MP3 Player Market 2026: Strategic Preview for Executive Decision-Makers

As PW Consulting’s Chief Industry Analyst, I present a focused preview of our new MP3 Player Market report—an executive-grade intelligence package designed to inform strategic decisions in 2026. This piece establishes the rationale, analytical scaffolding, and actionable vantage points you need to evaluate opportunities and risks in a mature, niche consumer-electronics sector. It is intentionally a “trailer”: we surface the signal—market trajectory, competitive context, and decision frameworks—while reserving the granular, segment-level tables and proprietary scores for the full report on our site.

MP3 Player Market

Why this market matters in 2026

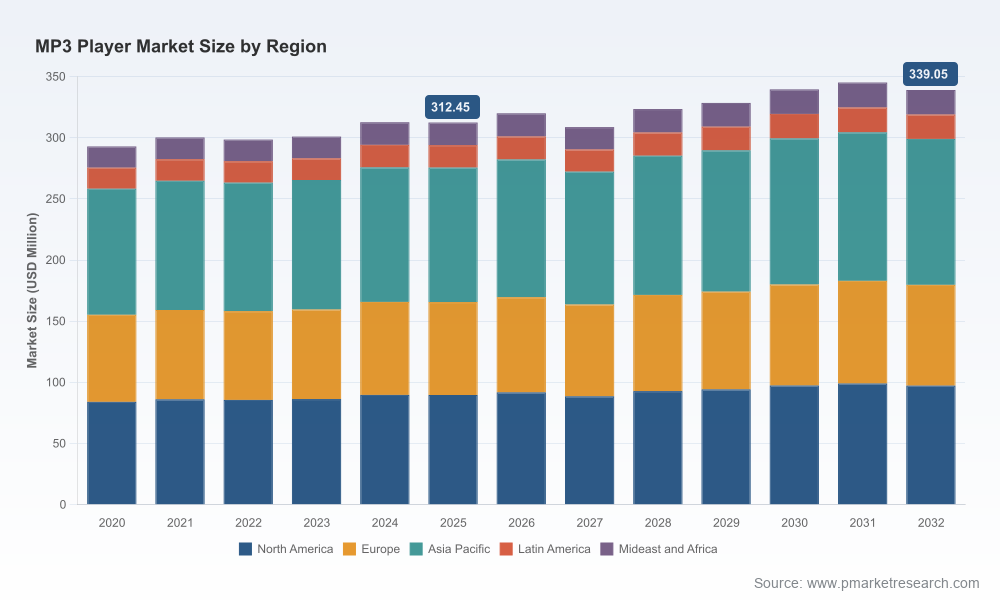

The MP3 player market is often mischaracterized as legacy hardware relegated to nostalgia. Our work finds a different reality: a compact, resilient ecosystem anchored by focused consumer segments, specialized product innovations, and adjacency play opportunities (accessories, bundled content, licensing). After a period of modest volatility through the early 2020s, the market stabilized near roughly USD 312 million in 2024–2025. Our base-year analysis (2025) and forecast horizon (2026–2032) projects a conservative compound annual growth rate (CAGR) of about 1.12%, yielding a low-to-mid–300s million-dollar market by the early 2030s.

MP3 Player Market

Why should executives care about a low-single-digit CAGR market? Because maturity brings clarity: user preferences are well-formed, cost structures are predictable, channel economics are stable, and the competitive landscape is fragmented—conditions that favor targeted strategic moves (product line optimization, high-margin niches, selective M&A and licensing arrangements) with rapid payback on invested capital.

MP3 Player Market

Top-level market character

- Stability with episodic pockets of innovation: growth is modest overall, but pockets of premium and specialist demand (audiophile-grade devices, youth-oriented wearable integrations, ruggedized players for specialized applications) create outsized margin opportunity.

- Fragmented competition: concentration metrics indicate a market where leading global brands co-exist with regional specialists and OEM providers—enough scale at the top to set technical and distribution benchmarks, but not so consolidated as to block new entrants.

- Durable value pools: while hardware volume growth is restrained, services and accessory ecosystems (content bundles, licensed codecs, premium earbuds, subscription tie-ins) represent actionable pathways to revenue expansion.

What the report delivers (practical content)

The full report is structured around deliverables that directly support board and executive decision-making in 2026:

- Strategic landscape maps: concise one-page views that align product archetypes (entry flash-based players, premium digital audio players, hybrid devices) with buyer needs, margin profiles, and channel dynamics.

- Go-to-market playbooks: tailored strategies for incumbents, challengers, and new entrants covering pricing architecture, distribution mixes (direct-to-consumer vs. retail), and promotional levers calibrated to customer lifetime value.

- Value-capture models: a set of financial templates and sensitivity analyses (TAM/SAM/SOM roll-ups, unit economics, break-even models) that let you model scenarios under conservative and aggressive adoption assumptions.

- Product and innovation roadmap guidance: prioritized technology investments (battery life improvements, high-resolution audio support, Bluetooth and streaming handshake enhancements, ruggedization) with expected ROI horizons and supplier considerations.

