PW Consulting: Diagnostic X‑Ray Market Poised for 5.6% CAGR Through 2032

Other |

2026-07-12 02:53:26

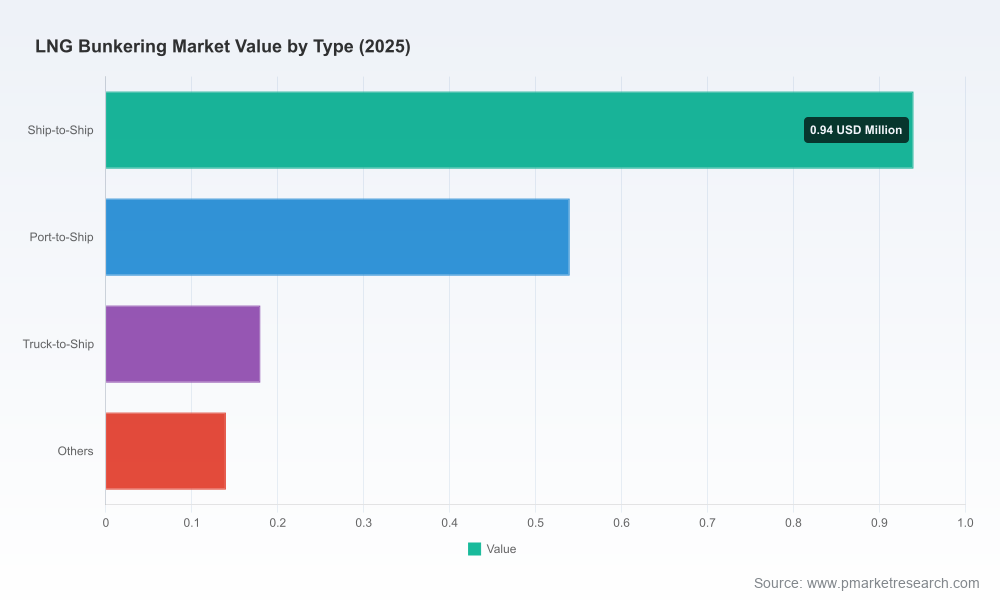

Between 2020 and 2025 the LNG bunkering market moved from an early demonstration phase into the first wave of commercial scale‑up. Our base‑year synthesis shows a market that expanded from approximately USD 0.55 Million in 2020 to about USD 1.8 Million in 2025 and that, under the central case in this study, is expected to reach roughly USD 2.24 Million in 2026 and accelerate to nearly USD 9.7 Million by 2032 — reflecting a compounded annual growth rate (CAGR) of 27.8% over the forecast window. Those headline dynamics signal more than a growth story: they represent an urgent timetable for strategic choices by ports, shipowners, fuel suppliers, infrastructure investors and regulators.

LNG Bunkering Market

Timing of capital deployment: In a market growing at nearly 28% CAGR, first movers secure pricing and capacity advantages but also face demand risk if they overbuild. Our study shows when and where demand thresholds are likely to tip into sustained utilization for small and mid‑scale bunkering assets — the kind of intelligence needed to justify FID in 2026.

LNG Bunkering Market

Commercial contracts and counterparty risk: The transition from ad‑hoc bunkering to long‑term supply arrangements is well underway. The research maps practical contracting structures and term lengths that balance offtake certainty with commercial flexibility for emerging fuel portfolios (including bioLNG and low‑CI fuels).

LNG Bunkering Market

Operational readiness and safety compliance: New harmonized best practices and codes reduce regulatory ambiguity but raise minimum compliance costs. The report links regulatory triggers (including recent DOE adjustments and new IRClass guidance) to operational checklists and CapEx/Opex estimates needed for safe, certifiable operations.

Portfolio and partnership choices: For energy majors, specialist suppliers and shipping lines deciding whether to build, charter, partner or buy capacity, the study offers decision trees and risk‑reward profiles calibrated to 2026 market conditions.

Integrated market sizing and three‑scenario forecasts (conservative, base, accelerated) covering 2026–2032, with transparent assumptions and sensitivity tables to test fuel price, vessel uptake and infrastructure lead times.

Asset deployment playbooks: modular build paths for shore‑side terminals, ship‑to‑ship (STS) deployment sequencing, and truck‑to‑ship operations, including recommended vessel classes and utilization thresholds for each operating model.

Regulatory and permitting roadmap tied to major jurisdictions, with actionable timelines and checklists for compliance, including steps triggered by recent policy shifts.

Competitive supplier scorecards and capability matrices that evaluate operational footprint, fleet composition, supply integration and strategic partnerships — enabling rapid short‑listing and due diligence prioritization.

Investment underwriting toolkit: downloadable financial models (three‑statement templates), IRR and payback heatmaps, financing structures, and a risk‑adjusted valuation approach for both greenfield and brownfield projects.

