not optional: it is a strategic imperative.

Access the full report for the complete dataset, supplier scorecards, and action templates that translate this preview into a 6–18 month operational plan. The full analysis contains the specific subsegment tables and actionable numbers you will need to finalize 2026 budgets and go-to-market milestones.

For detailed analysis of this topic, please visit the official page:Silicon Nitride (CAS 12033-89-5) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com