- Risk and resiliency playbook: supply-chain stress tests, component concentration matrices, and contingency playbooks to safeguard launches and seasonal inventory.

- Commercial diligence toolkit: a checklist and scorecard for evaluating M&A targets and strategic partnerships, including red-flag indicators and synergies stress-tested against our market model.

Methodology and confidence calibration

Our market construct combines triangulated inputs: primary interviews across retail, distribution and OEM channels; financial analysis of disclosed product lines; shipment and install-base proxies; and bottoms-up modeling of end-user cohorts. Scenario planning underpins our 2026 guidance—best-case, base-case (used to derive the ~1.12% CAGR), and downside stress scenarios are included in the full report. Importantly, while headline macro numbers are robust, the full segmentation matrices, competitor market shares, and proprietary scoring remain gated—intended to drive direct engagement and to preserve the integrity of our primary-source inputs.

Competitive landscape — practical takeaways

Three global firms anchor the visible competitive set and illustrate the strategic variety within the market:

- Sony Corporation (Tokyo, Japan; https://www.sony.com): Sony’s Walkman line demonstrates how a legacy brand can sustain premium positioning through product differentiation, brand heritage, and careful high-margin feature sets (audio fidelity, bespoke UX, premium materials). Their strategy shows the endurance of aspirational hardware and how brand-led premiumization can coexist with low-growth markets.

- Samsung Electronics Co., Ltd. (Suwon, South Korea; https://www.samsung.com): Samsung’s historic and portable media player efforts reflect a platform-oriented mindset—leveraging software and ecosystem tie-ins to sustain device relevance. For companies evaluating partnerships, Samsung’s approach highlights the importance of interoperability and seamless streaming integration as defensive measures against commoditization.

- Creative Technology Ltd. (Singapore; https://www.creative.com): Creative exemplifies the niche-specialist playbook—targeting audio enthusiasts and accessory-led bundles. Their product mix and channel choices show how focused innovation (sound-processing features, accessory ecosystems) can create defensible microsegments even in a mature market.

Across these profiles, three strategic vectors emerge: brand-led premiumization, ecosystem integration, and niche specialization. Each vector demands different resource commitments and delivers different risk/return profiles. The full report includes competitor benchmarking matrices and decision trees to assist resource allocation choices between these vectors.

Strategic options for 2026

Executives using this report in 2026 will be choosing from a small set of high-leverage strategic options—our analysis helps prioritize them by expected margin accretion, time-to-impact, and organizational fit:

- Optimize portfolios toward margin over volume: trim low-velocity SKUs, reallocate R&D and marketing to premium or high-margin accessories, and pursue SKU rationalization to reduce working capital drag.

- Pursue adjacent monetization: bundle content licensing, offer subscription tie-ins, or embed premium audio codecs to increase ARPU without relying on device volume growth.

- Selective M&A and partnerships: target distressed or high-synergy niche players to acquire capabilities (DAC tuning, niche content rights) rather than market share. Use our commercial diligence toolkit to quantify synergy capture and downside exposure.

- Channel reconfiguration: double down on high-margin D2C channels where feasible, and negotiate consignment or buy-back terms with retail partners to mitigate obsolescence risk.

- Supply-security investments: pursue multi-sourcing for critical components and implement inventory hedges for peak selling windows; our risk matrices prioritize parts and suppliers by impact and likelihood.

KPIs and dashboards we recommend

To translate strategy into measurable outcomes, the report proposes a concise KPI stack tailored to the market’s economics:

- Unit economics by product archetype (gross margin per SKU, contribution margin, payback on marketing spend).

- Channel mix elasticity (revenue per channel, return on promotional spend by channel).

- Customer LTV and attachment rate (accessory/content attach rates; subscription conversion rates).

- Supply resilience index (single-source dependency score, average lead time volatility).

Templates to populate these KPIs are included in the full deliverable so teams can run sensitivity tests with their own data.

Use-cases: how leaders are applying the research

- Product executives use our roadmap prioritization to re-weight R&D toward battery and codec improvements that lift resale value and accessory attach rates.

- Corporate development teams apply the M&A scorecard to fast-track two to three candidate acquisitions with clear capability synergies and low integration drag.

- Commercial teams reconfigure pricing ladders and promotional calendars to protect margins during seasonal troughs, informed by the elasticities in our playbooks.

Closing—and next steps

The MP3 player market in 2026 is not a growth story in headline terms, but it is rich in strategic choices. With a stable base size in the low–to–mid hundreds of millions and a modest forecast CAGR, the opportunity for value creation lies in disciplined portfolio moves, differentiated product strategies, and monetization beyond the box. The full PW Consulting report provides the confidential segmentation tables, detailed competitor share analysis, and proprietary scoring that practitioners need to act with confidence.

For executives ready to convert insight into action, the next step is direct engagement: access the full report to download the detailed models, competitor scorecards, and playbooks, or schedule a workshop with our strategy team to tailor the findings to your organization’s risk profile and capabilities.

For detailed analysis of this topic, please visit the official page:MP3 Player Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com