Innovation Trends Driving the US Acoustic Neuroma Market Growth

Health |

2026-06-18 07:29:53

As power systems worldwide push toward higher resilience, greater electrification and more diverse generation sources, surge arresters have quietly moved from commoditized safety components to strategic risk-mitigation assets. PW Consulting’s forthcoming Surge Arresters Market study — anchored on a 2025 base year and projecting through 2032 — translates these technical and commercial dynamics into a pragmatic roadmap for corporate decision-making in 2026. This preview explains why procurement leads, product strategists, corporate development teams and grid operators should treat the report as a near-term playbook, while reserving certain granular segment disclosures for subscribers who download the full analysis.

Surge Arresters Market

The market entered 2025 having more than doubled in scale since 2020 and is forecast to continue a steady expansion at a mid-single-digit compound annual growth rate (CAGR) across the 2026–2032 horizon. That trajectory is far from uniform: macro drivers such as accelerated renewable interconnections, UHV transmission projects, EV charging networks, and distributed energy resources (DERs) are altering demand patterns, while standards updates and localized procurement rules are reshaping product qualification and sourcing decisions. For companies planning capital allocation, product launches or M&A in 2026, timing and scenario planning matter — and immediate access to tailored demand curves and price-sensitivity matrices will materially change outcomes.

Surge Arresters Market

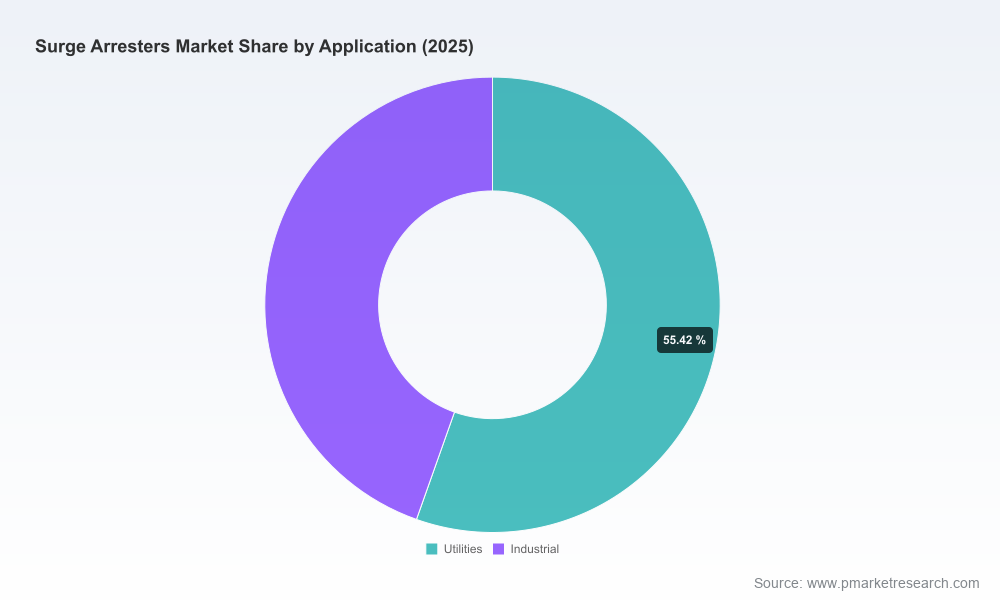

From component to system resilience: Surge arresters are increasingly being specified not as point items but as elements of integrated protection architectures. Manufacturers who can demonstrate system-level reliability improvements (for example, through integrated transformers, modular MV/HV packages, or digital monitoring) are winning longer-term purchase agreements and service contracts.

Surge Arresters Market

Material and form-factor evolution: Polymer housings and metal-oxide varistor technologies continue to displace traditional ceramics in many use cases due to lifecycle, weight and maintenance advantages. However, applications operating at the extremes of voltage and environmental stress still keep legacy formats relevant. The commercial battleground in 2026 will be about guaranteeing lifecycle economics, not just initial procurement costs.

Standards and qualification are leverage points: International standards (notably the IEC benchmark for metal-oxide arresters and recent seismic qualification updates) and localized utility specifications are now gating procurement. Meeting these standards quickly — and documenting compliance across manufacturing lines — accelerates market entry and premium pricing.

Supply chain and tariff exposure: Geopolitical frictions and trade measures remain tail risks. Judicial reviews and evolving tariffs can create sudden sourcing shifts; firms should model alternative supply scenarios and pre-qualify multi-sourcing paths in 2026.

Services and digital upsell: Condition monitoring, lifecycle management and performance-based contracting will be important margin levers. The first movers to offer validated digital prognostics plus contractual uptime guarantees will capture a larger share of serviceable revenue.

Proprietary market sizing and trend trajectories from 2020 through 2032, with base-year granularity (2025) and a 2026–2032 forecast built on scenario-driven demand modelling.

