Breaking: Evolution of Remote System Access Tools in KVM Switch Market

Other |

2026-04-10 07:37:59

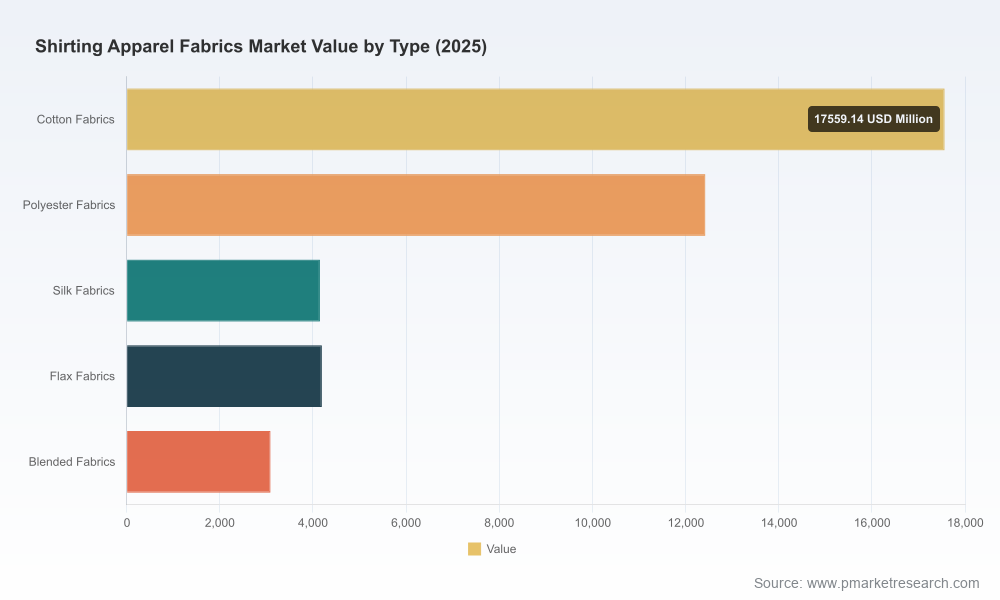

As companies prepare 2026 budgets and three‑to‑five year strategic plans, the shirting apparel fabrics value chain sits at a crossroads: steady organic growth underpinned by shifting trade dynamics, a sharper focus on climate‑positive sourcing, and an intensifying split between premium and volume segments. Our Shirting Apparel Fabrics Market study (base year 2025, forecast 2026–2032) synthesizes historical performance, forward projections and executable playbooks so executives can convert uncertainty into mapped decisions. Headline metrics: the market rebounded from its 2020 position and reached roughly USD 41.4 billion (2025 base), then continues on a steady trajectory (CAGR ~5.9% across the forecast period) toward mid‑2030s scale. This briefing explains the practical strategic value of that analysis for 2026 decision cycles — without giving away the segment-level figures reserved for subscribers.

Shirting Apparel Fabrics Market

Actionable foresight for allocation: Accurate aggregate sizing and a transparent growth path enable CFOs and business unit leaders to prioritize capex, working capital and inventory buffers against a known growth baseline.

Shirting Apparel Fabrics Market

Sourcing and supplier strategy: The report contextualizes how trade shocks and non‑price buyer requirements will affect landed costs and supplier selection, supporting nearshoring vs. offshore trade‑offs.

Shirting Apparel Fabrics Market

Portfolio rationalization and innovation roadmaps: Product teams get a prioritized list of fabric subcategories and technical attributes to invest in to capture expanding pockets of demand.

M&A and JV screening: A market concentration map and competitive heatmap make target screening more surgical, helping corporate development teams shortlist counter‑cyclical or consolidation bets.

Commercial planning and price architecture: Sales and channel leaders can calibrate list‑prices, promotions and private‑label strategies against scenarioed market volumes and expected input‑cost trajectories.

Viewed from the macro lens, the shirting fabrics market now exhibits a predictable expansion pattern: a post‑pandemic recovery phase followed by structural growth driven by replacement demand, rising per‑unit fabric complexity (performance finishes, blended and specialty yarns), and the reconfiguration of sourcing networks in response to geopolitical trade policy. The market advanced materially from its 2020 level to the 2025 base and the forecast horizon to 2032 reflects a mid‑single digit compound annual growth rate (approximately 5.9%). That combination of size and steady growth makes the sector attractive for both scale plays (efficiency and integration) and differentiated plays (premium, sustainable, tech‑enabled fabrics).

Two practical implications follow. First, the growth profile creates runway for investments in automation and finishing‑capability upgrades that shorten lead times and raise margins. Second, the predictability of aggregate growth improves the signal‑to‑noise ratio for long‑lead capex decisions: conversion of spinning/weaving capacity, or rescues for legacy finishing lines, are now assessable against an explicit demand staircase rather than anecdotal forecasts.

