Injection at Home Services for Senior Citizens’ Healthcare Needs

Health |

2026-06-15 11:24:26

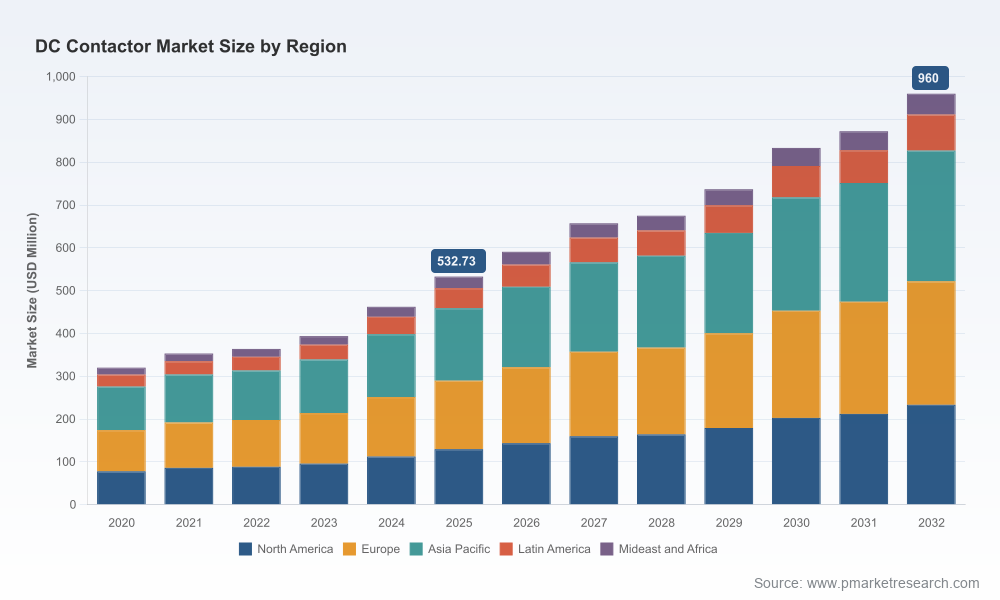

As companies map their product roadmaps, M&A pipelines and supply‑chain strategies for 2026, the DC contactor market has emerged as a focal point where electrical safety, power density and system integration converge. PW Consulting’s latest market study (base year 2025; forecast period 2026–2032) synthesizes the underlying economics, technological inflection points and competitive dynamics you need to make confident, time‑sensitive decisions. The headline: after accelerating from roughly USD 320 million in 2020 to about USD 533 million in 2025, the market is projected to continue expanding at a compound annual growth rate of 8.79%, approaching approximately USD 960 million by 2032. This trajectory reframes DC contactors from niche components into strategic elements of electrified platforms across EV, energy storage and industrial segments.

DC Contactor Market

Actionable market sizing and demand modeling: granular scenario models (base / upside / downside) tied to product, application and technology pathways — delivered as configurable tools to stress‑test your 18‑month and 3‑year plans.

DC Contactor Market

Commercial playbooks: go‑to‑market options tailored to OEMs, Tier‑1 suppliers and aftermarket service providers, including pricing levers, channel strategies and OEM co‑development constructs.

DC Contactor Market

Supply‑chain and cost sensitivity analysis: raw‑material exposure maps, supplier risk heatmaps and recommended hedging/dual‑sourcing tactics to protect margins amid commodity volatility.

Technology and product roadmaps: prioritized feature investments (arc suppression, thermal stability, compact packaging, and diagnostic telemetry) with estimated development timelines and CAPEX profiles.

Competitive intelligence and target screening: validated supplier profiles, capability matrices and a short list of inorganic targets or partners calibrated to your strategic ambition.

Regulatory and standards tracker: evolving safety and certification requirements and the implications for test programs, compliance budgets and time‑to‑market.

Several converging dynamics make 2026 a decision point rather than a planning checkpoint. First, system electrification continues to accelerate across vehicle platforms and energy infrastructures; suppliers are being evaluated not just on current ampere or voltage ratings but on how their devices integrate into high‑voltage battery and power electronics ecosystems. Second, regulatory expectations for arc suppression, dielectric stability and thermal performance are tightening — a trend that materially affects design validation schedules and supplier qualification. Third, cost pressure is real: our industry monitoring shows raw‑material prices for DC contactor manufacturers rose by approximately 5.4% in 2025, compressing margins for vendors that lack tactical procurement responses or scale advantages.