Segment frameworks by material, voltage class and end-use application that explain where volume growth and margin expansion converge (note: detailed segment tables are in the full report).

Supply-chain maps, manufacturing-cost drivers and a supplier qualification checklist tailored to buyers and EPCs.

Regulatory and standards matrix (global and jurisdictional) that flags near-term compliance risks and opportunities for product differentiation.

Competitive landscape intelligence: capability profiles, product roadmaps, strategic moves and an M&A pipeline assessment for active and passive acquirers.

Transaction playbooks — from bolt-on acquisition scoring to JV negotiation checklists — and a buyer’s guide to technical due diligence for arresters, MOV stacks and polymer housings.

Commercial tools: price and margin sensitivity models, procurement negotiation templates, and three field-validated demand scenarios for 2026 planning.

The market shows moderate concentration: global incumbents retain leadership in HV and specialist applications, but regional players and niche specialists remain commercially relevant in distribution and localized manufacturing. Leaders combine deep product portfolios with system-level capabilities and broad qualification records. Notable players profiled in our analysis include:

Hitachi Energy (Switzerland) — Offers comprehensive arrester ranges for medium and high voltage including AC/DC and rail applications. Recent product integration initiatives that embed arresters within transformer solutions underscore a systems-play approach to reliability.

Toshiba (Japan) — Known for high-voltage arresters engineered for demanding applications such as gas-insulated substations; advanced zinc-oxide element engineering remains a differentiator for ultra-high-voltage projects.

Siemens Energy (Germany) — Emphasizes safe and reliable protection products for utility-scale MV and HV assets, pairing arresters with grid digitalization services in target accounts.

ABB, Eaton, Hubbell and TE Connectivity — Each brings complementary strengths ranging from broad electrical infrastructure portfolios to in-house MOV manufacturing and acquisitions that broaden grounding and lightning-protection capabilities.

Specialist and regional manufacturers — Several firms based in India, China, Germany and the U.S. supply competitive products for distribution networks and regional transmission programs; their agility and cost position keep them relevant in price-sensitive tenders.

Recent market moves reinforce strategic themes: Hitachi Energy’s integration of transformers and arresters (late 2025) validates the systems approach; TE Connectivity’s acquisition to deepen grounding and lightning expertise (late 2024) reflects consolidation around complementary capabilities; and several product launches in 2025–2026 point to intensified innovation at both ends of the value chain (from military-grade packaging to application-focused utility solutions).

IEC and IEEE standards continue to be the de facto qualification frameworks. The IEC benchmark for metal-oxide arresters remains central to cross-border supply, while recent seismic performance amendments and new development efforts for controllable metal oxide arresters are shifting test plans and R&D priorities.

Targeted utility specifications (e.g., recent heavy-duty distribution class qualification requirements) are creating localized procurement corridors that favour pre-qualified suppliers.

Trade measures and judicial reviews of tariffs introduce procurement volatility. Firms must maintain compliance intelligence and fast-switch sourcing capabilities.

Pre-qualify multiple sources: Build at least two validated suppliers for each critical voltage class, including one that meets the most stringent local utility specifications likely to appear in tenders.

Invest in systems integration R&D: Prioritise projects that embed arresters into larger electrical modules (transformers, switchgear) or add digital monitoring to support service contracts.

Hedge supply-chain risk: Model tariff and logistics shocks and establish contingency manufacturing routes or buffer inventories for critical components like MOV stacks.

Monetize services: Launch pilot lifetime-performance contracts with at-risk customers to validate premium pricing for condition-monitoring-enabled arresters.

Pursue selective M&A: Target bolt-ons that either (a) add in-house MOV manufacturing, (b) expand qualification scope for HV/UHV projects, or (c) deliver digital analytics capabilities for asset health.

Align testing and compliance timelines: Update product qualification roadmaps to reflect the latest IEC/IEEE amendments and local utility spec windows to avoid requalification delays that can cost quarters in project timelines.

Use scenario planning in procurement: Price and volume sensitivity tools in our report will help procurement teams set contract terms that flex with energy transition trajectories and DER penetration rates.

This study converts market-wide trends into executable choices. It aligns technical qualification requirements and supplier economics with commercial levers — from procurement contract design to product roadmap prioritization. For executives, the primary value is not a single datapoint but a defensible, integrated view of where to invest, what to insource, and how to structure partnerships to capture the next wave of protection-market value.

We have intentionally presented high-level conclusions here to demonstrate the report’s analytical depth while leaving core segment-level breakdowns and proprietary scenario matrices within the full study. Downloading the complete report will unlock the detailed tables, supplier scorecards, tender-level case studies and the interactive financial models that procurement, strategy and M&A teams need to act in 2026 with conviction.

For detailed analysis of this topic, please visit the official page:Surge Arresters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com