The market structure is moderately concentrated: the top three players control a meaningful share, and the top five consolidate a clear majority of tradable shirting fabric volume — a dynamic that rewards scale in commodity cotton and polyester offers, and specialization in premium segments. Against that backdrop, the principal strategic archetypes among leading firms are clear:

Integrated premium mills focused on designer and high‑end buyers (heritage quality, fine finishing). Example archetype: established European mills with direct designer relationships and boutique product lines.

Large vertically integrated textile conglomerates with downstream apparel or uniform contracts, leveraging scale to compete on price and reliability.

Export‑oriented manufacturers who scale through cost advantages, high capacity and multi‑modal sourcing from polyester and cotton blends.

Apparel manufacturers that internalize fabric sourcing to protect margins and lead times for large private label or brand partners.

Operational moves we observe among the named incumbents include: capacity rationalization in mature geographies, accelerated sustainability certification and traceability programs, targeted forward integration into finishing or garmenting, and selective geographic diversification of production and finishing footprints to reduce tariff and logistics risk. Trade shows held in early 2026 reinforced these tendencies — buyers are openly prioritizing accessible ready‑to‑wear shirting and fabrics that combine cost efficiency with demonstrable sustainability credentials.

Three external forces stand out as immediate decision levers:

Tariff volatility: Recent shifts in apparel import tariff regimes have created short‑term price dislocations and a renewed emphasis on reshoring or nearshoring as a hedging strategy. Procurement teams must scenario‑plan for tariff repricing and reconfigure sourcing mixes to avoid margin erosion.

ESG and traceability standards: Updated cross‑industry standards for organic, recycled and responsible fibers are moving from voluntary differentiation to procurement table stakes for many multinational buyers. Certification pathways and supply‑chain mapping are now part of the cost of entry into premium and some mainstream channels.

Technical and quality standards: Accepted performance specifications — including contemporary iterations of woven shirt fabric standards — continue to influence product development cycles and factory compliance expenditures.

For 2026, companies that treat these externalities as strategic constraints (to be engineered around) rather than compliance costs (to be minimized) will unlock superior commercial outcomes.

Designed to be operational, not academic, the full study provides:

A transparent demand model (2020–2032) with scenario toggles for tariff shocks, rapid sustainability adoption, and accelerated premiumization.

Price and input‑cost sensitivity analysis that traces cotton, polyester and finishing chemistry movements through to landed fabric cost under alternate freight and tariff assumptions.

Supply‑chain maps and supplier capability matrices that distinguish mills by finishing, traceability readiness and lead‑time responsiveness — with a shortlist of strategic suppliers for buy‑side outreach.

Competitive playbooks for incumbents and new entrants: recommended moves across product positioning, channel strategy, pricing and partnership templates (including term sheets for toll‑finishing and supply agreements).

M&A and capex heatmaps: attracted subsegments, integration synergies, and a due‑diligence checklist focused on quality control, environmental liabilities and contract continuity.

Commercial launch templates: product spec checklists, sample development timelines and sample costing sheets designed to compress decision cycles between fabric selection and product launch.

Note: the report reserves full segment‑by‑segment tables and granular regional and application‑level figures for subscribers; the content above highlights the practical outputs and decision levers that corporate teams will use immediately.

Procurement — rebuild supplier scorecards around landed cost and certification readiness; use scenario outputs to set strategic inventory and sourcing buffers for potential tariff realignments.

Product development — prioritize fabric attributes that map to growth pockets identified by the model and align sampling cadence to buyer acceptance cycles.

Finance & strategy — overlay the market forecast on internal revenue projections to stress‑test investment cases and M&A valuation assumptions.

Operations — sequence capex to increase finishing versatility and reduce lead times in anticipation of higher SKU complexity across shirting assortments.

Commercial teams — design go‑to‑market plays that pair price tiers with sustainability credentialing to capture both value and volume opportunities.

If your 2026 plan answers these three questions, you are using the right market inputs: 1) Where will my principal buyers be sourcing from under plausible tariff scenarios? 2) Which fabric attributes must I own to remain competitive in my target channels? 3) Which investments in capacity, certification and supplier partnerships produce the fastest, most defendable returns?

Our shirting fabrics study is built to answer those questions with working models, operational playbooks and competitive intelligence. To review the detailed segment tables, supplier shortlists and downloadable templates that translate these insights into executable programs, consult the published report page and accompanying data pack. Pw Consulting’s industry team is available to brief executive committees and to run a tailored scenario workshop that maps these macro projections into your company’s P&L and 2026 action plan.

For detailed analysis of this topic, please visit the official page:Shirting Apparel Fabrics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com