Pet Food Market Trends in Freeze-Dried and Raw Food Products

Food |

2026-03-30 08:22:44

As companies recalibrate product pipelines, supply chains, and investment priorities for 2026, poly(lactic-co-glycolic acid) (PLGA) has moved from a niche polymer to a strategic industrial asset. This preview of PW Consulting’s latest PLGA Market study synthesizes the macro trajectory, structural dynamics, and competitive moves that will matter most for executive decisions in 2026 — while deliberately preserving the granular segment-level data that is central to tactical execution. Consider this a strategic trailer: rich in framing, insight, and implications; reserved on the fine-grained tables and regional/application splits that subscribers will find on the primary report page.

PLGA Market

The PLGA market has demonstrated robust expansion through the recent historical window and is positioned for accelerated scaling across the coming forecast horizon. Our base-year assessment (2025) pegs the global market at approximately USD 149.0 Million (revenue unit: Million USD), reflecting steady recovery and commercialization activity since 2020. Looking ahead into the forecast period (2026–2032), PW Consulting projects a compound annual growth rate (CAGR) of 13.5%, targeting a market roughly double the 2025 size by the end of 2032.

PLGA Market

Market concentration remains modest: the combined share of the top three suppliers is under one quarter, and the top five do not exceed one-third of the market. That fragmentation signals ample room for scale players to capture value, while also leaving niches for specialized and regional producers to defend. For decision-makers, the combination of high growth and moderate concentration creates both commercial opportunity and competitive urgency.

PLGA Market

Commercialization wave of PLGA-based therapeutics — long-acting injectables (LAIs), implantable devices, and advanced drug-delivery systems — continues to broaden market pull. Regulatory pathways are maturing, and approvals for PLGA-enabled formulations have progressed without new high-profile safety recalls in 2025, reducing regulatory uncertainty for sponsors.

Supply-chain shocks and trade policy shifts that crystallized in 2025 are still reshaping sourcing strategies. A tariff recalibration implemented in early March 2025 materially altered the economics of Chinese-origin polymer imports and accelerated diversification initiatives among Western purchasers and OEMs.

Raw-material and upstream cost drivers — notably lactic acid feedstock pricing and fermentation/purification labor intensity — are sustaining upward pressure on production cost structures. These factors are not transitory and should be modeled into five-to-seven-year procurement and pricing strategies.

Demand drivers are multifold and intersect with both the pharmaceutical innovation cycle and medical-device adoption. Clinically, PLGA’s established biocompatibility and tunable degradation kinetics continue to attract formulators pursuing controlled-release profiles and implantable scaffolds. Commercially, manufacturers are accelerating formulation platforms and platform partnerships to lower time-to-clinic for LAIs and novel delivery formats.

On the supply side, three dynamics stand out. First, feedstock economics: lactic acid pricing moved higher through 2025, reflecting healthy demand from PLA and PLGA manufacturers and placing a premium on procurement flexibility. Second, policy-driven sourcing shifts: tariff increases on certain Chinese-origin polymers took effect in early 2025, lifting duties and prompting many buyers to re-evaluate supplier footprints. Third, production cost structures — the fermentation and purification stages intrinsic to lactic acid and copolymer manufacture — keep baseline costs elevated, incentivizing process optimization and vertical integration conversations.

The PLGA value chain spans multinational specialty-chemicals players, GMP-certified polymer manufacturers, and regionally focused suppliers. Strategic moves in 2024–2025 highlight two important themes: channel consolidation for medical-grade polymers and focused commercial partnerships to accelerate device adoption.

Corbion N.V. (Amsterdam) — a key supplier of GMP-grade copolymers focused on controlled-release excipients — continues to show growth in lactic-acid-derived products. Recent financial disclosures indicate resilient lactic acid demand from PLA and PLGA producers, reinforcing Corbion’s market posture in high-purity feedstocks and excipient-grade offerings. Strategic implication: firms seeking supply security or formulation co-development should consider early-stage engagement with Corbion to secure prioritized allocation and technical collaboration.

Evonik Industries AG (Essen) — with established branded PLGA families used in parenteral and implantable devices — has deepened its commercial reach through distribution partnerships. Notably, the appointment of an exclusive European distributor for bioresorbable polymers underscores Evonik’s channel strategy to accelerate clinical adoption. Strategic implication: device OEMs and contract development partners should map distributor coverage when evaluating supplier access, regulatory support, and logistics.

Akina, Inc. (West Lafayette) and Merck KGaA (Darmstadt) — both offer research- and GMP-grade PLGA variants that serve academic labs through to late-stage formulators. Their positioning highlights the spectrum from discovery-supporting materials to clinical-grade supply. Strategic implication: R&D organizations can leverage breadth from these suppliers to shorten the transition from bench to GMP studies, but must verify scale-up pathways early.

Nomisma Healthcare Pvt. Ltd. (Pune) — as a regional manufacturer, exemplifies the expanding supplier set in emerging markets. These players can provide cost-competitive supply and flexible manufacturing for certain product classes, but buyers should rigorously evaluate regulatory dossiers and quality systems before scaling applications with such partners.

