Screen Protector Market 2026 — Strategic Imperatives for Leaders

Executive preview

As enterprises prepare budgets and strategic plans for 2026, the screen protector market presents a unique mix of steady, defendable growth and episodic disruption. PW Consulting’s latest study — anchored on a 2025 base year and a rigorous 2020–2025 historical trace — projects a compound annual growth rate (CAGR) of 7.4% across a 2026–2032 forecast horizon. Our topline model quantifies the market expanding from roughly USD 54.9 billion in 2025 to an anticipated USD 90.49 billion by 2032, with 2026 representing an early inflection as manufacturers and channel partners respond to regional industrial policy, material innovation, and emergent regulatory scrutiny.

Screen Protector Market

Why this matters for 2026 decision-making

Market size and growth alone understate the strategic opportunities and risks that will shape enterprise outcomes next year. For incumbents and new entrants alike, three practical realities govern choices in 2026:

Screen Protector Market

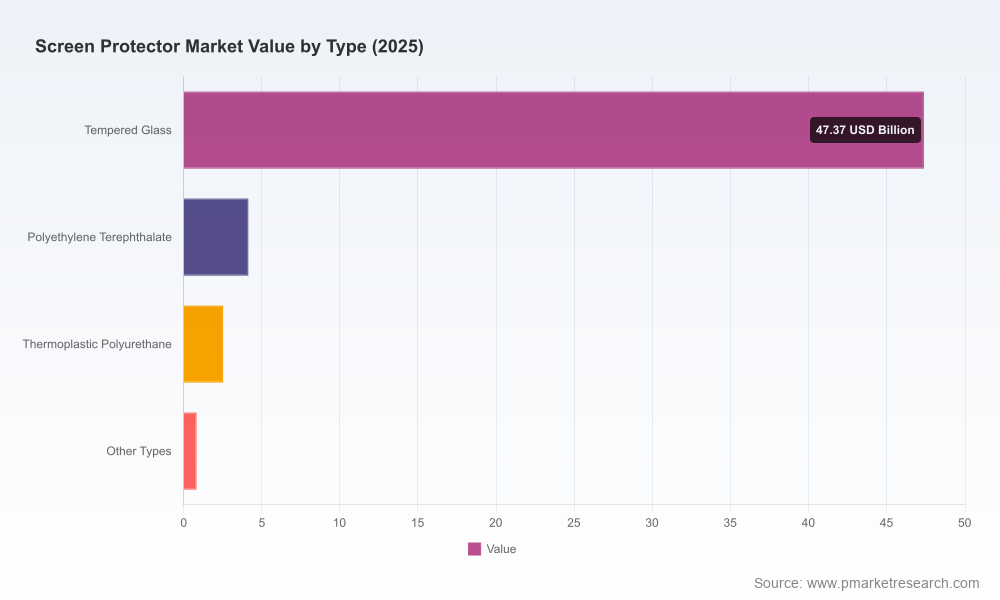

- Scale and specialty matter: categories of premium protection, differentiated materials, and bundled privacy/blue-light solutions are delivering higher margin density than commodity protectors. Capturing premiumization requires investment in materials partnerships and quality-certified manufacturing.

- Policy and trade are active variables: 2025–2026 has already delivered binding events that materially alter cost, sourcing, and competitive posture. Regulatory actions and standards-setting are moving faster than operating cycles in many regional markets.

- Channel fragmentation increases execution risk: global e-commerce and retail channels continue to migrate between direct-to-consumer, OEM accessory programs, and private-label retail supply, demanding distinct commercial models and sharper go-to-market segmentation.

What the numbers reveal — a concise synthesis

Our longitudinal model shows the market rising from approximately USD 38.4 billion in 2020 to USD 54.9 billion in 2025, with projections continuing to grow to roughly USD 91 billion by 2032 under our base scenario (7.4% CAGR). That growth profile masks heterogeneity — pockets of accelerated premium demand and regions where policy-driven local capacity is re-shaping cost curves — which is why 2026 plans must be both quantitatively grounded and scenario-aware.

Screen Protector Market

Market structure and competitive posture

Concentration metrics indicate a moderately concentrated industry: the top three players account for a material share of the market, and the top five increase that concentration meaningfully. This structure favors firms that can combine product differentiation with scale or that can niche into premium or OEM-focused channels.

Our competitive analysis (summarized, non-exhaustive) highlights five archetypal players and their strategic plays:

- Supershieldz — Positioned as a value and volume player in tempered glass for mainstream smartphone protection, emphasizing affordability, ease of installation, and wide compatibility. Tactically strong in retail and accessory channels.