These forces translate into discrete commercial consequences: product specifications that were formerly “nice‑to‑have” (advanced arc suppression, integrated diagnostics) are becoming threshold requirements for system acceptance; lead times and qualification hurdles are lengthening; and procurement teams are prioritizing supplier reliability and long‑term roadmaps over short‑term price wins. For strategic buyers and suppliers alike, the question for 2026 is simple: build capability, secure supply, or cede ground to better prepared competitors.

The DC contactor market shows a moderate concentration: the top three global players account for roughly 62% of supply, and the top five for around 75%. This structure creates a dual strategic environment — incumbents with scale advantages on one side, and specialist or regional players on the other, each with different routes to competitive advantage.

Large diversified incumbents (examples): companies with broad product portfolios and global footprints are leveraging scale to offer high‑voltage series and high‑current devices suitable for aerospace, BESS and automotive applications. Their strengths lie in verified performance, global service networks, and the capacity to support complex qualification programs — all attractive to large OEMs pursuing global platforms.

Focused specialists (examples): regional or technology specialists concentrate on specific application sets (e.g., EV traction, solar inverter isolation, or marine battery disconnects). They often move faster on product innovation, customized designs and close OEM co‑development, making them valuable partners for agile OEMs or platforms with unique integration needs.

Emerging challengers: new entrants and vertically integrated OEMs are experimenting with alternative switching technologies and integrated systems that blur the line between contactor and power electronics — a development that could compress demand for traditional contactor form factors over a multi‑year horizon.

To make these dynamics concrete: some established suppliers advertise solutions rated to extreme voltages and currents, suitable for high‑voltage battery and heavy‑duty transportation systems, while others emphasize compact, thermally‑stable packages for new‑energy and industrial control. The practical implication for decision‑makers is to assess suppliers not only by headline ratings but by their roadmap for thermal management, arc suppression and diagnostic integration — the capabilities that determine long‑term system reliability and total cost of ownership.

Prioritize technology gaps that map directly to system acceptance. Allocate R&D and validation spend to arc suppression, thermal stability and embedded diagnostics — these drive OEM qualification and reduce warranty exposure.

Implement supply‑chain de‑risking now. Build raw‑material hedges, secure long‑lead components, and pre‑qualify alternative suppliers in lower‑cost regions while maintaining a pathway to re‑localize critical production if geopolitical or tariff risks rise.

Differentiate through integration. For suppliers, packaging contactors with monitoring and health‑reporting features accelerates adoption among OEMs that value predictive maintenance and digital twins.

Use targeted M&A and partnerships to close capability gaps. Buyers should consider acquiring specialist firms with proven high‑voltage experience or entering licensing agreements to accelerate time‑to‑market without bearing full development risk.

Align commercial terms with system lifecycles. Shift part of your pricing and warranty structures to reflect long‑term system performance metrics rather than unit price alone — this both protects margin and aligns incentives with OEMs.

For large incumbents: double down on platformization and global service capabilities. Your advantage is scale and trust; convert that into long‑term supply agreements, extended warranty offers and bundled service contracts that are hard for smaller suppliers to match.

For specialists and new entrants: focus on speed and customization. Win OEM mindshare by delivering rapid prototyping, shorter qualification cycles and close engineering support. Develop alliances with local Tier‑1s to access larger programs without heavy upfront capital.

For OEMs and system integrators: reframe supplier selection criteria to emphasize lifecycle cost and functional safety roadmaps. Place a premium on suppliers that publish robust test data against evolving safety standards and have a clear plan for manufacturing continuity under commodity stress.

Detailed demand forecasts by application and product type, delivered with an interactive Excel model you can use to test your assumptions (note: specific segmentation tables and supplier financials are available in the paid report).

Supplier scorecards including technology readiness, production footprint, quality incidents and customer concentration metrics.

A regulatory calendar and compliance checklist that maps new safety requirements to test protocols and certification timelines.

Six executable go‑to‑market investments with CAPEX estimates and projected payback periods tailored to different corporate strategies (scale, specialization, or vertical integration).

An 18‑month workplan for procurement and engineering leaders to reduce supplier risk and accelerate product qualification.

The DC contactor market is no longer a low‑visibility component market — it sits at the intersection of power electronics, safety engineering and system integration. For organizations deciding how to allocate capital and engineering resources in 2026, the choices you make now will determine whether you capture the market upside implied by an ~8.8% CAGR or become a price‑squeezed supplier chasing commoditization. PW Consulting’s study is designed to translate that macro projection into pragmatic decisions: which technologies to prioritize, which suppliers to partner with, and where to invest for defensible differentiation. For the full set of datasets, supplier diagnostics and executable roadmaps, visit our report page or contact PW Consulting’s industry team to schedule a briefing and model‑walkthrough.

For detailed analysis of this topic, please visit the official page:DC Contactor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com