Second-Life Automotive Battery Module Systems Market Estimated at USD 2.2 Billion in 2026, Forecast to Reach USD 9.4 Billion by 2036

Other |

2026-07-08 19:02:30

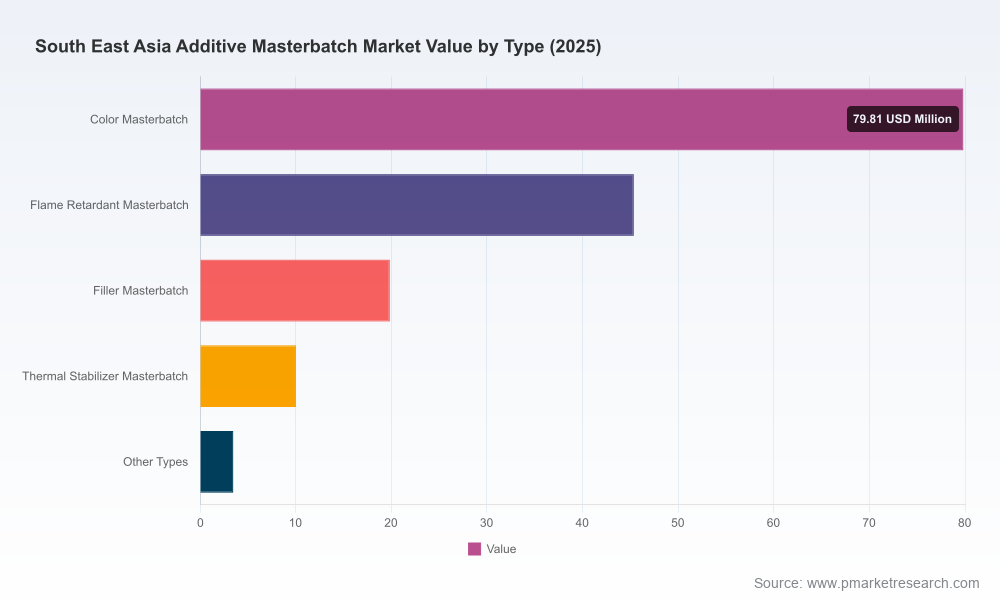

PW Consulting’s South East Asia Additive Masterbatch Market study is a decision-grade briefing tailored for executives who must act in 2026 with both speed and conviction. Built on a 2025 base year and projecting through 2032, the analysis integrates market sizing, scenario-based forecasts and operative playbooks to convert industry complexity into explicit choices. At the aggregate level, the market grows from roughly USD 120 million in 2020 to an estimated USD 158.5 million in 2025, and is projected to reach approximately USD 241.3 million by 2032 — a trajectory underpinned by a 6.5% CAGR across the 2026–2032 forecast window. This research is structured as a strategic trailer: it demonstrates analytical depth and practical outputs while reserving granular sub-segment tables for the full report to preserve commercial value and encourage follow-on engagement.

South East Asia Additive Masterbatch Market

Clarity under cost pressure: Firms face simultaneous shocks — resin volatility, freight surcharges and shifting labor dynamics. Our study translates these inputs into margin and breakeven scenarios so CFOs can prioritize price passes, hedging, or SKU rationalization.

South East Asia Additive Masterbatch Market

Product and portfolio prioritization: With tighter regulatory scrutiny on certain additive chemistries and accelerating sustainability requirements, R&D and product roadmaps must be re-weighted. This report identifies which additive families and application routes will deliver defensible ROI in the near term.

South East Asia Additive Masterbatch Market

Supply chain design and nearshoring: The research maps supply vulnerabilities and highlights realistic options for nearshoring, tolling partnerships, and regional distribution hubs that materially reduce lead times and exposure to freight volatility.

M&A and partnership scouting: We provide a structured approach to target screening and valuation sensitivities for bolt-ons, contract manufacturers, and specialty compounders to accelerate capacity or capability acquisition.

Input-cost volatility: Average masterbatch price points spiked regionally amid upstream resin swings; for example, market reporting in mid‑2025 recorded elevated masterbatch pricing in Thailand, highlighting input-cost pass-through as a live P&L lever for 2026 planning.

Regulatory tightening: Environmental restrictions on select additives continue to reconfigure formulation options. Compliance-driven reformulation is not optional — it is a capex and opex consideration that affects product roadmaps, customer retention and claims around recyclability.

Logistics and freight pressure: Persistent shipping disruptions have raised landed costs for producers who import pigments and carrier resins. Transport surcharges require re-examining supplier contracts and inventory strategies to protect gross margins.

Labor and operational cost swings: Wage inflation in several ASEAN hubs combined with raw-material cost fluctuations creates a corridor of uncertainty for pricing strategies and localization decisions.

Trade-policy noise: Tariff variability and ad hoc trade measures are increasing the effective cost of cross-border pigment and resin flows; this makes customs strategy, bonded warehousing and local backward-integration strategic levers.

Demand remains anchored in traditional end-markets — automotive, packaging and construction — but the growth drivers and required value propositions vary. Packaging is rapidly evolving under circularity and regulatory pressures; this creates near-term demand for additive masterbatches that enable recyclability and downgauging. Automotive requires higher-performance functional additives (UV, flame-retardant, thermal stabilizers) as vehicle electrification and lightweighting intensify. Construction offers steady base demand but is sensitive to commodity cycles.