Across the competitive landscape, two tactical themes emerge. First, distribution and channel arrangements (e.g., exclusive distribution deals) materially change market access and should be assessed in supplier selection. Second, the moderate market concentration means strategic M&A or capacity investments by large players would materially alter competitive dynamics — a risk/opportunity that should be monitored by corporates with expansion plans.

The complete PLGA Market report is structured to translate macro trends into executable recommendations. Subscribers will receive:

Comprehensive market sizing and validated historical time series (2020–2025) and forward-looking forecasts (2026–2032) with scenario modeling.

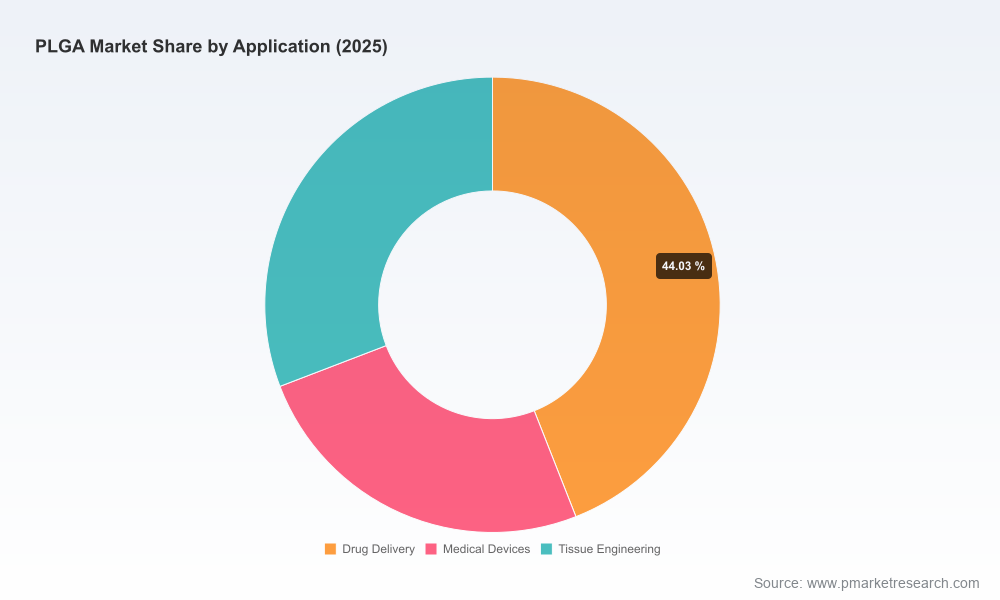

Segment-level analytics across regional, polymer-type, and application axes — including demand drivers, price trends, and adoption curves. (Note: detailed segment breakdowns and tables are reserved for the full report.)

Supply-chain heat maps identifying critical nodes, supplier concentration, and potential single-source risks.

Competitive profiles and benchmarking for the key PLGA providers, plus an M&A watchlist of strategic and financial buyers.

Regulatory landscape and approval-pathway synthesis for PLGA-enabled therapeutics and devices, with implications for clinical timelines and reimbursement considerations.

Practical playbooks for procurement, price-hedging strategies, contract manufacturing partner selection, and R&D de-risking.

Re-assess sourcing footprints now, not later. Tariff shifts and feedstock price volatility require diversified supplier shortlists and contingency capacity. Secure prioritized allocation or tiered contracts with GMP suppliers to protect clinical timelines.

Embed cost modeling into product economics. Incorporate elevated upstream fermentation and purification costs into lifetime product-cost models and pricing strategies, especially for complex delivery systems with narrow margins.

Accelerate technical partnerships. Co-development with polymer suppliers or CDMOs can shorten scale-up risks. Early technical transfer agreements and shared stability datasets reduce downstream regulatory surprises.

Monitor distribution and channel shifts. Exclusive distributor agreements for branded bioresorbables can materially affect product availability and go-to-market timelines in critical regions; factor channel access into procurement and clinical site planning.

Stress-test regulatory pathways. The absence of new major restrictions in 2025 is encouraging, but regulatory expectation-setting for LAIs and implantables continues to evolve. Prototype regulatory dossiers and pre-submission engagements remain essential.

This preview deliberately focuses on macro-trajectory, competitive posture, and strategic implications. To preserve the utility of the intelligence as an actionable asset, we have withheld the granular regional and application-level splits, detailed price curves, and contract-level supplier metrics that are essential for execution. These are available in the full PW Consulting PLGA Market report, which contains the tables, primary-source references, and scenario workbooks that enable precise capital-allocation, procurement negotiation, and clinical-planning decisions.

PLGA’s market story entering 2026 is one of maturation: expanding clinical utility, accelerating commercialization, and intensifying supply-chain complexity. For executives, the window to translate this growth into durable competitive advantage is immediate. Firms that internalize the macro projections, hedge supply and cost risks, and align R&D and commercial models to evolving distribution realities will capture disproportionate value as the market roughly doubles over the forecast horizon.

PW Consulting’s full PLGA Market report is designed to move teams from strategic intent to operationalized plans. For the granular datasets, supplier scorecards, and step-by-step playbooks referenced here, visit the full report page to obtain the complete intelligence package and the underlying data appendices.

For detailed analysis of this topic, please visit the official page:PLGA Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com