- New Vision Display — A Shenzhen-based manufacturer focused on custom glass solutions for global retailers, OEMs, and private-label partners; notable for leveraging advanced accessory glass in bespoke manufacturing programs.

- ZAGG Inc — A feature-led incumbent, marketing InvisibleShield lines and premium glass innovations (privacy, blue-light filtering, anti-glare), targeting consumers and enterprise users who accept a price premium for differentiated protection and optical performance.

- Spigen Inc — Engineering-centric approach with AluminaCore tempered glass, pitched on extreme durability and fit-for-form-factor design integration with cases and phone ecosystems.

- Optiemus Infracom Limited — A strategical example of policy-enabled local capacity: recently launched a BIS-certified premium line in partnership with a major glass licensor, signaling the emergence of domestically branded premium manufacturing in large emerging markets.

Recent industry developments that will shape 2026

- Standards and certification: The introduction of a national standard and the first BIS certification for tempered glass screen protectors has created fresh incentives for domestic manufacturing in at least one major emerging market, reducing historical import dependence and altering local supplier economics.

- Licensing and partnerships: A high‑profile trademark and licensing agreement between a global glass innovator and a local contract manufacturer illustrates how material technology access is becoming a gatekeeping factor for premium product lines.

- Regulatory escalation: A complaint led to formal notices in early 2026 that could affect imports, product design, or distribution in key developed markets. Firms must treat such proceedings as strategic events — not merely compliance items — because outcomes can reallocate competitive advantage fast.

- Product launches: New premium launches employing engineered glass from global suppliers demonstrate accelerating product sophistication across price tiers.

Practical report takeaways — what PW Consulting delivers

Our full report is designed as an operational toolkit for 2026 strategy teams. Highlights include:

- Transparent methodology and a reproducible demand model that reconciles unit flows, replacement cycles, and aftermarket channel elasticity from 2020 through 2032.

- Scenario-based forecasts with downside, base, and upside cases that quantify the impact of tariffs, standards adoption, and component supply shocks on revenue and margin pools.

- Competitive profiles and capability matrices for key manufacturers and distributors, including go-to-market playbooks tailored to OEM partnerships, retail private-label, and direct-to-consumer models.

- Commercial tools: pricing waterfall templates, margin benchmarking, and channel profitability matrices to guide SKU rationalization and promotional design.

- Regulatory and trade risk matrix with recommended mitigations (sourcing diversification, local certification strategies, and proactive engagement plans for standards bodies and customs authorities).

- M&A and partnership heatmaps highlighting targets and capability gaps for firms seeking bolt-on technologies, contract manufacturing capacity, or distribution scale.

Strategic recommendations for 2026

Based on our synthesis of market dynamics, competitive positioning, and regulatory signals, we recommend five priority actions for executives crafting 2026 plans:

- Lock in material partnerships now. Access to specialized accessory glass and proprietary coatings is a primary determinant of premium positioning. Licensing or JV structures with technology owners shorten time-to-market and protect margin.

- Pursue selective local manufacturing where policy creates durable cost or market access advantages. Certification regimes and local content incentives can materially compress landed costs for regional distribution and support higher margin premium SKUs.

- Design modular channel strategies. Separate operating models for OEM accessory programs, private-label retail, and direct-to-consumer channels enable tailored pricing, return mechanics, and promotional approaches that preserve margin and scale efficiently.

- Build regulatory playbooks. Treat trade complaints and standards proceedings as strategic events: model potential outcomes, pre-negotiate supply contingencies, and establish a rapid-response cross-functional team to engage with authorities and customers.

- Use M&A and contract-manufacturing to accelerate capability. Where organic build-outs are slow or costly, consider asset acquisitions or strategic CM partnerships to secure capacity, certification, or technology access.

Why PW Consulting’s study is decision-ready

Our report combines a demand-driven financial model, validated primary interviews across the value chain, and a curated competitive database that includes both global incumbents and rising regionals. It is structured to guide capital allocation, commercial execution, and risk management for the full 2026 planning cycle.

We intentionally limit public summaries to preserve the commercial sensitivity of subsegment splits, channel-level margins, and the detailed supplier scorecards that are often the basis for rapid competitor responses. The full intelligence set — including granular region/application forecasts, SKU-level pricing benchmarks, and our proprietary probability-weighted scenarios — is available on the report page and via our advisory engagements.

Next steps

If your 2026 plan depends on accurate, defensible market sizing, or if you need an independent risk assessment of regulatory proceedings and sourcing alternatives, engage with PW Consulting to access the full Screen Protector Market study and our scenario modeling suite. The report is built to be immediately actionable for investment committees, commercial leaders, and supply-chain strategists.

For detailed analysis of this topic, please visit the official page:Screen Protector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com