Commercial contracting templates and negotiation playbooks for offtake, vessel charter, and joint ventures — written to be adapted for local legal/regulatory conditions.

Geospatial demand‑supply overlays and prioritized port opportunity lists supported by AIS traffic analytics and cargo conversion scenarios (note: the public summary intentionally omits port‑level granular data to preserve the study’s proprietary value).

Major integrated energy companies are moving beyond pilot projects into dedicated merchant bunkering fleets and long‑term supply agreements. These operators combine trading, logistics and vessel ownership to capture margin across the value chain. Expect continued JV activity between shipping lines and energy majors to secure both vessel capacity and fuel supply certainty.

Specialist regional providers are scaling with purpose‑built vessels tailored to local port restrictions and commercial patterns. Their strength is operational agility and deep relationships with coastal operators and port authorities; their growth trajectories often make them attractive partners or acquisition targets for global players seeking on‑the‑ground reach.

Shipowners and ship managers are forming procurement consortia and opting for hybrid strategies — contracting fixed volumes where possible while retaining flexibility through time‑charter and spot purchasing options to manage fuel price volatility and regulatory uncertainty.

New entrants and niche service providers are differentiating on decarbonized LNG blends (e.g., bioLNG) and certification services, positioning themselves as premium suppliers for cargo segments with strict sustainability mandates.

The market concentration profile is meaningful: the top three players account for a substantial share of current commercial supply capacity, and the top five capture a majority share. That concentration pattern creates both opportunities for smaller players to specialize and risks of regional gatekeeping that buyers must address through contractual and partnership strategies.

Joint ventures between energy majors and large shipowners to co‑own sizable bunker vessels and lock in long‑term offtake demonstrate a shift toward vertically integrated supply models. These arrangements accelerate deployment of high‑capacity assets but also raise competitive barriers for pure‑play suppliers.

New operational launches and regionally focused bunkering services on major coasts indicate that operational know‑how and regulatory approvals are no longer the primary constraints — access to volumes and stable offtake remains the gating factor.

Policy and regulatory updates (including DOE order adjustments and the publication of harmonized industry best practices) have two effects: they lower legal/regulatory uncertainty for investors but set higher baseline operational standards and inspection regimes that influence cost estimates and timelines.

Local infrastructure decisions — for example, final investment decisions on small‑scale ports and targeted vessel charters — can shift regional economics within months. Investors should treat such developments as trigger events in their deployment roadmaps.

Ports: prioritize modular, scalable infrastructure that can be commissioned fast and expanded in phases. Embed multi‑fuel handling capability and allow for co‑location of truck, pipeline and STS operations to maximize throughput options.

Shipowners: move from intention to staged execution — secure optionality through medium‑term time‑charters or aggregated offtake agreements while using hedged exposure to fuel price movements; test bioLNG pilots for high‑visibility trade lanes.

Fuel suppliers and traders: lock supply flexibility via diversified sourcing and inventory staging; pursue partnerships with regionally strong operators to mitigate port access restrictions and accelerate route coverage.

Investors and lenders: require asset‑level stress testing including regulatory risk, utilization shortfalls and fuel price shocks; prefer structures with staged equity tranches and revenue‑linked loan covenants.

EPCs and equipment suppliers: standardize modular skid designs for quicker permitting cycles, and offer integrated safety and compliance packages to reduce operational ramp time for buyers.

The most valuable output for executives operating in 2026 is not a single point forecast but a set of stress‑tested scenarios that translate macro assumptions into asset‑level outcomes. Our analysis provides scenario matrices that link fuel prices, ship uptake rates, and permit lead times to cashflow outcomes and utilization breakpoints. These enable planners to see, for example, how a six‑month delay in permitting or a sustained 20% swing in fuel spreads alters IRRs and the timeline for additional vessel commitments — information that is essential when negotiating contracts or timing FIDs.

Methodology: an integrated bottom‑up approach that combines AIS traffic analytics, primary interviews across the value chain, and asset economics rather than pure top‑down extrapolation.

Actionability: downloadable financial templates, contract language, and port prioritization maps enable immediate translation of insight into procurement, negotiation and investment actions.

Market validation: the study triangulates public announcements, operator filings and on‑the‑ground intelligence to reconcile headline market growth with operational constraints and competitive positioning.

In short, as stakeholders plan capital and commercial moves in 2026, the difference between an opportunistic outcome and a strategically winning position will be determined by the quality of demand timing, the calibration of contract terms, and the foresight to structure partnerships that share operational and market risk. Our full report contains the granular, port‑level analytics, proprietary segmentation and downloadable models needed to act decisively. This summary intentionally omits the detailed segment and port‑level datasets that underpin our conclusions — those proprietary deliverables are included in the full study for clients ready to transition from insight to execution.

For detailed analysis of this topic, please visit the official page:LNG Bunkering Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com