From a product-type perspective, color masterbatches continue to command broad usage, while performance and functional additive combinations (e.g., flame-retardants paired with impact modifiers or UV stabilizers) are where margin uplifts and differentiation occur. The practical implication for manufacturers is to shift from commodity color fill to higher-value bundled solutions and service contracts (e.g., color matching, just-in-time replenishment, regulatory dossiers).

South East Asia is heterogeneous: some countries are manufacturing hubs with vertically integrated compounders and strong automotive supply chains, while others are growth markets for consumer-packaged goods and construction polymers. For 2026 execution, exporters and regional producers must adopt country-level playbooks — balancing centralized R&D and QC with decentralized manufacturing footprints to reconcile cost, speed and regulatory compliance.

The market features both regional specialists and multinational compounders. Key players profiled in the study include:

US Masterbatch Joint Stock Company (Hanoi, Vietnam) — Specializes in additive masterbatch production and export across South East Asia, offering UV stabilizers, flame retardants, anti‑static agents and process aids tailored to plastics processors. Strategic implication: strong regional export orientation and customization capability make it an attractive partner for OEMs seeking localized supply with technical support. (https://usmasterbatch.com/)

PMJ Greentech Joint Stock Company (Vietnam) — Focuses on additive masterbatches such as PPA and desiccant masterbatches alongside filler solutions, emphasizing customization. Strategic implication: niche specialization and close industry ties enable rapid formulation changes for local customers. (https://www.pmj.vn/)

Tosaf Compounds Ltd (Israel) — Global compounder supplying packaging and industrial sectors with PPA, UV stabilizers and functional additives; recent capacity expansions outside the region reflect a dual strategy of serving local markets and global customers. Strategic implication: multinational logistics footprint and technology transfers create competitive pressures on regional players. (https://www.tosaf.com/)

TPI Polene Public Company Limited (Thailand) — Offers polyethylene compounds and masterbatches for films, laminates and injection molding; integration into regional polyolefin value chains is a core strength. Strategic implication: integration with resin supply can create cost and lead‑time advantages. (https://www.tpipolene.com/)

SCG Chemicals Co., Ltd. (Thailand) — Develops color masterbatches with functional additives, targeting automotive and medical sectors. Strategic implication: scale and product breadth position SCG to pursue premium segments requiring certification and traceability. (https://www.scgchemicals.com/)

Thaipoly Masterbatch Co., Ltd. & Chokdee Masterbatch Co., Ltd. (Thailand) — Local specialists focused on color matching and functional additives for consumer packaging and injection molding. Strategic implication: regional manufacturing agility and customer intimacy are competitive differentiators for local demand fulfillment.

Recent market developments that affect competitive dynamics include facility expansions by global compounders and product innovations enabling recyclability in PET closures. These moves emphasize two strategic themes for 2026: capacity repositioning in response to demand geography, and product innovation aimed at circularity and regulatory compliance.

Market sizing & dynamic forecast model (2020–2032) with sensitivity runs and scenario toggles for resin price, freight cost and regulatory constraints.

Demand-mapping by application and product family, with econometric drivers and growth pockets identified. (Note: detailed segment tables and percent splits are available in the full report.)

Price-cost modelling that translates resin and pigment price paths into margin stress points and identifies profitable pricing thresholds.

Supply-chain heat map highlighting import dependencies, candidate nearshoring locations, tolling partners and logistics levers to reduce landed costs.

Regulatory impact matrix detailing additive chemistries under scrutiny and compliant formulation pathways per jurisdiction.

Competitive intelligence dossiers on key manufacturers, with capability matrices, capacity indicators and M&A targets prioritized by strategic fit.

Commercial playbooks — go-to-market tactics for producers, tollers, and distributors including sample pricing templates, service offers and account segmentation rationales.

Re-run capital plans against the report’s scenarios. Use the sensitivity model to assess whether new capacity should be greenfield, brownfield expansion, or secured via tolling/contract manufacturing.

Rebalance product portfolios toward bundled solutions that capture service fees and reduce price elasticity. Prioritize development efforts where regulatory headwinds create supplier scarcity.

Re-negotiate supplier terms with explicit clauses for freight surcharges and resin price passthroughs, and evaluate strategic stockpiles for critical pigments and carriers to smooth production.

Deploy a targeted M&A and partnership playbook: prioritize partners that close capability gaps (e.g., recyclability formulation, specialty functional additive know-how) and provide local manufacturing footprints to mitigate tariff and freight risk.

Operationalize compliance: create a regulatory dossier and testing roadmap for all high-risk chemistries and adopt traceability protocols that support customers’ circularity claims.

The South East Asia additive masterbatch market presents a classic strategic inflection: steady aggregate growth (6.5% CAGR in our forecast horizons) with sharply differentiated outcomes at the product and country level depending on how incumbents and new entrants respond to cost volatility, regulation, and logistics pressure. PW Consulting’s study converts that complexity into a clear set of actions — from detailed cost models to a prioritized list of capability investments and M&A targets. This article has outlined the themes and tactical levers; for the granular segmentation, model inputs, and the executable annexes that your strategy team can put to work this quarter, please access the full report and accompanying datasets available from PW Consulting.

For detailed analysis of this topic, please visit the official page:South East Asia Additive Masterbatch Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com